Here at EquityEdge Research, we make Small-Cap Investing easy for you by Backing you up with Robust & Full-Fledged Research.

Please Fill the form Below if you are interested in our Services and would like a Free Sample of our Equity Research Report covering a Small/Micro-cap Company.

Read our Previous Report here:

Table of Contents:

Key Highlights.

Company Price Chart Analysis.

About the Company.

Management Analysis.

Business Breakdown.

Financial Analysis

Ratio Analysis.

Shareholding Analysis.

SWOT Analysis.

Concall Analysis (Q1FY26).

Growth Drivers & Risks/ Challenges for the Company.

Competitor Analysis.

Premium (Includes Free):

Global Contract Research Organization Industry.

Indian Contract Research Organization Industry.

Financial Analysis- Quarterly.

Competitive Analysis- Bio & Financials.

Daily Share price trend TTM- Peer comparison.

Company Relative Valuation.

Segment Wise Performance.

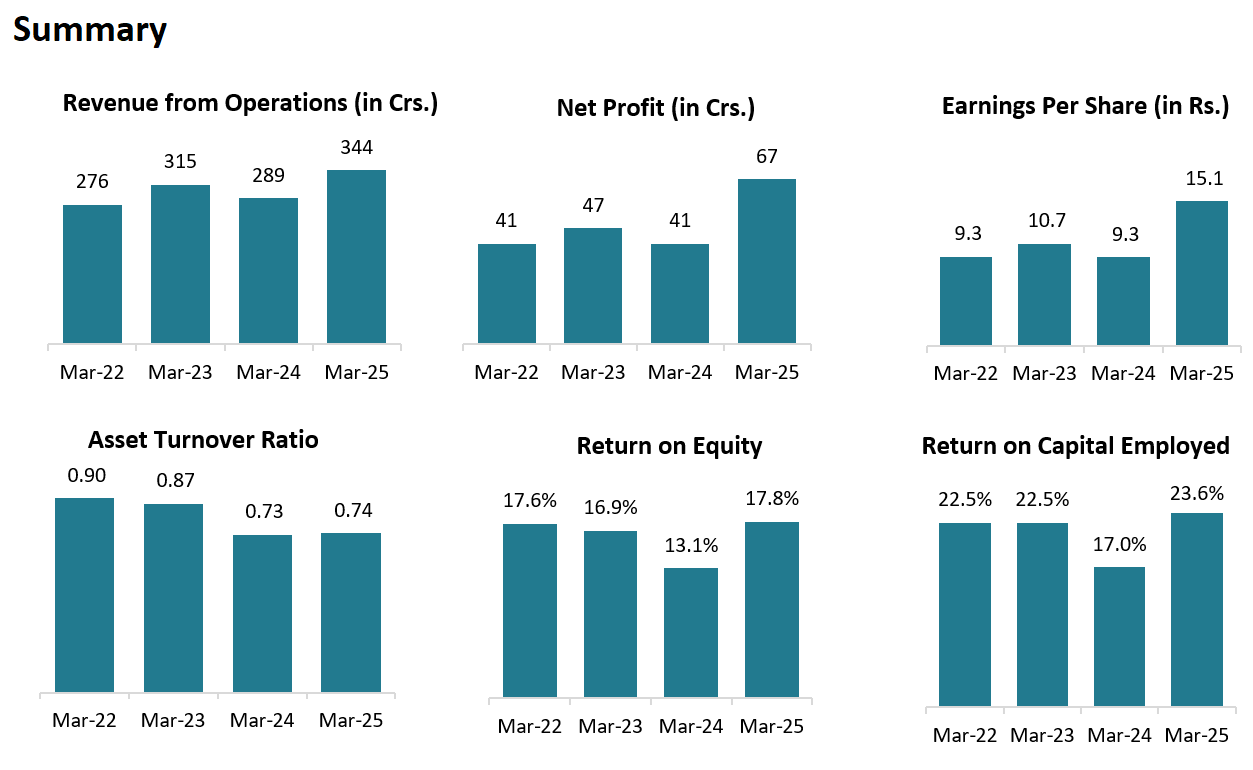

1. Key Highlights:

FY26

REVENUE: ₹ 344 Cr. (+19.03% YoY)

EBITDA: ₹ 122 Cr. (+32.61% YoY)

EBITDA MARGIN: 35% (+200 YoY)

PAT: ₹ 67 Cr. (+63.41% YoY)

Q2FY26

REVENUE: ₹ 102 Cr. (+4.08% QoQ, +20% YoY)

EBITDA: ₹ 34 Cr. (No Change in QoQ, +13.33% YoY)

EBITDA MARGIN: 34% (-100 bps QoQ, -100 bps YoY)

PAT: ₹ 20 Cr. (+5.26% QoQ, +33.33% YoY)

OTHER HIGHLIGHTS:

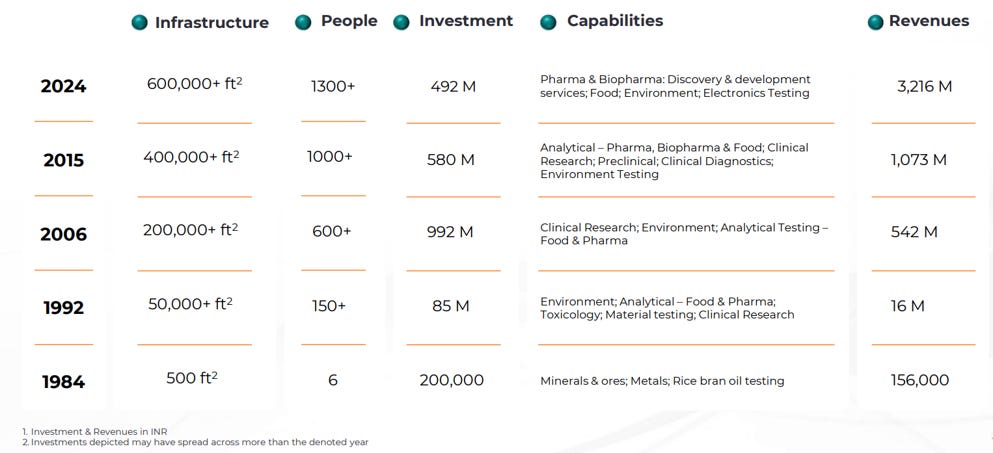

Presence: 10 labs across India, 600,000+ sq. ft. lab space.

Global Clientele: 36% revenue from overseas in Pharma Analytical; 75% in Clinical Research.

Team: 1,300+ multidisciplinary professionals.

Strong cash position: ₹545 Mn cash & equivalents.

Capacity Expansion: Added ~200,000 sq. ft. of lab space at Life Sciences Facility.

CAPEX Outflow: ₹39 Mn.

Free Float: 63.3%.

2. Company Price Chart Analysis:

*Comparison charts are Indexed*

2.1 Vimta Labs Ltd. Performance:

2.2 Vimta Labs Ltd. Vs. NIFTY:

2.3 Vimta Labs Ltd. Vs. NIFTYSMLCAP50:

3. About the Company:

Vimta Labs Ltd. is one of India’s leading scientific services and contract research organizations (CROs). Founded in 1984 and headquartered in Hyderabad, the company provides high-end analytical testing, research, and laboratory services across a wide range of sectors including pharmaceuticals, biotechnology, food, chemicals, environment, clinical studies, and government / regulatory work. Vimta’s services are used by domestic and global clients for product development, quality assurance, regulatory compliance, and safety evaluations. The company operates multiple integrated laboratories in India and abroad, staffed with scientific expertise and advanced instrumentation, enabling it to support customers throughout the R&D and product lifecycle.

3.1 BUSINESS SEGMENTS:

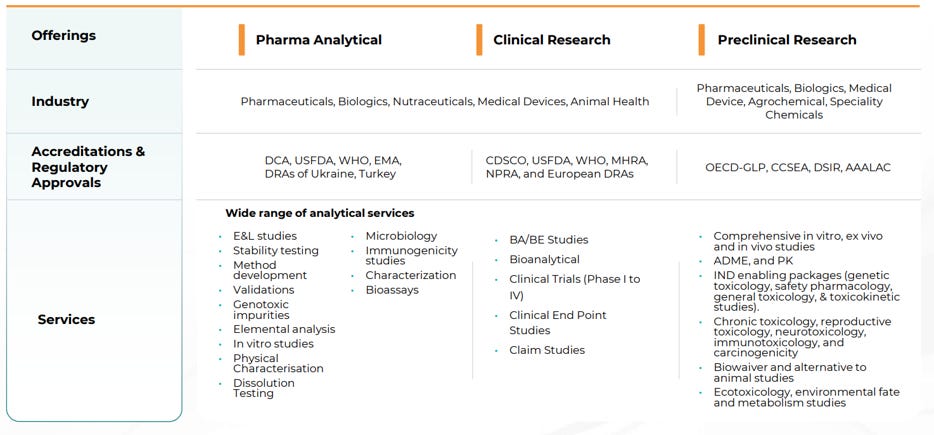

Drug Discovery & Development / Contract Research Services: This is one of Vimta’s core scientific offerings. It includes pre-clinical research, bioanalytical services, toxicology studies, pharmacokinetic assessments, and molecular biology support for biopharmaceutical and pharmaceutical companies. This segment helps clients discover, optimise, and validate new drug candidates before clinical trials or regulatory submission, and is important for global CRO partnerships.

Pharmaceutical Testing & Quality Control Services: This segment covers analytical testing of active pharmaceutical ingredients (APIs), formulations, and intermediates to ensure quality, purity, safety, and compliance with regulatory standards. It includes stability studies, method development/validation, impurity profiling, and release testing. These are services that pharmaceutical manufacturers and exporters need to meet global regulatory requirements (e.g., US FDA, EMA).

Clinical Research Services: Vimta supports clinical trials and associated laboratory evaluations (e.g., clinical biochemistry, hematology, microbiology, biomarker assays) for biotech and pharma sponsors. This segment enables clinical studies from Phase I to later stages by providing integrated lab support and data reporting.

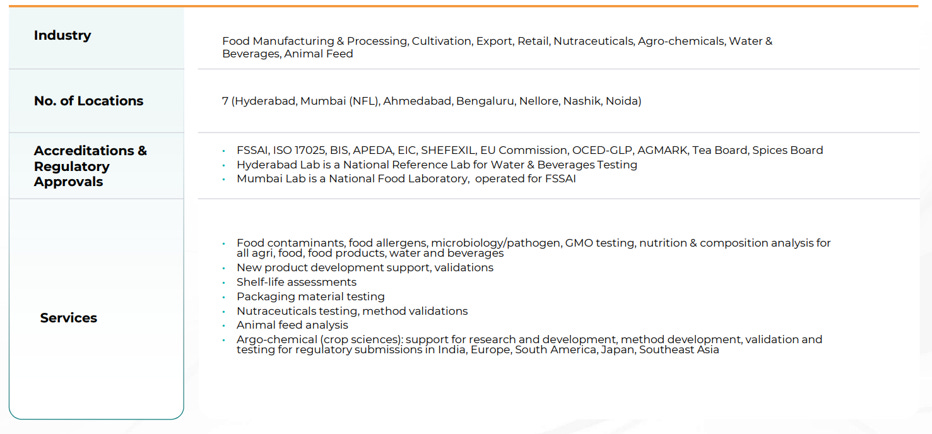

Food, Environment & Consumer Product Testing: This segment comprises testing of food products, beverages, water, cosmetics, consumer items, and environmental samples for contaminants, composition, microbial quality, and safety standards. It supports brand owners, food processors, FMCG firms, regulatory agencies, and export compliance checks.

3.2 Company Journey:

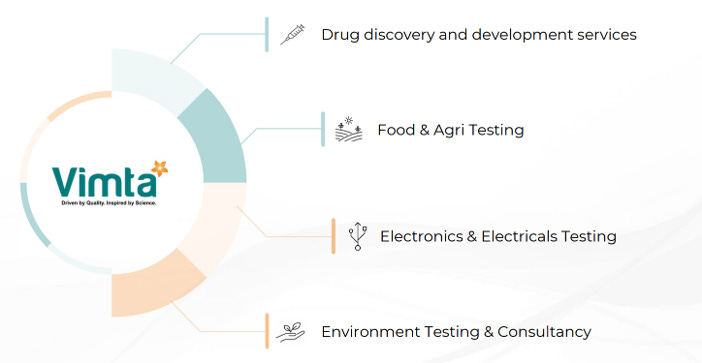

3.3 Company Offerings:

3.4 Drug discovery and development services:

3.5 Food & Agri Testing:

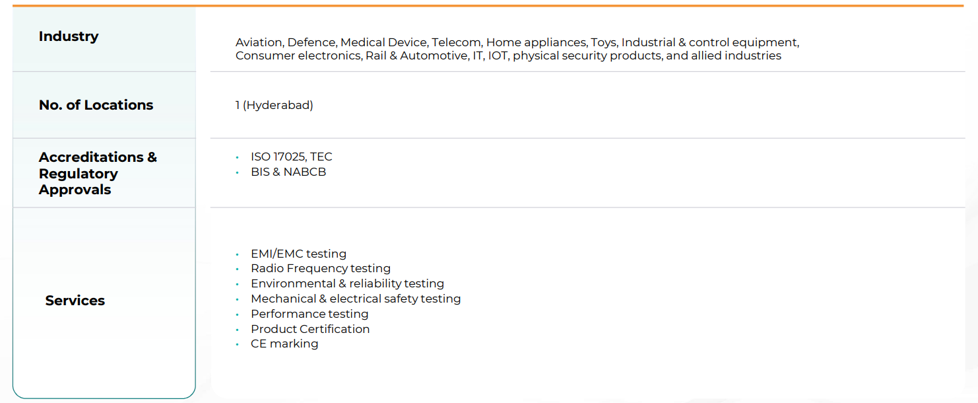

3.6 Electricals & Electronics Testing & Certification:

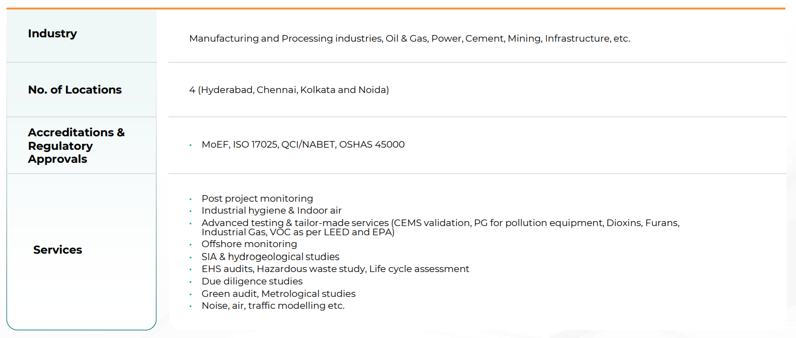

3.7 Environment Testing & Consultancy Services:

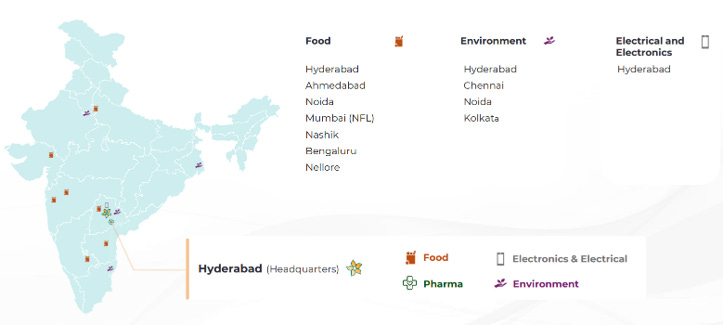

3.8 Geographical Presence:

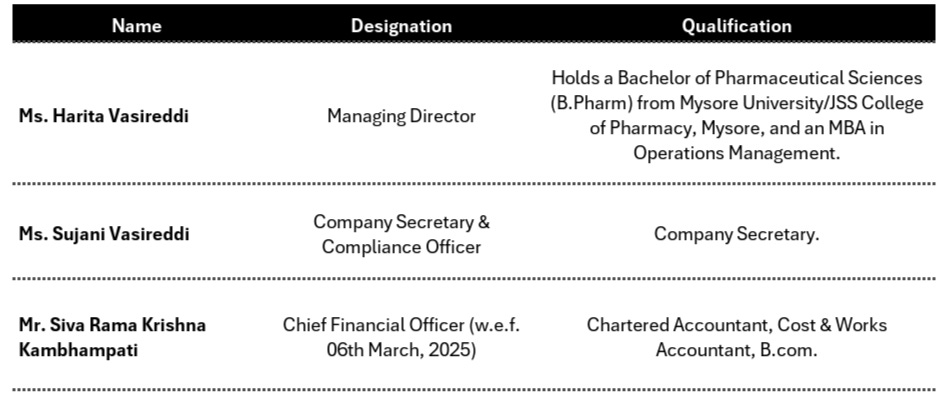

4. Management Overview:

4.1 KMP’s Remuneration:

5. Business Breakdown:

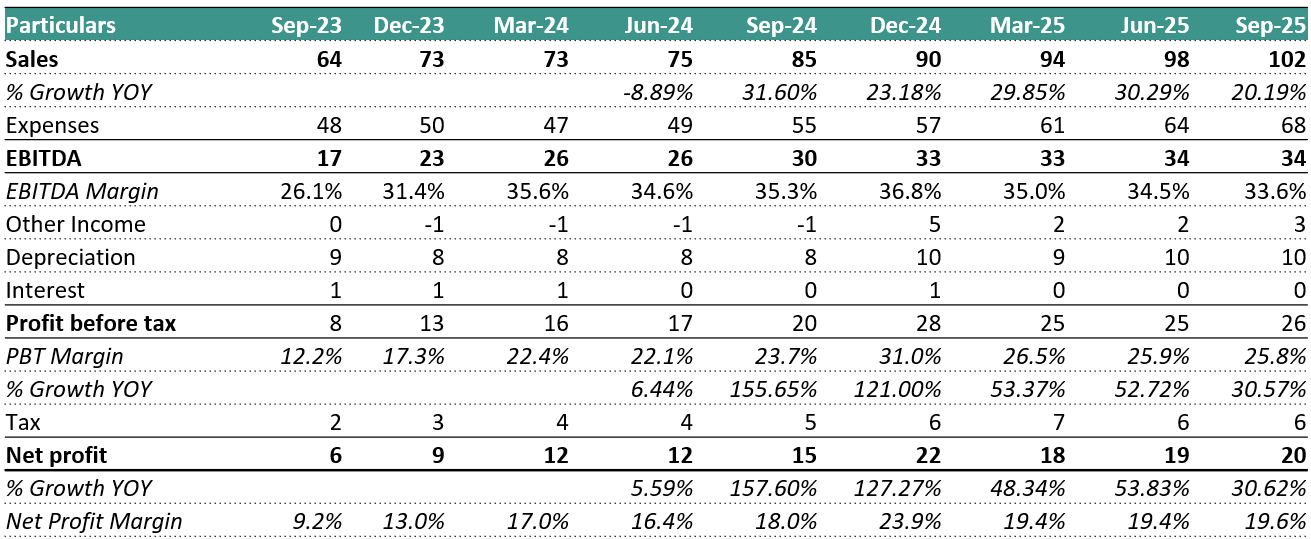

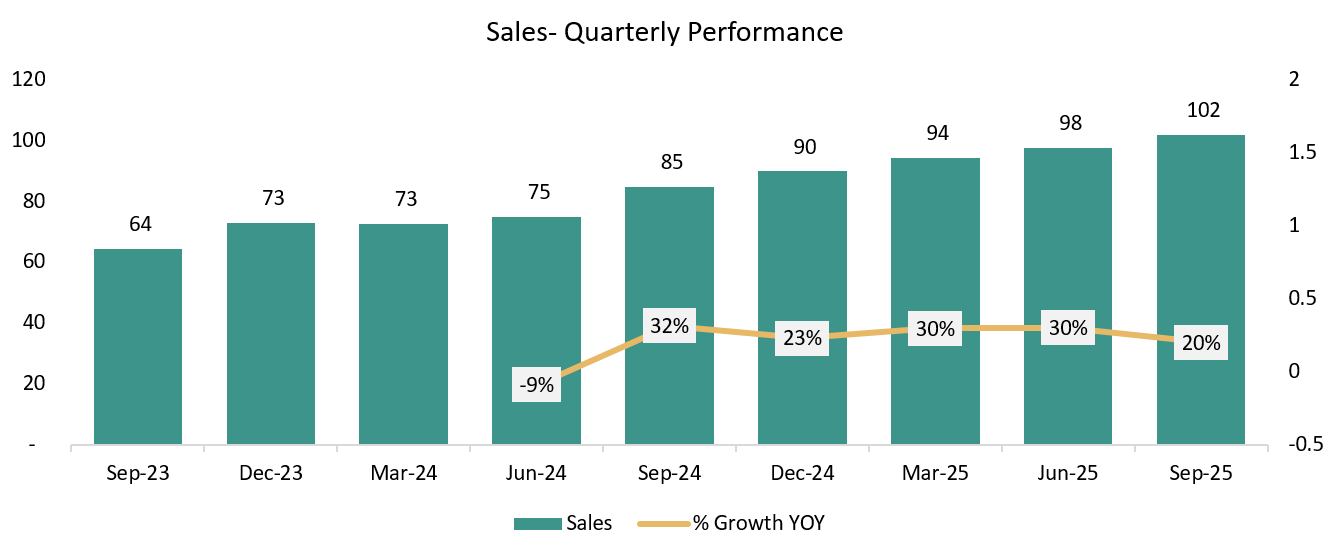

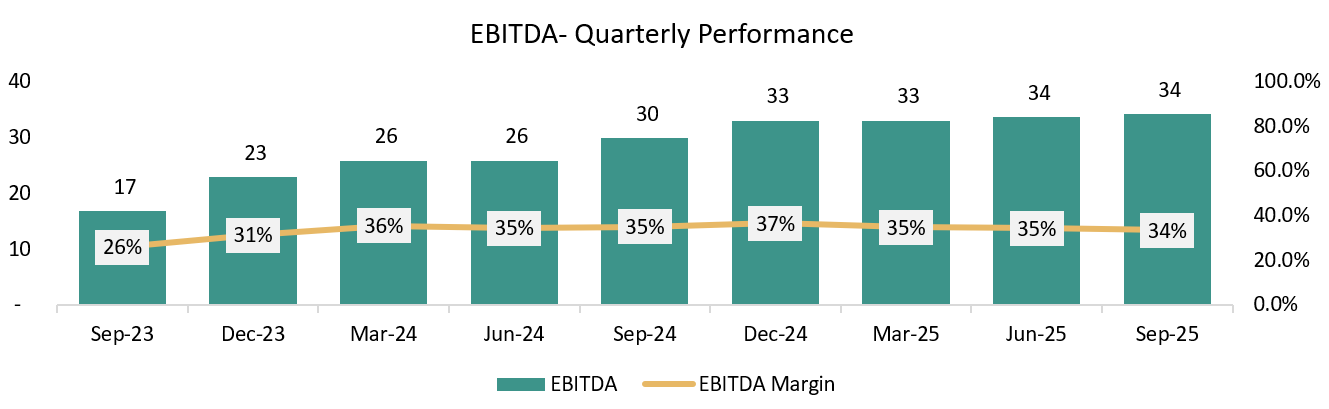

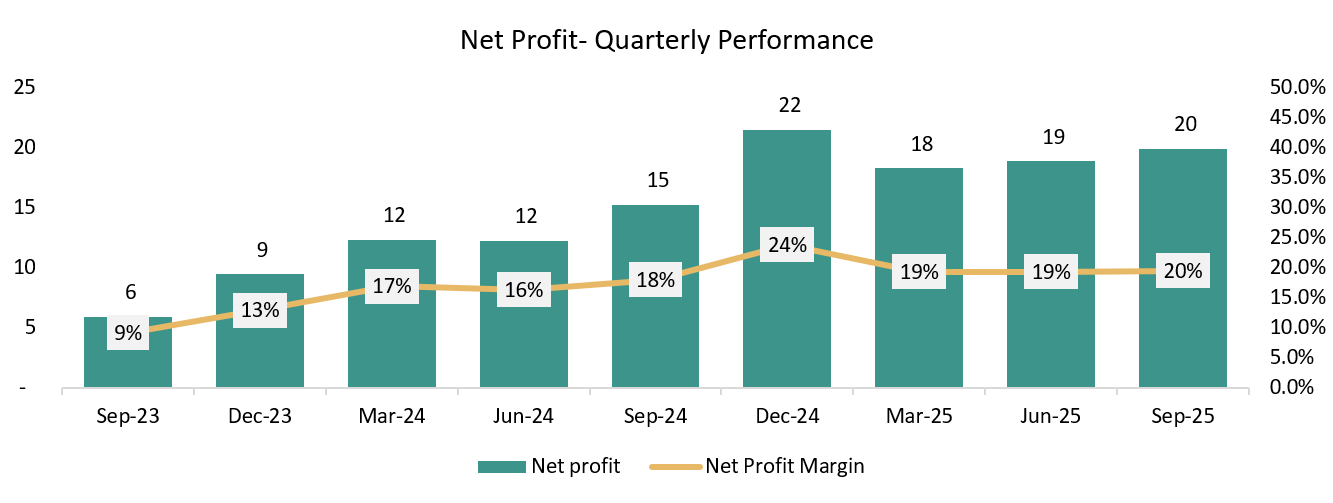

6. Company’s Financial Analysis:

QUARTERLY ANALYSIS:

(Read detailed Quarterly Analysis in the Premium Version)

Growing at a CQGR of 5.9% in last 9 Quarters.

Growing at a CQGR of 9.3% in last 9 Quarters.

Growing at a CQGR of 16.4% in last 9 Quarters.

ANNUAL ANALYSIS:

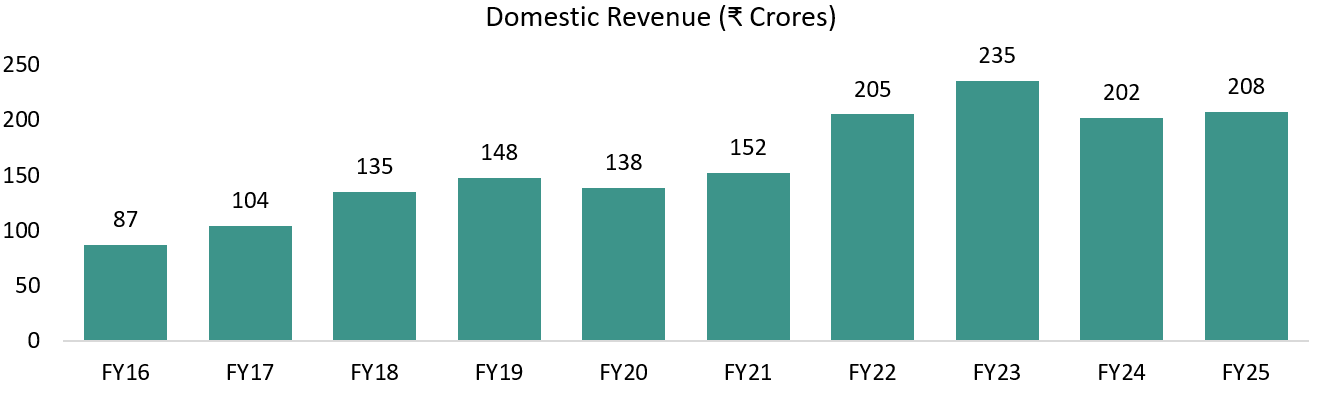

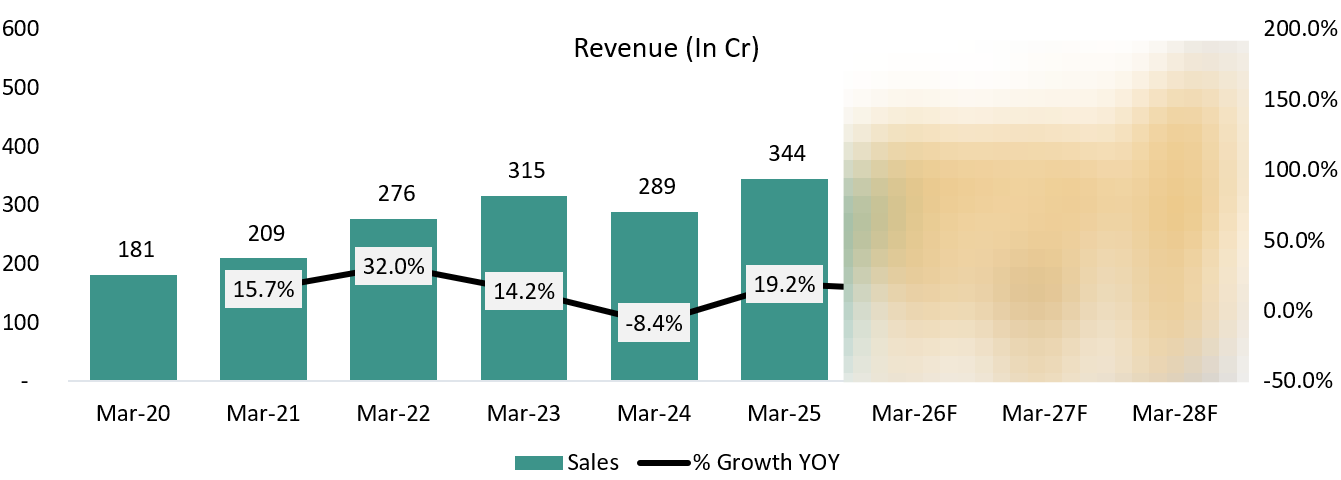

6.1 Revenue:

(Read detailed Annual Analysis and Forecasts in the Premium Version)

FY24 was a transition year for Vimta. Revenue was impacted by a slowdown in global pharma spending, particularly in clinical research, and by capacity constraints that limited the onboarding of new customers. At the same time, management deliberately exited low-margin diagnostics by shutting down the Kolkata and Delhi diagnostic labs, which reduced reported revenue but improved the quality and margin profile of the business.

The year was also used to build capacity and compliance, with investments in new facilities at Genome Valley and upgrades to quality and IT systems — groundwork that did not immediately show up in revenue.

Going forward, these constraints have largely eased. New facilities are operational, capacity is no longer a bottleneck, diagnostics drag is behind the company, and growth is now execution-led. This underpins management’s confidence in scaling the core pharma and food testing businesses and achieving a ₹500 crore annualized exit run-rate (~₹125 crore per quarter), with biologics contributing only from FY27.

Our expectations differ from Management’s expectation of growth.

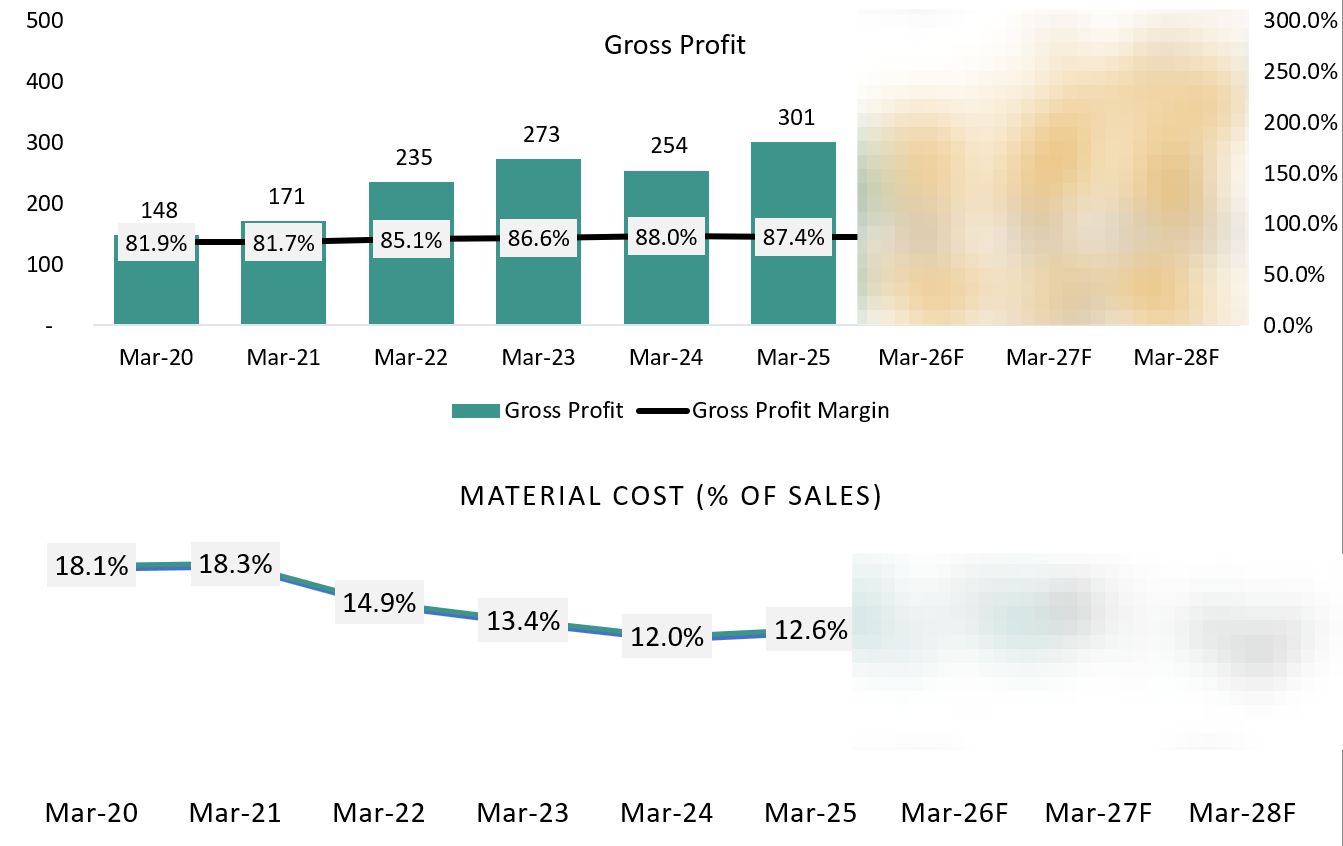

6.2 Gross Profit:

Historically, Vimta’s gross profit was affected less by pricing and more by cost absorption and mix. During FY24, gross profit growth was muted because capacity utilisation was sub-optimal while the company was still carrying the cost base of expanded infrastructure. In addition, the diagnostics business (before the Kolkata and Delhi lab shutdowns) had a structurally lower gross margin, which diluted overall profitability.

As FY25 progressed, gross profit improved meaningfully as utilisation picked up in the core pharma and food testing segments and the diagnostics drag was removed. Higher-value pharma testing, better sample throughput, and improved operating discipline allowed a larger portion of revenue to convert into gross profit.

Going forward, management expects gross profit to strengthen further as capacity utilisation improves at the Genome Valley facilities, the business mix continues to shift toward pharma research and food testing, and cost absorption improves. With no major raw-material or pricing headwinds flagged, gross profit expansion is expected to be volume- and utilisation-led rather than price-driven.We expect the Gross Margin and Material Cost to remain stable in future.

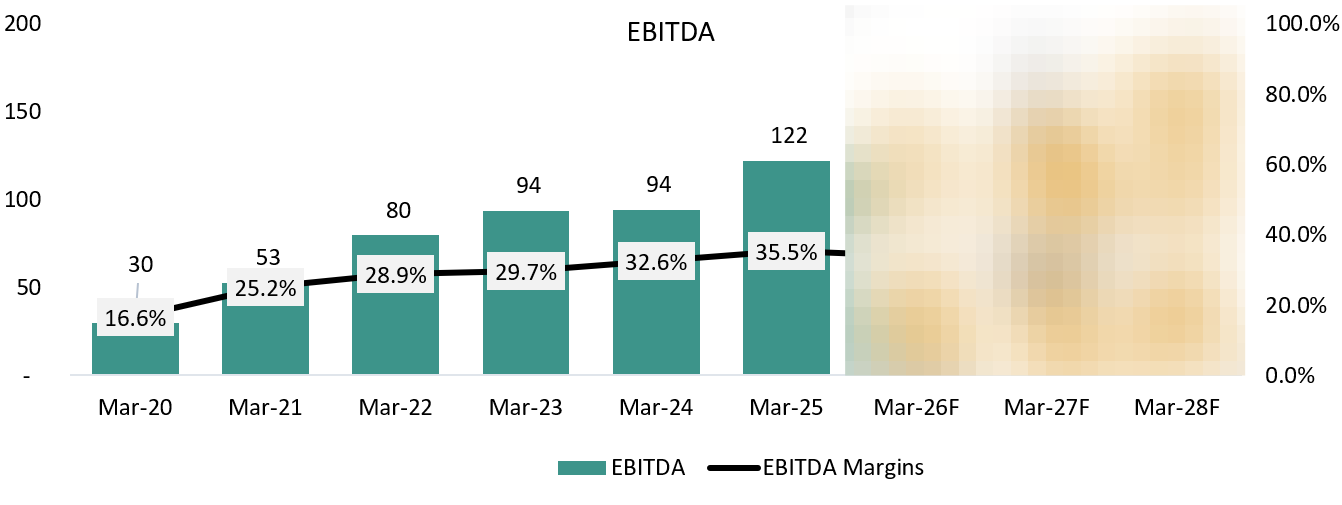

6.3 EBITDA:

EBITDA performance over the last few years has largely been a function of how well Vimta absorbed its fixed cost base, rather than sharp swings in pricing. During FY24, margins were capped because the company was running below optimal utilisation while carrying higher employee, compliance, and infrastructure costs following expansion. This kept EBITDA from fully reflecting the underlying strength of the core pharma testing business.

From FY25 onward, EBITDA began to expand steadily as utilisation improved, and the lower-margin diagnostics business (including the Kolkata and Delhi labs) was exited. Importantly, the margin improvement was not driven by cost cutting, but by better throughput on an already-built cost base.

Looking ahead, management expects EBITDA margins to remain structurally strong as capacity is no longer a constraint and incremental revenue comes with limited incremental fixed costs. Investments in manpower and compliance will continue, but at a pace that allows operating leverage to play out, supporting sustained EBITDA growth as the company moves toward its targeted exit run-rate. We expect the EBITDA Margin to stay stable as well.

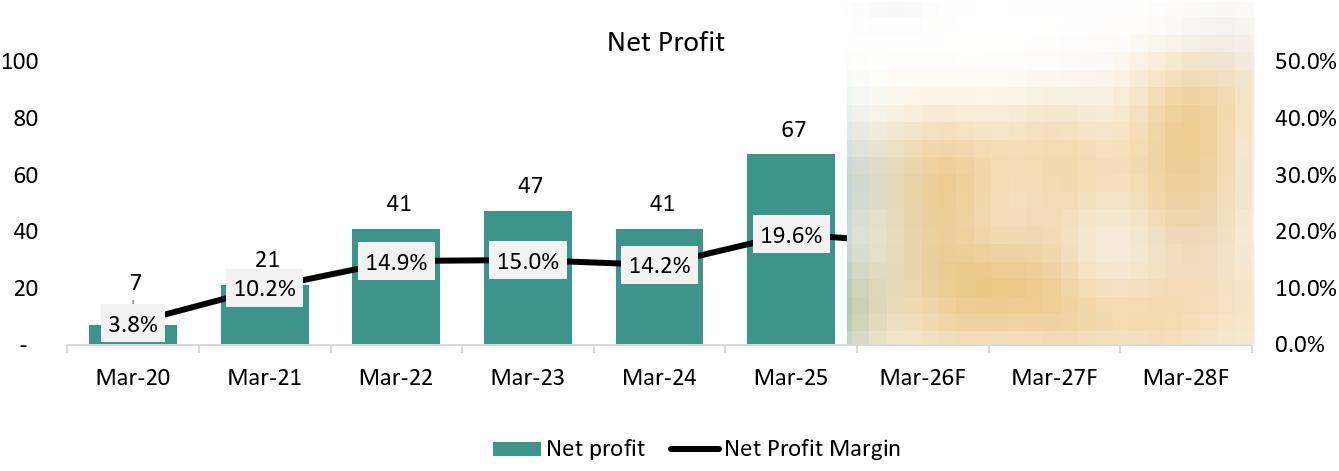

6.4 Net Profit:

Net profit trends at Vimta have largely mirrored the clean-up and stabilization below the operating line. In FY24, PAT growth was restrained not because EBITDA was weak, but because higher depreciation from new facilities and a normalizing tax outgo limited bottom-line expansion. Importantly, this was a quality issue, not a stress issue.

From FY25 onward, net profit began to scale more predictably as depreciation stabilised, interest costs remained negligible, and operating gains flowed through with minimal leakage. The exit from diagnostics (including the Kolkata and Delhi labs) also removed a volatile, lower-quality earnings stream, improving consistency.

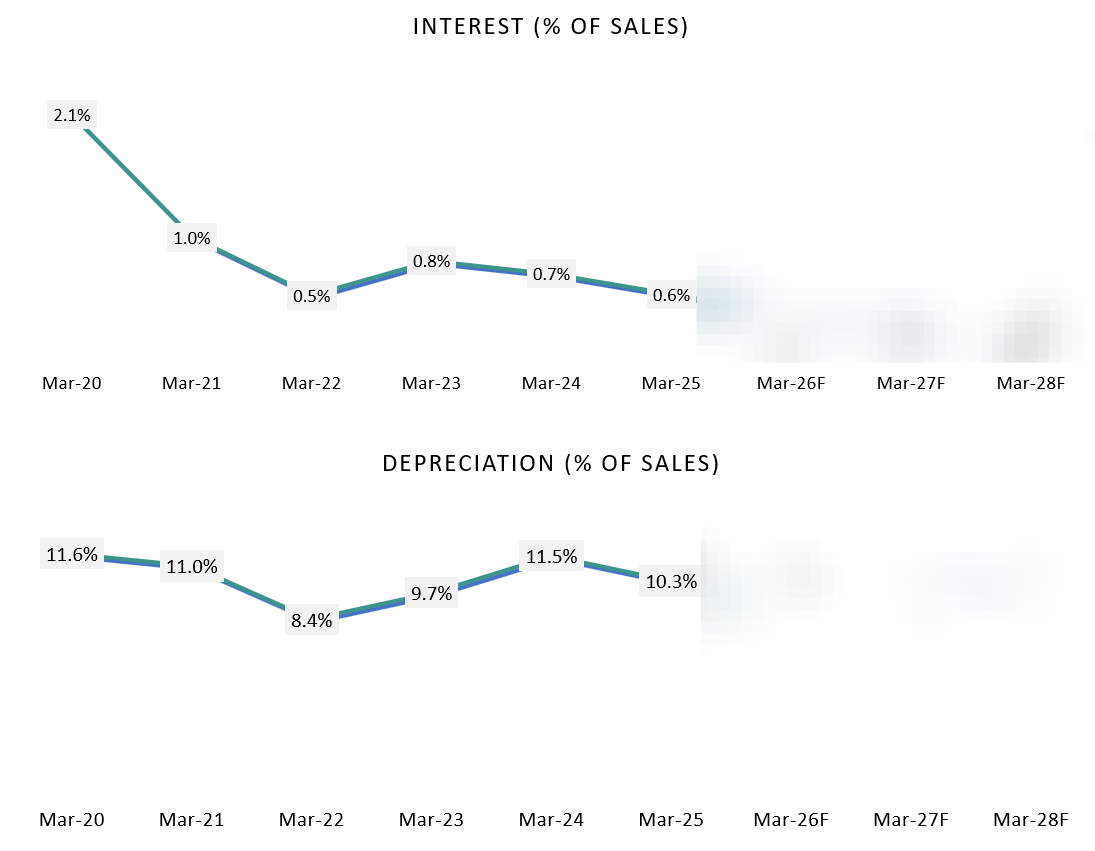

Going forward, management expects PAT to grow steadily with operating performance, supported by negligible finance costs and stable tax rates. With no dependence on leverage or one-offs, net profit growth is expected to remain clean, predictable, and execution-driven, in line with the company’s move toward its targeted exit run-rate. We expect the depreciation to stay high in the near future due to recent capex made by the company.

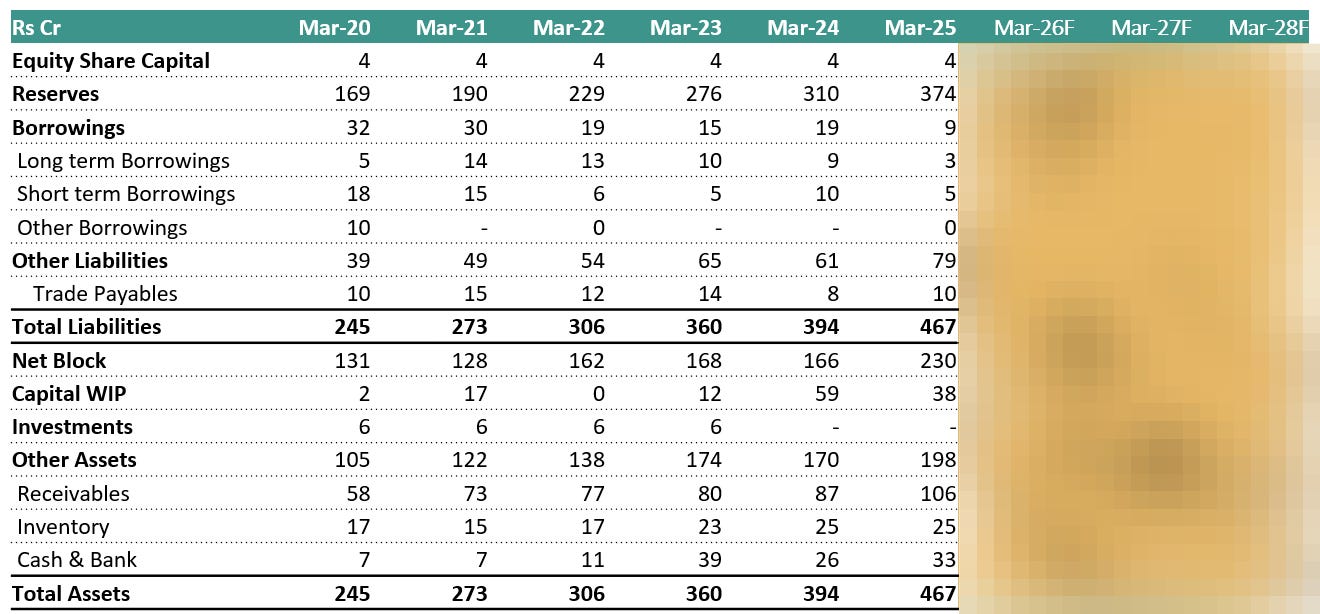

6.5 Balance Sheet:

Debt remains negligible and not a growth lever. Management has repeatedly clarified that Vimta operates with minimal to near-zero interest-bearing debt, and growth plans do not rely on leverage. This is reflected in consistently low interest costs and reinforces that expansion is being funded through internal accruals.

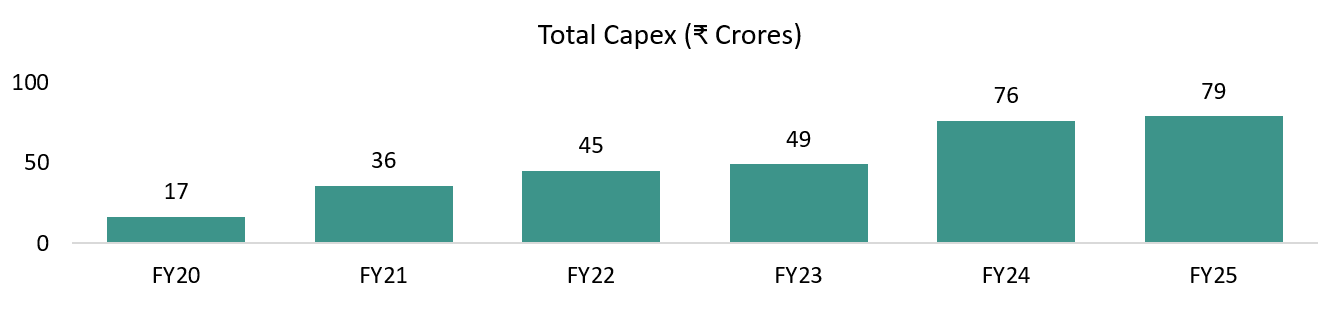

Capex has already been largely incurred. The major balance-sheet change over the last few years has been the increase in fixed assets due to Genome Valley facility expansion and compliance infrastructure. Management has stated that this capex phase is largely behind them, and current assets are sufficient to support growth for the next 5–6 years, limiting the need for heavy incremental capex.

Working capital is stable and well controlled. Management has indicated that receivables and working capital remain under control, with no mention of stretched debtor days or collection stress. Growth in receivables is described as volume-led rather than credit-led.

Asset productivity is improving. With depreciation stabilising and utilisation rising, management views the balance sheet as entering a phase where returns improve without proportional asset addition, allowing operating and net profits to scale on an already-built base.

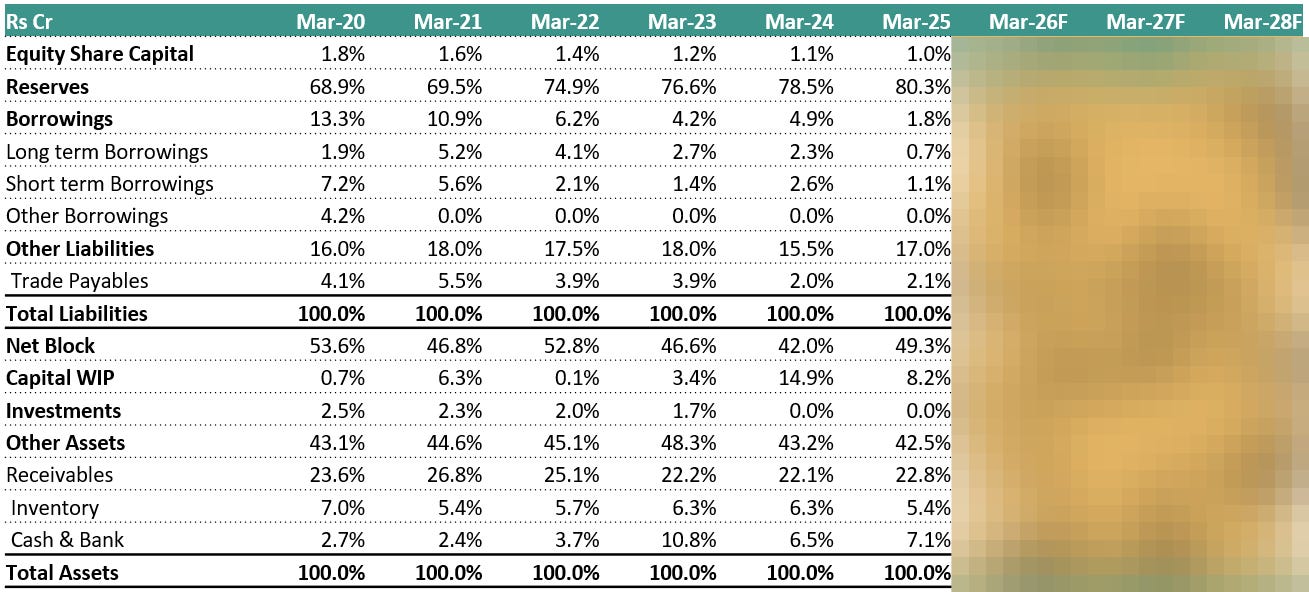

6.6 Common-Size Balance Sheet:

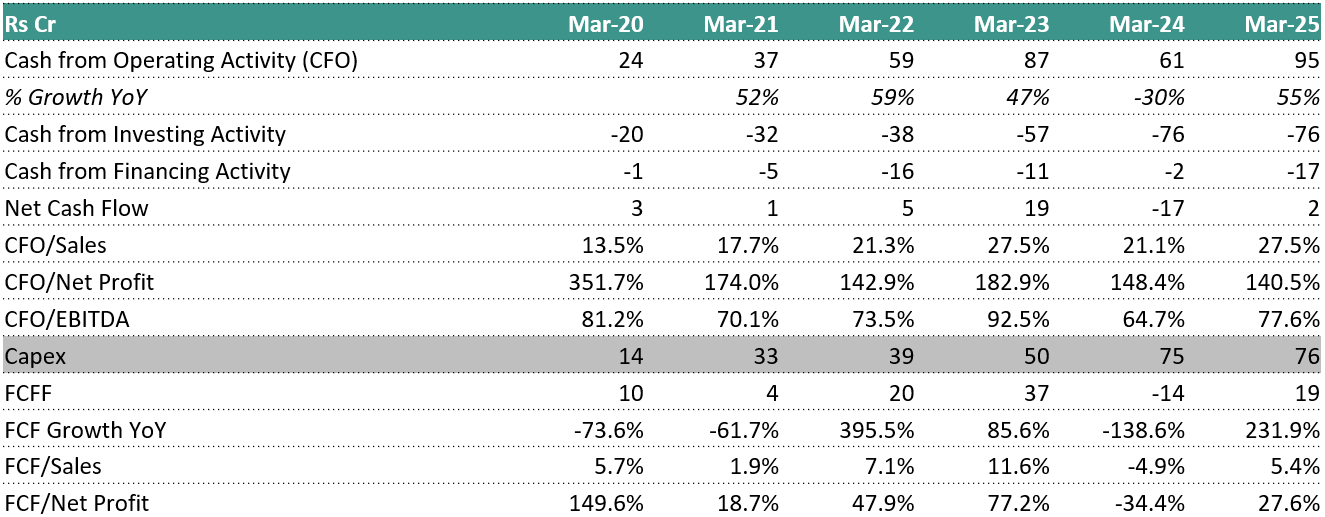

6.7 Cash Flow Analysis:

Operating cash flow has structurally strengthened, but with higher working-capital absorption. CFO rose from ₹61 cr in FY24 to ₹95 cr in FY25, tracking the jump in profit from operations (₹92 cr → ₹125 cr). However, this improvement came despite working capital remaining a drag (WC change –₹15 cr in FY24, –₹8 cr in FY25), driven mainly by receivables (–₹22 cr in FY25). This indicates growth is increasingly cash-generative but still front-loaded on receivables as volumes scale.

Capex intensity peaked in FY24–FY25 and is now clearly visible in investing cash flows. Investing cash outflow expanded to –₹76 cr in both FY24 and FY25, almost entirely due to fixed-asset purchases (–₹77 cr in FY24, –₹79 cr in FY25). This confirms management’s stance that the last two years were infrastructure-heavy, particularly around Genome Valley and capacity build-out.

Financing cash flows show deliberate balance-sheet conservatism. Despite rising scale, financing cash flow stayed negative (–₹2 cr in FY24, –₹17 cr in FY25). Borrowings were modest (₹9.17 cr in FY24, ₹5.87 cr in FY25) and largely offset by repayments (–₹5.17 cr, –₹16.79 cr). This shows growth is being funded primarily through internal accruals, not leverage.

Dividend payouts continued even during peak capex years. Vimta paid dividends of ~₹4.4 cr annually in FY22–FY25, including FY24 and FY25, signaling management confidence in cash sustainability despite heavy investment.

Net cash flow volatility reflects timing, not stress. Net cash swung from +₹19 cr in FY23 to –₹17 cr in FY24, then back to +₹2 cr in FY25. This mirrors the capex cycle rather than operational weakness, reinforcing that cash compression in FY24 was investment-driven, not earnings-driven.

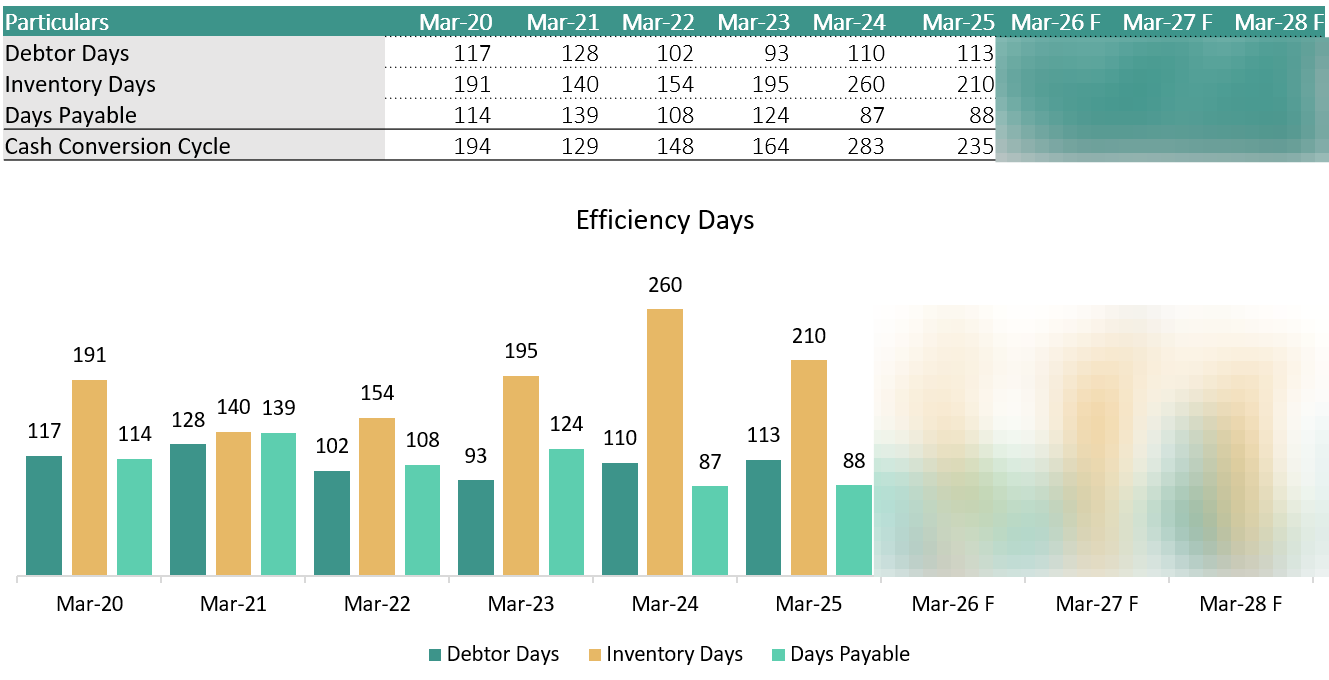

6.8 Cash Conversion Cycle:

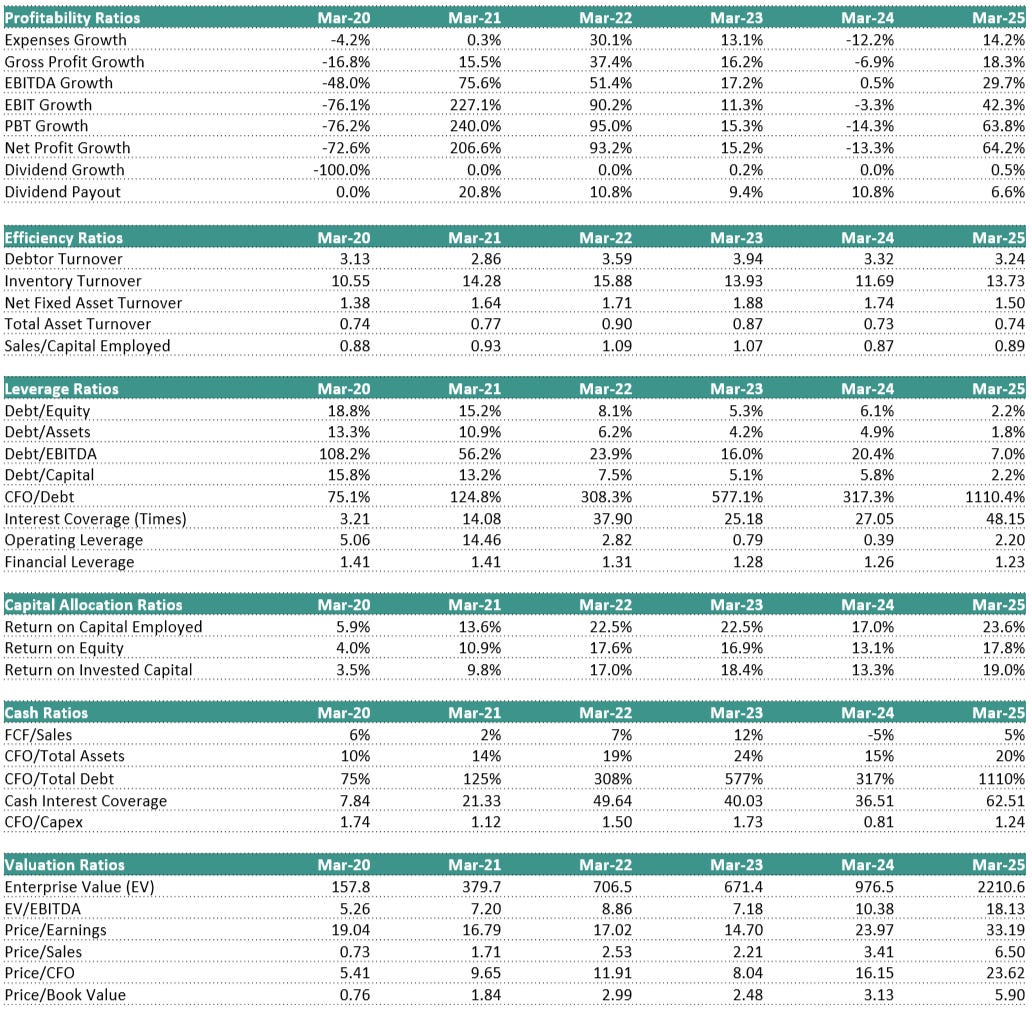

7. Key Ratios:

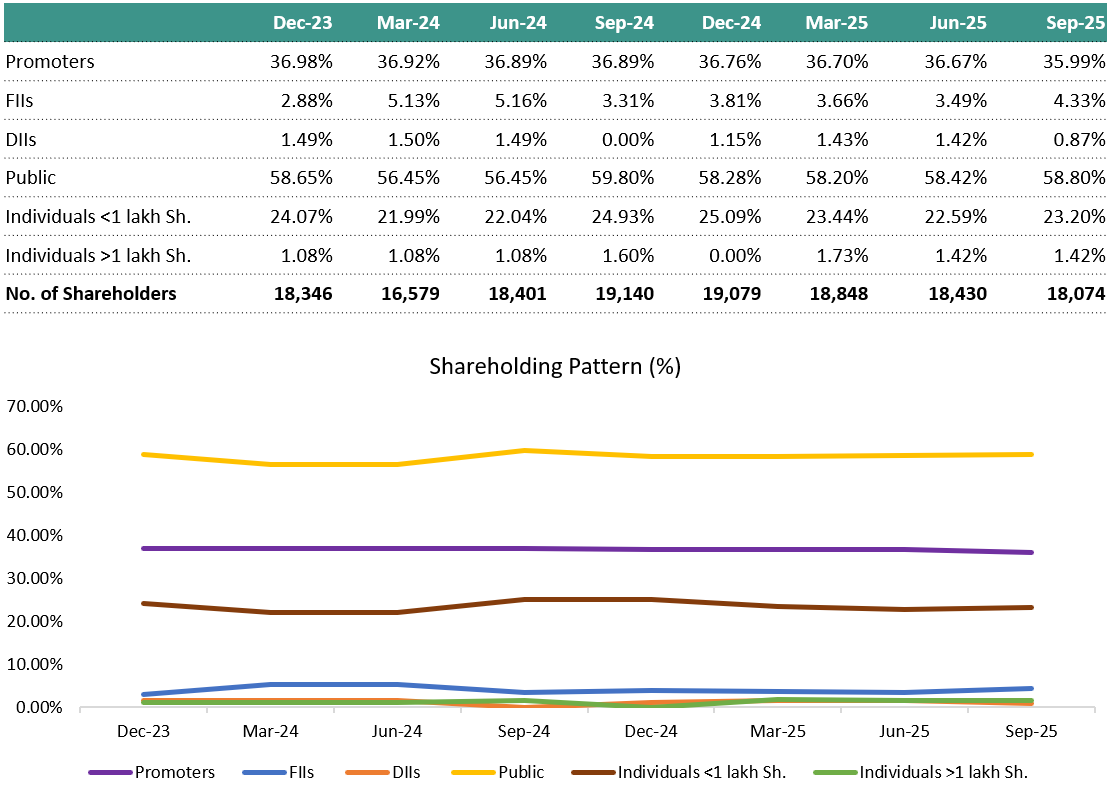

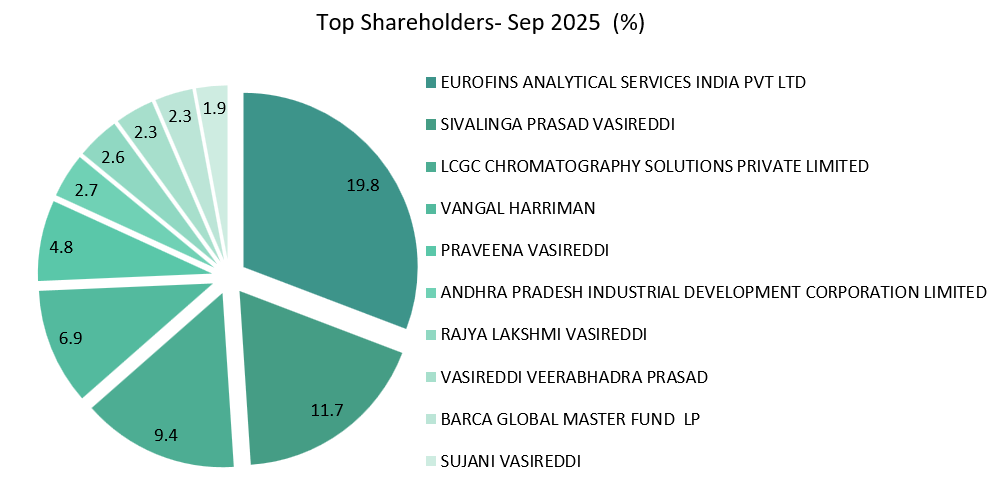

8. Shareholding Pattern:

9. SWOT ANALYSIS:

Strengths

Dominant Market Positioning & Brand Equity: The company holds the #1 position in India for both Pharmaceutical Analytical testing and Food Testing. It maintains a client portfolio comprising 90% of India’s top 20 pharmaceutical companies and 7 of India’s top 10 food companies. It possesses a long operational track record of 41+ years (established in 1984), creating high barriers to entry regarding trust and data integrity.

Massive Infrastructure & Integrated Capabilities: Operations are supported by ~600,000 square feet of ultra-modern laboratory space. It operates a Gold LEED-certified Vivarium, essential for high-quality pre-clinical research. The business model is highly diversified across four distinct verticals: Pharma (Pre-clinical, Clinical, Analytical), Food & Agri, Electronics, and Environment, reducing dependency on a single service line.

Superior Regulatory Accreditations: It was the first company in Asia to be pre-qualified by the WHO (2008). It serves as the National Reference Laboratory for the FSSAI (Food Safety and Standards Authority of India) and operates the National Food Lab at JNPT under a PPP model. It is the only private lab in India approved by the EU for Guar gum testing. Facilities are inspected/accredited by global bodies including USFDA, UK-MHRA, and EMA, enabling acceptance of their data in over 100 countries.

Strategic “One-Stop” Provider: The company has integrated backward to offer end-to-end services in biologics, covering everything from cell line development (upstream) to formulation development and analytical testing, positioning it as a comprehensive partner rather than just a testing vendor.

Weaknesses

Geographic Concentration of Key Verticals: While the company has a presence in multiple cities, the high-tech Electrical & Electronics (E&E) testing is currently limited to a single location (Hyderabad). The central laboratory infrastructure is heavily concentrated in Hyderabad, creating a single-point operational risk in case of localized disruptions.

Underutilization of New Capacities: Recent infrastructure expansions (referred to as Phase 1 and Phase 2) are not yet fully optimized. Specifically, the Phase 2 facility currently reports utilization rates of 50% to 60% of the additional space created, indicating a lag between capital deployment and full operational efficiency.

High Capital Obsolescence Risk: The business requires continuous technology refreshes to handle smaller molecules and complex biologics. The company faces a structural necessity to constantly replace instrumentation due to technological obsolescence and strict regulatory requirements, rather than just for capacity expansion.

Niche Perception in Defense/Electronics: Despite entry into the defense sector 2.5 years ago, this segment remains a niche area compared to the established Pharma and Food divisions, requiring significant effort to increase visibility and market share against specialized incumbents.

Opportunities

Shift to Large Molecules (Biologics): The global pharmaceutical industry is pivoting toward large molecules (biologics, vaccines, peptides). The company is capitalizing on this by setting up Formulation Development services specifically for biologics, with commercialization targeted for Q1 FY27.

Geopolitical Tailwinds (Biosecure Act): The passing of the BIOSECURE Act and the “China Plus One” strategy are driving global demand toward India. Top 5 to 6 global biotech giants (including names like Merck, Sanofi, and Amgen) are establishing manufacturing or clinical centers in India, creating immediate demand for independent third-party analytical testing.

Evolution of Clinical Research: There is a shift from healthy volunteer studies to patient-population studies conducted in hospital setups. The company has successfully completed its first full-scale trial in this domain and initiated 2 new studies, opening a new revenue stream without requiring heavy capex (as these are off-site/hospital-based).

Domestic Regulation & “Make in India”: Stricter enforcement by FSSAI and increased consumer awareness regarding product safety (protein content, sugar levels) are driving higher testing volumes. Government push for Electric Vehicles (EVs) and increased defense budgeting is generating demand for EMI/EMC and reliability testing.

Outsourcing Trends: As major pharma companies establish “fill and finish” centers in India, the requirement for independent, third-party laboratory testing (mandatory for regulatory filing) is structurally increasing.

Threats

Strict Regulatory & Reputational Risk: The business operates under stringent GXP (Good Manufacturing/Clinical/Laboratory Practices) standards. Any adverse observation or “Form 483” from regulators like the USFDA or WHO could result in immediate suspension of operations and severe reputational damage, which is the core asset of a CRO.

Intellectual Property Secrecy by Innovators: Innovator companies (as opposed to generic manufacturers) often split their value chain across multiple vendors to protect IP. This limits the company’s ability to capture the “entire wallet share” of a single molecule’s development lifecycle, as clients are hesitant to house all development stages with one vendor.

Intense Competition: The company competes with massive international players such as Eurofins, SGS, Intertek, Bureau Veritas, and Charles River, who have deep pockets and global networks. Domestic Fragmentation the market also includes captive CROs owned by large pharma companies and specialized standalone clinical trial firms, creating pricing pressure.

Technological Disruption: Rapid advancements in analytical instrumentation mean that current testing methodologies can become obsolete quickly. Failure to adopt the latest testing technologies ahead of the curve could result in a loss of contracts to more tech-agile competitors.

10. Concall Analysis:

1. Company Overview & Business Segments

Core Business: A leading player in the contract research, testing, and manufacturing services space.

Key Business Verticals:

Pharmaceutical Research & Testing: The largest contributor, providing preclinical, clinical, and analytical research and testing services. Accounts for ~65% of total revenue.

Food Testing: The second-largest vertical, contributing ~20% of total revenue.

Electrical & Electronics Testing: A smaller but stable vertical.

Environmental Testing: The smallest vertical with relatively lower margins.

Strategic Direction: The company is focused on harnessing emerging opportunities driven by tightening quality norms, technological advancements, and growth in the wellness sector. It maintains a net debt-free balance sheet.

2. Key Strategic Initiatives & Capex

Biologics CRDS (Contract Research & Development Services): This is the most significant new strategic initiative.

Status: The project is on schedule. Equipment has been ordered, and the facility is expected to be ready by the end of Q3 FY26.

Commercialization Timeline: Expected to be commercialized by Q1 FY27.

Capex: An outlay of ~₹25 crores is planned for this year, with a similar amount for next year.

Strategy: The goal is to become a one-stop provider for biologics clients by backward integrating from their existing analytical expertise into formulation development. This completes the “whole life-cycle” for large molecule services.

Capacity Expansion:

Phase 1 & 2: New facilities have been created, and while already partially commercialized (50-60% of additional space is in use), full utilization will ramp up from Q1 FY27.

Management confirmed there are no immediate capacity constraints and that the expanded infrastructure will support growth for the next few years.

Divestment of Diagnostics: The company divested its diagnostics and pathological services business on August 30, 2024. The reported financials have been regrouped for a like-for-like comparison of the core business.

3. Business Outlook & Market Dynamics

Growth Drivers: Future growth is expected to continue being led by the pharmaceutical and food testing services, which form the largest part of the revenue pie.

Competitive Landscape: The company competes with a mix of domestic and international players.

Food: Competitors are primarily large multinational CROs with a presence in India, such as SGS, Eurofins, Intertek, and Bureau Veritas.

Pharma: Competes with Indian counterparts and European/American CROs in the overseas market.

Market Growth vs. Company Growth: The underlying market growth for Vimta’s sectors is estimated at 7.5-9%. The company’s consistent growth of 20-25% indicates it is successfully gaining market share from competitors and capturing new business in overseas markets.

Domestic Pharma Environment: Management sees no slowdown or adverse regulatory changes in the domestic pharma landscape. The trend of MNCs setting up fill/finish centers in India and the growth in complex product development (biologics, peptides) is increasing the demand for independent testing laboratories.

BIOSECURE Act: The passing of the act has led to top global biotech companies (Merck, Sanofi, Amgen, etc.) announcing plans to set up manufacturing or clinical centers in India. This is a positive for Vimta, as it will increase the demand for third-party CRO testing.

4. Key Q&A Insights

No Forward-Looking Guidance: Management reiterated its policy of not providing specific forward-looking revenue or margin guidance. However, they did state that the current high PAT margins of ~19% are “very good,” and they “don’t expect to see higher ones.”

Clinical Services: The clinical services business, which has been running for 33 years, is seeing a strategic shift. While it started with healthy volunteer studies, the focus for the last four years has been on patient population studies, which are conducted off-site at hospitals and are less capital-intensive.

Capex Details: Total capex for the first half of FY26 was ₹47 crores. This has been spent across the pharmaceutical, food, and electrical & electronics verticals.

Biologics Capabilities: Vimta has existing analytical capabilities for biologics (developed over the last 7-8 years). They are now building capabilities for cell line and formulation development to offer an integrated package. The recent US FDA draft guideline allowing biosimilar approval with only analytical testing is a positive development that aligns with Vimta’s strengths.

Defence Business: The company has been supporting defense industries for over two years and is continuously adding more clients. This is considered a “niche testing area” with a margin profile similar to other electronics testing.

Small Molecule vs. Large Molecule: The majority of Vimta’s current pharma business is in generic product development (small molecules). The strategic move into biologics CRDS is to ensure they “don’t miss the bus on large molecules.”

11.1 Growth Drivers:

Biologics CRADS: Entry into High-Value Large Molecule Lifecycle

Setting up Biologics Contract Research & Development Services (CRADS) with ~₹50 crore capex over FY26–FY27, with commercialization targeted from Q1 FY27. Builds on 7–8 years of existing biologics analytical capabilities, reducing execution risk versus greenfield entry.

Positions Vimta as a one-stop provider across analytics, preclinical, clinical, cell line development, and formulation development for large molecules.

Expected to become a new growth engine as biologics typically command higher wallet share and longer client engagement cycles.

Sustained Market Share Gains in Core Pharma & Food Testing

Industry growth is estimated at ~7.5–9%, while Vimta has been delivering ~20–25% growth, implying continued market share capture dominant positioning with 90% of India’s top 20 pharma companies and 7 of India’s top 10 food companies as customers.

#1 position in pharma analytical testing and food testing in India, creating scale advantages and strong client stickiness.

Regulatory-driven demand (USFDA, WHO, EMA, FSSAI) favors large, compliant, trusted labs, raising entry barriers for smaller players.

Capacity Expansion Already in Place, Enabling Scalable Growth

Phase 1 and Phase 2 infrastructure expansions completed, with 50–60% of incremental capacity already utilized. Management has explicitly stated no near-term capacity or space constraints, supporting multi-year growth visibility.

Incremental capacity spans pharma, food, electronics, preclinical, and GMP testing for small and large molecules, ensuring balanced growth.

This readiness enables Vimta to absorb large client orders quickly, especially from MNCs setting up operations in India.

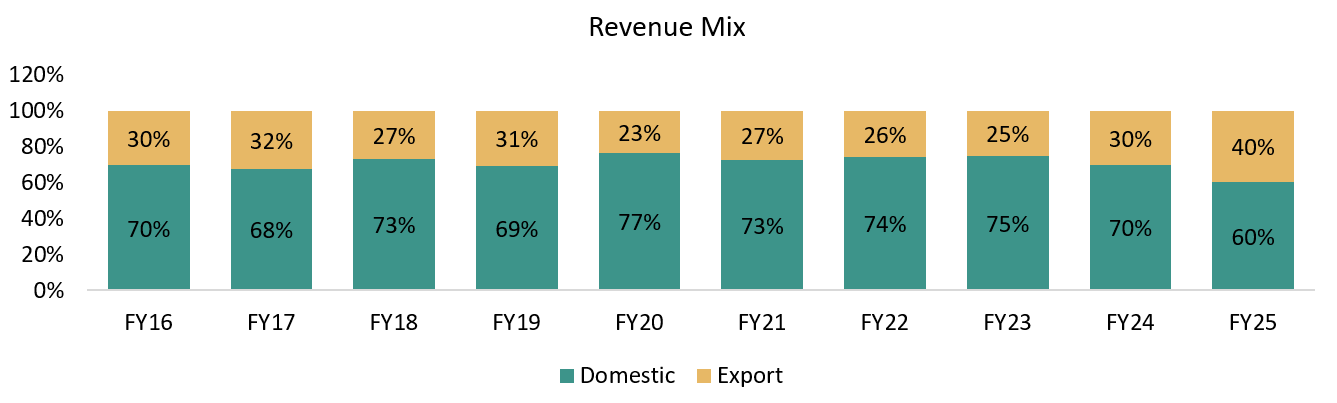

Overseas Business Expansion Driven by Regulatory & Geopolitical Shifts

Overseas revenues already contribute ~30%+ of total revenues, with management confirming a gradual upward trend. Beneficiary of the BIOSECURE Act and China+1 strategy, as global innovators set up manufacturing and clinical operations in India.

Management has confirmed active engagements and discussions with global innovators such as Merck, Sanofi, Amgen, Lilly, J&J, and GSK.

Innovator companies structurally require independent third-party CROs for analytical and CMC testing, benefiting Vimta’s neutral positioning. Increased overseas business development spend reflects management’s intent to scale international revenues sustainably.

Early-Mover Advantage in Defense & Electronics Testing

Defense electronics testing has been ongoing for 2–2.5 years, indicating continuity rather than pilot projects. Capacity in electronics testing has recently been doubled, positioning Vimta for incremental order inflows.

The government's focus on Make in India, defense indigenization, EVs, and electronics manufacturing supports steady demand.

Margins are broadly similar to electronics testing, adding growth without diluting profitability.

11.2 Risks/ Challenges:

Sustained High Margin Profile May Be Difficult to Defend at Scale

Current margins of ~35% EBITDA and ~19% PAT have been explicitly described by management as “very good,” with no expectation of further expansion.

Ongoing investments in manpower, overseas business development, technology upgrades, and biologics ramp-up could exert cost pressure ahead of revenue scaling.

Any slowdown in revenue growth, especially in high-margin pharma analytical services, could lead to negative operating leverage. Environment testing and newer service lines structurally carry lower margins, which could dilute blended profitability if their share increases faster than expected.

Competitive Intensity from Global and Domestic CROs

Vimta operates in a market with well-capitalized global competitors and increasing domestic capacity. Competes directly with large multinational CROs such as SGS, Eurofins, Intertek, Bureau Veritas, Charles River, and Covance, which have deeper global networks.

Innovator clients often split work across multiple CROs to protect intellectual property, limiting Vimta’s ability to capture the full lifecycle wallet share.

Aggressive pricing or bundled offerings by global peers could pressure realization, especially in overseas markets. Domestic competition from captive CROs owned by large pharma companies may restrict growth in certain service segments.

Dependence on Pharma and Food Verticals for Growth Momentum

Vimta’s revenue growth is heavily concentrated in a few core segments, creating concentration-related risks. Pharma (~65%) and food testing (~20%) together account for ~85% of revenues, making overall growth sensitive to demand trends in these verticals.

Any slowdown in generic product development activity, regulatory filings, or food compliance enforcement could disproportionately impact topline growth.

Smaller verticals such as environment and electronics testing are not yet large enough to fully offset any softness in the core segments. Diversification benefits from newer businesses will materialize only gradually, limiting near-term downside protection.

Slower-than-Expected Conversion of Overseas Pipeline

While overseas markets are a key growth driver, execution risks remain around conversion and scalability. Management has indicated increased overseas business development spend, which raises fixed costs ahead of revenue realization.

Overseas client onboarding cycles are typically longer due to regulatory qualification and audit requirements, delaying monetization.

Intense competition from established global CROs may limit win rates or pricing power in international tenders. A weaker-than-expected conversion of overseas discussions could pressure margins without delivering proportional revenue growth.

Client Concentration and Key Account Risk

A significant portion of revenue is derived from large pharmaceutical and FMCG clients, many of whom account for sizable individual engagements.

Large clients often have strong negotiating power, which could impact pricing or contract terms over time. Loss or downsizing of even a few marquee clients could lead to short-term revenue volatility, especially in high-margin analytical services.

Client decisions to insource certain testing activities could affect repeat business volumes.

12. Competitors:

12.1 Syngene International Ltd.

Market Cap: ₹ 26,262 Cr.

Syngene International Ltd., incorporated in 1993 and headquartered in Bangalore, is a leading contract research and manufacturing organisation (CRAMS). It provides integrated discovery, development, and manufacturing services to global biotech, pharmaceutical and agrochemical companies. Syngene operates across small molecules, biologics, cell therapy, and synthetic chemistry domains.

Business Model:

Syngene operates a research-plus-manufacturing services model, partnering with multinational and domestic life-sciences companies. It offers end-to-end capabilities from early discovery support to late-stage development and commercial supply. Revenue is driven by long-term research contracts, milestone-linked development fees and manufacturing agreements. The company’s flexible infrastructure including discovery labs, analytical facilities and GMP manufacturing plants supports scalable client projects on a fee-for-service and success-sharing basis.

What sets them apart:

End-to-End Integrated Services: Offers a comprehensive stack from drug discovery to commercial manufacturing a rare one-stop CRAMS platform in India.

Global Client Base & Partnerships: Strong relationships with global pharma and biotech players; long-term alliances, including multi-year contracts with large pharmaceutical companies.

Capability Across Modalities: Expertise spans small molecules, biologics, peptide synthesis, cell therapy, and advanced analytics allowing participation in cutting-edge therapeutic areas.

12.2 Thyrocare Technologies Ltd.

Market Cap: ₹ 6,895 Cr.

Thyrocare Technologies Ltd., incorporated in 1995 and headquartered in Mumbai, is a leading Indian diagnostic and preventive healthcare service provider. It operates a pan-India network and offers affordable, high-quality pathology and preventive health check-up services.

Business Model:

Thyrocare operates a hub-and-spoke model with a central high-throughput NABL/ISO-accredited laboratory in Navi Mumbai and a wide network of regional hubs and collection centres across India and overseas. It partners with hospitals, clinics, corporate clients and health-insurance firms while retaining strong direct-to-consumer reach through tie-ups with phlebotomists and collection points. The company also leverages technology platforms for sample tracking, digital reporting and preventive health analytics.

What sets them apart:

Centralised High-Throughput Lab: One of the first in India to use a central lab model at scale, improving quality, turnaround time and cost efficiency.

Preventive Health Emphasis: Large portfolio of preventive health packages encouraging early detection + chronic disease monitoring.

Strong Distribution & Tech Adoption: Extensive network of collection points nationwide and technology-enabled reporting (digital interfaces, apps), giving a broad reach even in smaller towns.

12.3 Krsnaa Diagnostics Ltd.

Market Cap: ₹ 2,343 Cr.

Krsnaa Diagnostics Ltd., incorporated in 2000 and headquartered in Gurgaon (Haryana), is an Indian diagnostics and pathology services company operating a wide network of laboratories and patient service centres. Krsnaa offers clinical lab testing, radiology diagnostics, preventive health check-ups, and specialised tests across urban and emerging markets.

Business Model:

Krsnaa runs a hub-and-spoke diagnostics network. It operates central high-throughput laboratories that process samples from collection centres and patient service centres (PSCs) spread across India. Revenue is generated from diagnostic tests, imaging services, preventive health packages, corporate tie-ups, and health-insurance collaborations. The company aims to expand deeper into Tier-2/3 markets through franchise/partner centres alongside its own outlets.

What sets them apart:

Wide Reach & Network: Extensive footprint with labs and collection centres across multiple states, helping tap both urban and underserved markets.

Integrated Test Portfolio: Offers broad diagnostic services lab testing, imaging, pathology, and special packages under one roof.

B2C + B2B Mix: Revenue from individual customers, corporates (employee health programs), and institutional tie-ups including health insurers diversifying demand sources.

Thank You So Much For Reading!!

Researched By- Naresh, Mayank and Vaibhav

All information is sourced from the company’s annual reports, Press Release, News Articles, GoIndiastocks.in, Screener.in, industry reports, and Economy Outlook reports.

Disclaimer: We do not recommend buying or selling any stock. You should consult your financial advisor before buying or selling any financial instrument.

We are Proud to Announce Our New Launch of the Premium services where we Deep-dive into the Business and back you up with Robust Research.

We Provide services for different Level of Investors. You can Email us directly to start your journey!