When we think of India’s growth story, we often imagine grand announcements, mega projects, and the sweeping rhetoric of trillion-dollar visions. But the real test of an economy doesn’t lie in speeches; it lies in cement, steel, and timelines. Over the last few years, India has been quietly shifting gears—moving from abstract plans on paper to visible execution on the ground.

This shift is powered by two forces working in tandem: the Centre designing a digital-first, capital-heavy infrastructure blueprint, and the states racing against each other to implement it better, faster, smarter. The result? A new map of Indian growth is emerging—shaped not by rhetoric, but by roads, factories, and power lines.

But there’s a twist in the tale. Just when the machinery begins to hum, the skies open up. The monsoon—our oldest economic variable—remains a stubborn disruptor, delaying projects, bunching output, and revealing flaws in execution. That’s why the next 6–12 months are not about new announcements but about execution under stress.

Let’s break this story down.

The Federal Catalyst: Gati Shakti and Industrial Corridors

Every growth story needs an anchor. For India, that anchor is PM Gati Shakti, launched in October 2021. Think of it as a ₹100 lakh crore digital control tower that integrates 16 central ministries and all 36 states and UTs onto one platform. The purpose is brutally simple: cut India’s notoriously high logistics costs (13–15% of GDP) down to below 10%.

This is not a fancy dashboard for bureaucrats to click through. It’s a GIS-layered, satellite-monitored tool that coordinates everything from highways to ports to industrial zones. For once, ministries are not working in silos; they are building with each other, not despite each other.

The second pillar is the National Industrial Corridor Development Programme (NICDP). If Gati Shakti is the planning brain, NICDP is the muscular body. Along dedicated freight corridors like the EDFC and WDFC, the government is building “ahead of demand” cities. These are plug-and-play industrial townships where companies don’t have to haggle over land or wait for clearances—the infrastructure is pre-built, waiting for business to arrive.

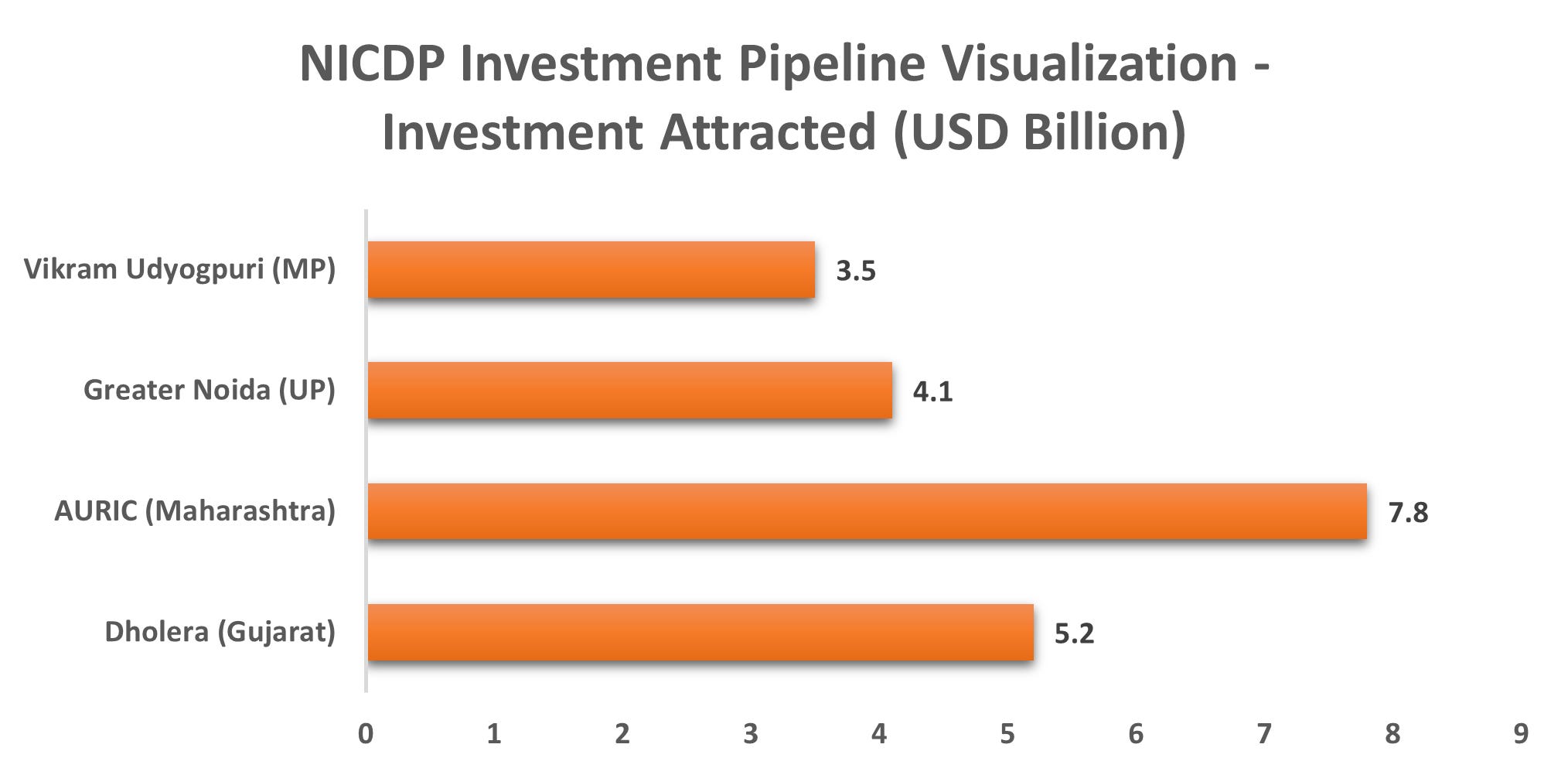

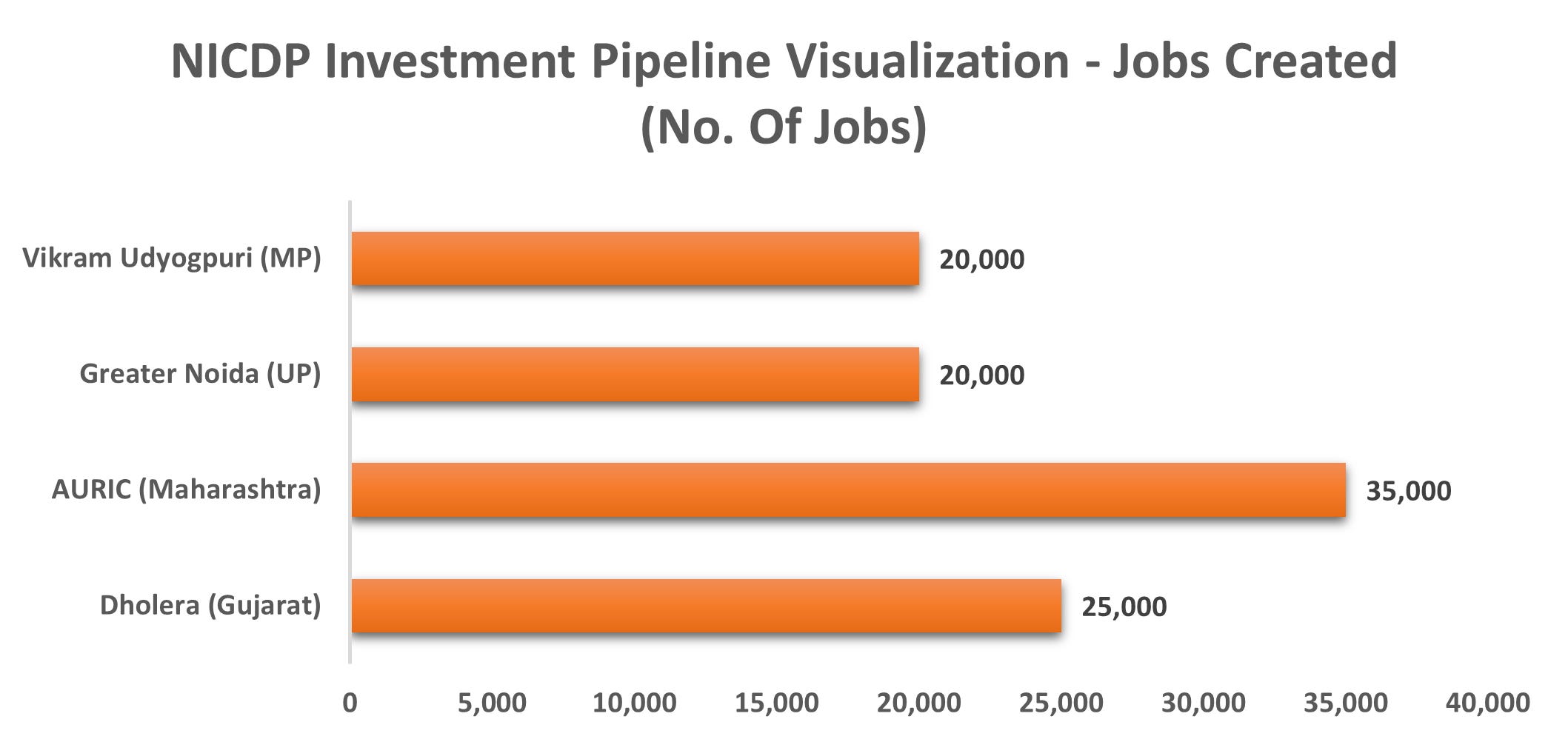

And business is arriving. Four early movers—Dholera (Gujarat), AURIC (Maharashtra), Greater Noida (UP), and Vikram Udyogpuri (MP)—have already pulled in $20.6 billion in investment and 100,000 jobs. In August 2024, another 12 projects worth ₹28,602 crore were approved, creating what policymakers like to call a “necklace of smart cities” along the Golden Quadrilateral.

This is federal orchestration at its most ambitious.

The State Stage: Where Announcements Meet Reality

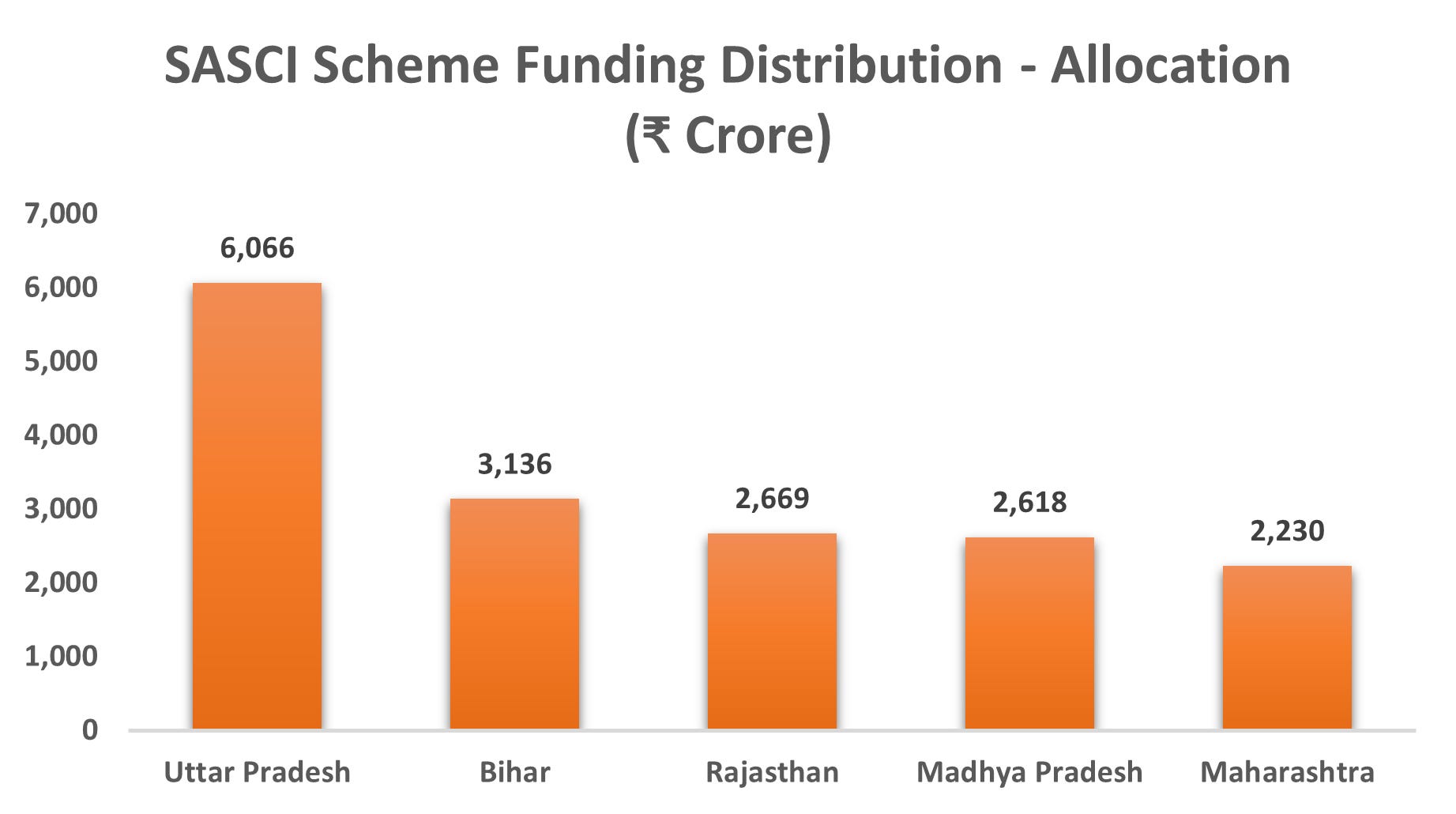

But here’s the real trick: Delhi can build plans and corridors, but only the states can make them breathe. That’s where the Scheme for Special Assistance to States for Capital Investment (SASCI) comes in. Instead of just writing cheques, the Centre now gives states 50-year interest-free loans, but with strings attached.

Want the money? Show us reforms. Integrate your property tax system. Build digital agri platforms. Improve urban planning. In other words, it’s not just about spending—it’s about learning how to govern better.

This creates a new race among states, a competitive federalism where the prize is both federal funding and private investment. Investors, after all, want competence. A state that shows it can convert announced projects into real, running factories earns credibility—and with it, more capital.

Take Uttar Pradesh. Long seen as a laggard, it is now turning into a case study. With 11.6% GSDP growth versus India’s 9.6% GDP growth, UP has climbed to second place in the Ease of Doing Business rankings. Its Defence Industrial Corridor has already attracted ₹28,762 crore, with 57 companies signed up across six nodes. Most impressively, from its Global Investors Summit, UP has actually converted 38% of promised investment into real projects—a rare follow-through in a country where announcements often evaporate.

This is the virtuous cycle: central push + state reforms → private investment → higher growth.

A Deep Dive: The Uttar Pradesh Story

When people think of Uttar Pradesh, the first images that come to mind are temples, farmlands, and political rallies. Rarely does one imagine aerospace factories, defence corridors, or plug-and-play industrial townships. And yet, over the past decade, UP has been quietly reinventing itself—from an agriculture-centric economy to a manufacturing-and-services powerhouse.

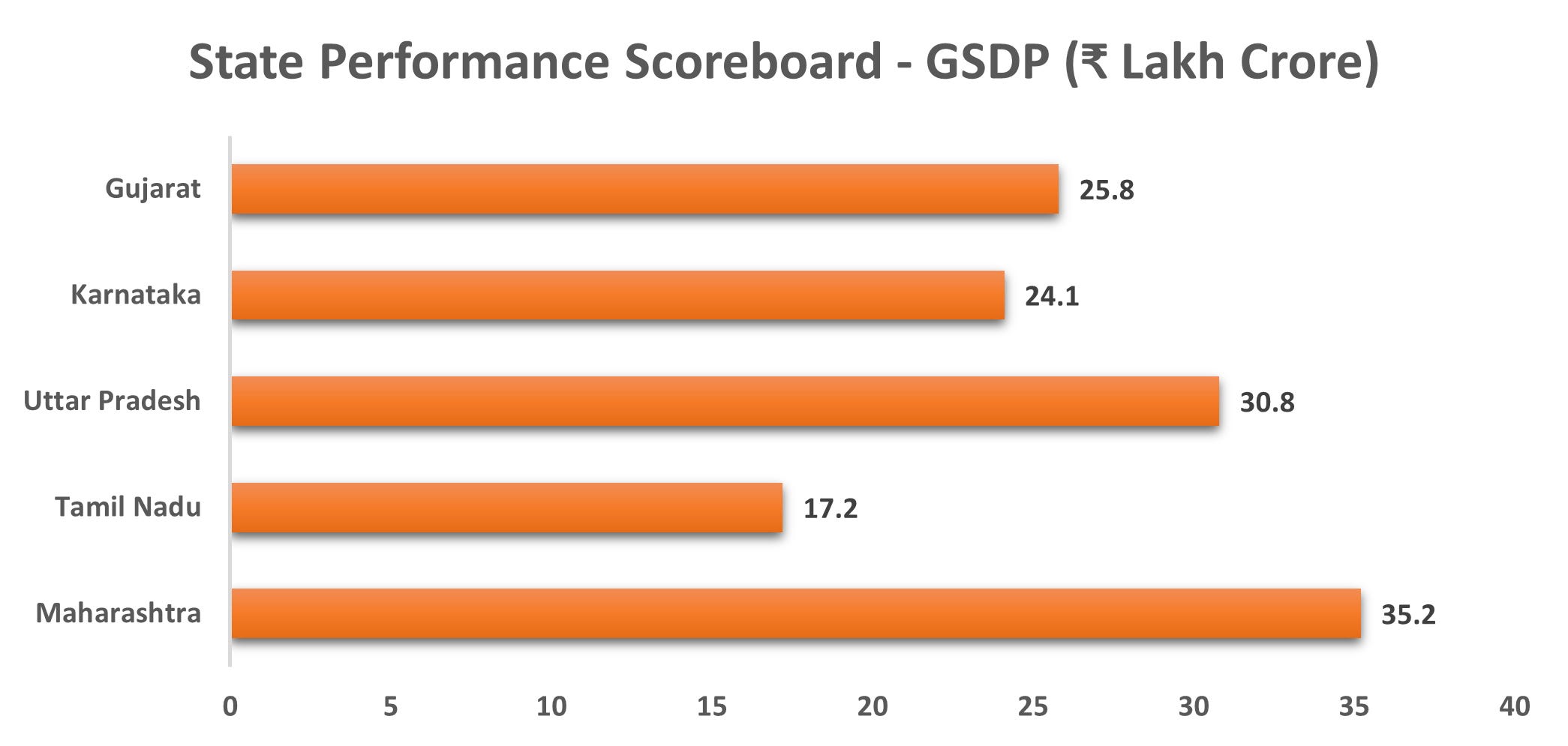

By 2025–26, UP’s economy is projected to touch ₹30.8 lakh crore, making it India’s third-largest economy. That’s no small leap. In 2017–18, the state’s GSDP was ₹12.89 lakh crore. By 2024–25, it had more than doubled to ₹27.51 lakh crore—outpacing India’s GDP growth at almost every step. The engine driving this acceleration? A cocktail of infrastructure spending and governance reforms.

The Confluence of Governance and Infrastructure

UP has done something many Indian states talk about but few deliver: it has put hard money behind its growth ambitions. In just five years, the state has committed ₹5.31 trillion in infrastructure capex, with its 2025–26 budget earmarking a hefty 20.5% of total spending for infrastructure.

The scale of projects is staggering. The Ganga Expressway, India’s largest greenfield expressway, is redrawing the state’s logistics map. The Multi-modal Logistics Hub (MMLH) in Dadri links UP’s industrial heartland to national freight backbones, slashing transport costs and creating new industrial clusters. The Integrated Industrial Township in Greater Noida—already operational—shows what “plug-and-play” really means: ready land, ready infrastructure, and ready investors.

Investors have noticed. Collectively, these projects have attracted over $20.6 billion, pulling UP into the same league as Gujarat’s Dholera or Maharashtra’s AURIC.

But roads and factories are only half the story. Governance is the other half—and here too, UP has rewritten the script. The Nivesh Mitra portal—a single-window digital platform—now handles 42 e-services, cutting land allotment e-auction timelines from 30 days to 15 days. Bureaucratic delays, long the bane of doing business in India, are being systematically attacked.

The state’s FDI Policy 2023 also reflects strategic thinking. Instead of a one-size-fits-all approach, it offers land subsidies of 30–50%, deliberately nudging investment into regions beyond Noida and Lucknow. The idea is not just growth, but balanced growth.

Quantifying the Promise-to-Project Pipeline

One of India’s biggest credibility gaps has been the gulf between announced investment and realized investment. Investment summits often throw up astronomical numbers, but ground realities tell another story.

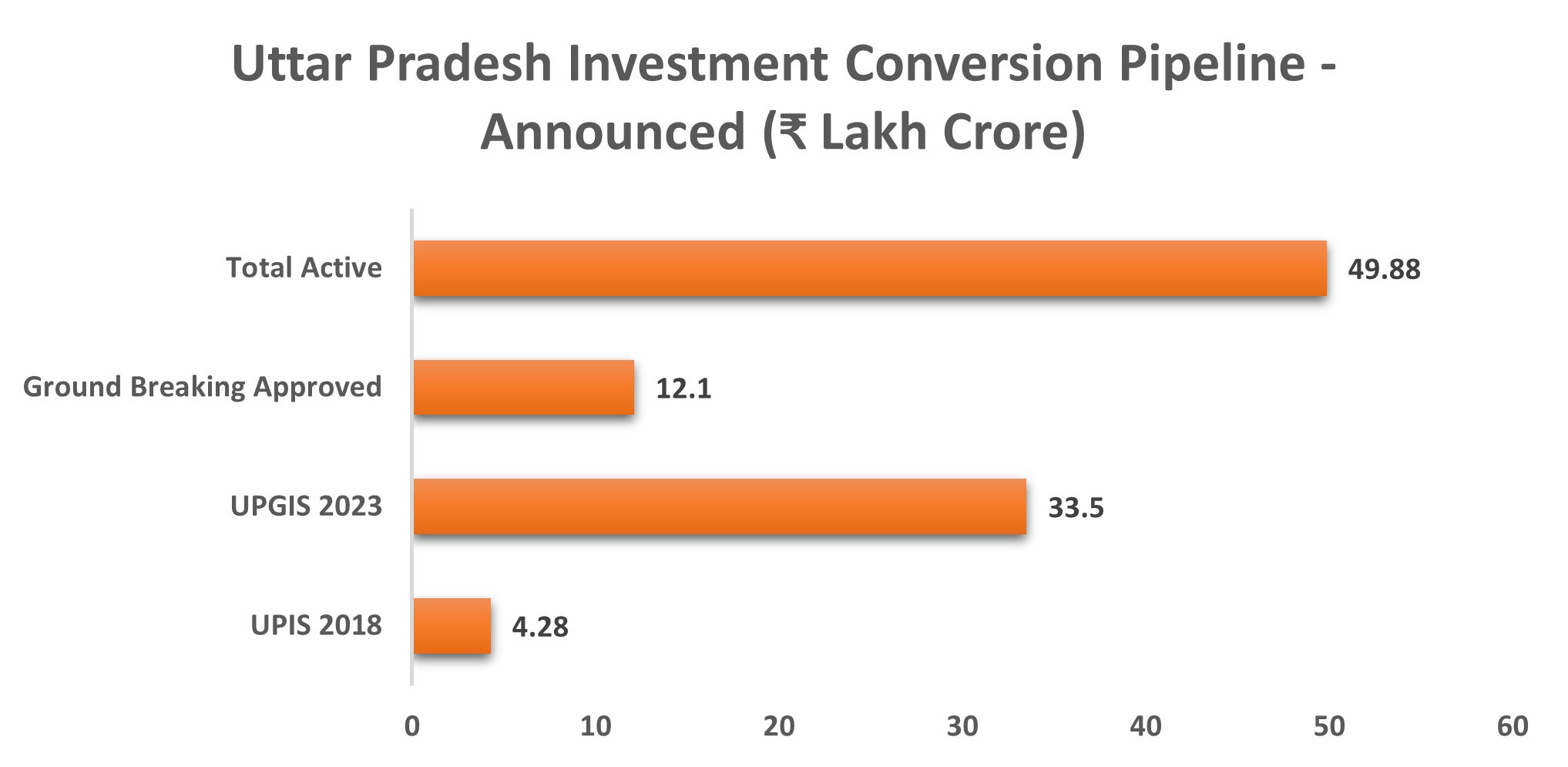

UP has tried to change this. After the UP Global Investors Summit (UPGIS) 2023, of the ₹33.50 lakh crore promised, the state has materialized ₹10.01 lakh crore. Groundbreaking ceremonies have been held for another ₹12.10 lakh crore. Out of this, projects worth ₹2.77 lakh crore are already in commercial operation.

That translates to a 38% conversion rate—the highest in the country. It’s a dry statistic, but it tells a dramatic story: UP is no longer just announcing; it is delivering.

Defence as the Growth Engine

One of the crown jewels of UP’s industrial story is the Defence Industrial Corridor. Spread across six nodes, it has already attracted ₹28,762 crore in investments.

Kanpur is leading the charge with ₹12,683 crore invested and already operational units.

Jhansi (₹6,853 crore) and Agra (₹2,888 crore) are under construction.

Lucknow, Aligarh, and Chitrakoot are at planning or partial operational stages.

In total, 923 hectares have been allotted to 57 companies, several of which have commenced production. By 2025–26, UP is targeting $25 billion in aerospace and defence production—a sector that India has long imported heavily but is now trying to indigenize.

This corridor does more than just attract investment—it anchors a high-value ecosystem of R&D, supplier networks, and skilled jobs.

Comparative Lens: How UP Stacks Up

But how does UP compare to other industrial powerhouses? Let’s look around.

Maharashtra remains India’s largest economy (₹35.2 lakh crore GSDP) and its undisputed FDI leader (31% share, $16.65 billion in FY25). It excels at mega-project execution—the Mumbai Trans Harbour Link is proof. But its challenge is de-concentration: moving growth beyond the Mumbai-Pune belt.

Gujarat, the export hub, contributes 8.3% of India’s GDP and handles 40% of national cargo. Its ports and logistics networks are unmatched. But it too faces the problem of reinvention. Ford’s exit in 2020 was a reminder that clusters can decay. Gujarat’s big bets now are in green hydrogen (₹40,000 crore by Welspun) and biotech (₹5,000 crore by Zydus).

Karnataka (₹24.1 lakh crore GSDP) and Telangana (₹12.8 lakh crore GSDP) are playing the tech card. With 12.1% and 8.3% of FDI share, respectively, they are magnets for IT, pharma, and innovation-led corridors.

Seen against this backdrop, UP’s rise is remarkable. It does not have Gujarat’s ports, Maharashtra’s finance capital, or Karnataka’s IT base. But what it does have is scale, political will, and a newfound reputation for execution. That makes it the wild card of India’s economic geography—an underdog suddenly punching at the weight of incumbents.

The Economics of Corridors: Why This Matters

Why should an investor or policymaker care about industrial corridors? Because they fundamentally change the math of doing business. Four channels explain this:

Transport Cost Cuts – Multi-modal connectivity and freight corridors shave logistics costs by 20–30%.

Time Compression – Faster cargo movement and better last-mile links shrink lead times.

Supplier Clustering – Firms co-locate, workers live near jobs, and costs drop through ecosystem effects.

Land Readiness – Pre-approved, plug-and-play land parcels mean less red tape and faster setup.

Add these together, and you get a simple truth: corridors turn location into a competitive advantage.

The Monsoon Test: Where Execution Meets Weather

But let’s not get carried away. Infrastructure in India has a long history of optimism meeting reality—and reality often wins. The monsoon is the most immediate reminder.

Between 62–85% of projects face weather-linked delays. This isn’t just about a few weeks of rain. It reveals something deeper: weak planning, fragile designs, and execution that struggles with stress. The result is staggered commissioning—projects bunch up into the later part of the year, creating spikes and troughs in output.

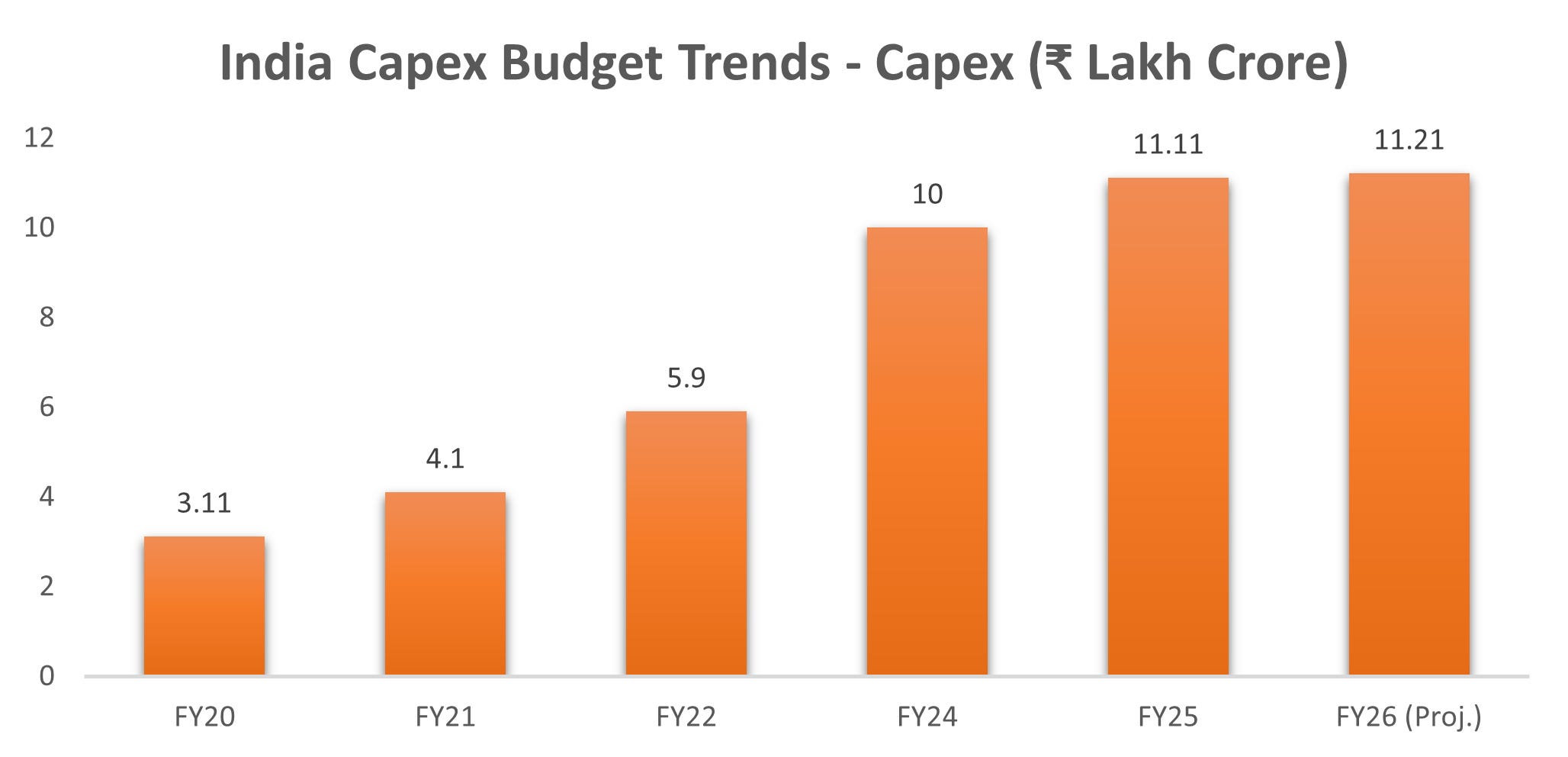

For 2025–26, India has penciled in ₹11.11 lakh crore of capex (3.4% of GDP). That’s a staggering commitment. But success won’t be measured by new announcements—it will be measured by how many ground-breaking ceremonies turn into factories running at full capacity despite the rains.

This is the critical inflection: if execution proves resilient against the monsoon, India graduates from being a country of grand plans to one of reliable delivery. If not, the cycle of delays will keep haunting us.

Mechanism of Delays

The monsoon season acts as a systemic risk factor for Indian infrastructure projects, directly impacting both cost and timing. At the construction site, critical activities such as excavation, foundation work, and concreting often come to a complete halt due to waterlogging, flooding, and worker safety concerns. Data from the Ministry of Road Transport and Highways highlights a 10–15% slowdown in highway construction during peak monsoon months.

These delays extend beyond the site itself:

Flooding disrupts logistics, especially the last-mile transport of aggregates, cement, and steel.

Moisture damage to inputs like wood and cement raises replacement costs.

Hot-mix plants and equipment failures during heavy rains force shutdowns.

Worker safety constraints lead to lower productivity even on non-rain days.

Together, these factors impose a hidden cost burden on contractors, who must account for idle time, damaged material, and deferred payments.

Evidence from the Field & Estimated Slips

Ground-level reports confirm that monsoon-related risks are not merely theoretical but materializing in high-priority projects.

Ganga Expressway: While the main route is largely complete, heavy rains have delayed interchange construction. Officials now target a November 2025 launch, slipping past earlier schedules.

Bengaluru–Mysuru Expressway: Severe waterlogging during pre-monsoon showers exposed design flaws and poor drainage systems. This shows that delays arise not only from rainfall but also from a lack of climate-resilient planning.

Sarai Kale Khan RRTS Station: Missed its June deadline; construction was still underway in July, despite being a flagship project.

Corporate Capex: Tata Chemicals noted a “softer Q2” due to monsoon disruptions, with volume and margin recovery expected in Q3–Q4.

NHAI Projects: A Ministry of Finance note recorded a temporary dip in capital expenditure in August 2024 due to heavy downpours.

On average, a 1–3 month pause in civil works translates into a 4–8 week delay in project commissioning.

The Indian growth story is entering a new phase. The Centre is no longer just a spender; it is an orchestrator, tying funds to reforms. States are no longer passive recipients; they are competitors, racing to execute faster and better. And private investors are no longer just spectators; they are partners drawn into this virtuous cycle.

But the real story isn’t in Cabinet approvals or ribbon-cutting ceremonies. It’s in the muddy fields where monsoon clouds test the strength of our designs. Over the next 6–12 months, the scoreboard won’t be measured in new MOU signings, but in concrete, steel, and power plants actually humming with activity.

For policymakers, the lesson is to keep focusing on granular execution. For investors, the signal is to watch not what’s announced, but what’s delivered.

India’s new investment map is being drawn, not in Delhi’s corridors of power, but in the industrial corridors crisscrossing its states. The question is whether we can draw it straight—or whether the rains will keep smudging the lines.

Sources- KPMG, PIB, TOI, HT, PIB, India.gov, IBEF, PIB, InvestIndia.gov, psrIndia, InvestIndia, DeccanChronicals, PIB, Kirtanepadit, TOI, Swarajyamag, cgihamburg.gov, FinancialExpress, ET.

Piramal Pharma is not a one-trick story. It combines:

A trusted partner for pharma companies making complex, high-value drugs,

A global leader in critical hospital medicines, and

A recognizable consumer healthcare brand house in India.

The company faces near-term bumps, but with world-class compliance, global scale, and investments in next-gen therapies, it has a credible shot at achieving its FY2030 vision.

For investors, that could mean meaningful upside if execution stays on track.

https://stocklens.substack.com/p/piramal-pharma-a-global-three-in