The Great Financial Convergence

Why the Digital Economy is Quietly Becoming a Banking Layer

When Every Shopkeeper Starts Asking About Your Salary

There was a time when you went to a bank only for bank-like things. You deposited money, withdrew cash, maybe argued with a form, and returned home slightly older than when you entered. A food app delivered food. A taxi app booked rides. A shopping app sold products. Each business stayed politely inside its lane.

That world is disappearing.

Today, almost every app you open seems to have developed the financial curiosity of a neighbourhood uncle. Order dinner, and it asks if you want “Pay Later.” Book a cab, and suddenly there is insurance attached to your trip. Buy groceries, and the platform gently nudges you toward cashback wallets, EMI offers, or credit products. Scroll through a commerce app, and somewhere between toothpaste and detergent, you may be offered digital gold or mutual fund investments.

At first glance, this feels like convenience. But underneath that convenience lies one of the biggest structural shifts in the digital economy: platforms no longer want to merely sell services. They want to become financial layers. In simpler terms, every app increasingly wants to behave a little like a bank.

And if you are wondering why your grocery app is suddenly interested in your borrowing habits, the answer is simple: transactions may bring customers, but financial behaviour brings profits.

From Utility Apps to Financial Ecosystems

Think of the early internet as a mall of specialized shops.

One app did messaging. Another did transport. Another sold books. Another streamed music. Each digital company had a narrow job. Their business models were mostly built around fees, subscriptions, commissions, or advertising.

But mature digital economies rarely stay narrow.

As user growth slows, platforms hit a painful reality: there are only so many people to acquire. Once the market saturates, the battle shifts. Firms stop competing merely for downloads and attention. They begin competing for something deeper the user’s financial life.

Why? Because owning a customer’s payment flow is more valuable than owning a one-time transaction.

If a platform knows what you buy, when you buy, how often you buy, whether you delay payments, what ticket size you prefer, how sensitive you are to discounts, and whether your spending spikes before salary day, it is no longer just observing a consumer. It is quietly building a behavioural credit file.

Banks once relied on branch visits, salary slips, collateral, and paperwork. Platforms now rely on digital footprints.

That changes everything.

The modern app is no longer just software. It is becoming a miniature financial institution disguised as convenience.

Why Transactions Are Becoming Less Valuable Than Data

For years, the digital economy celebrated transaction growth.

More orders. More rides. More payments. More clicks.

Volume was the trophy. But scale alone has limits.

A food delivery platform earns a thin commission. A commerce platform often fights razor-thin margins. Ride-hailing firms spend heavily to balance drivers, incentives, and pricing. Many digital businesses learned a hard truth: moving goods or services is expensive; moving money is often more profitable.

This is where financial convergence begins.

When a platform processes millions of transactions, it gathers something richer than revenue data.

And data reveals behaviour.

A customer who consistently orders groceries every Sunday may be low-risk. A merchant receiving stable daily payments may qualify for working capital credit. A driver with predictable income flows may be a candidate for micro-insurance. A shopper frequently buying on discount might be highly price-sensitive. Someone making late-night impulse purchases may simply be… human.

The joke aside, these patterns matter.

Traditional finance was built around balance sheets.

Digital finance is increasingly built around behaviour sheets.

That is why platforms are moving from commerce to credit, from payments to lending, from engagement to deposits, from user traffic to wealth management.

The transaction itself is no longer the destination.

It is the data trail.

India: The World’s Largest Real-Time Payment Laboratory

If this transformation had a testing ground, it would be India.

Few countries have built digital public infrastructure at this scale.

Through coordinated institutional work involving the Government of India, the Reserve Bank of India, and NPCI, India turned payments into something almost frictionless. The Unified Payments Interface (UPI) changed the economics of money movement.

Sending ₹10 to a tea seller now requires less effort than remembering your own ATM PIN.

That matters.

UPI did not simply digitize payments. It rewired financial behaviour.

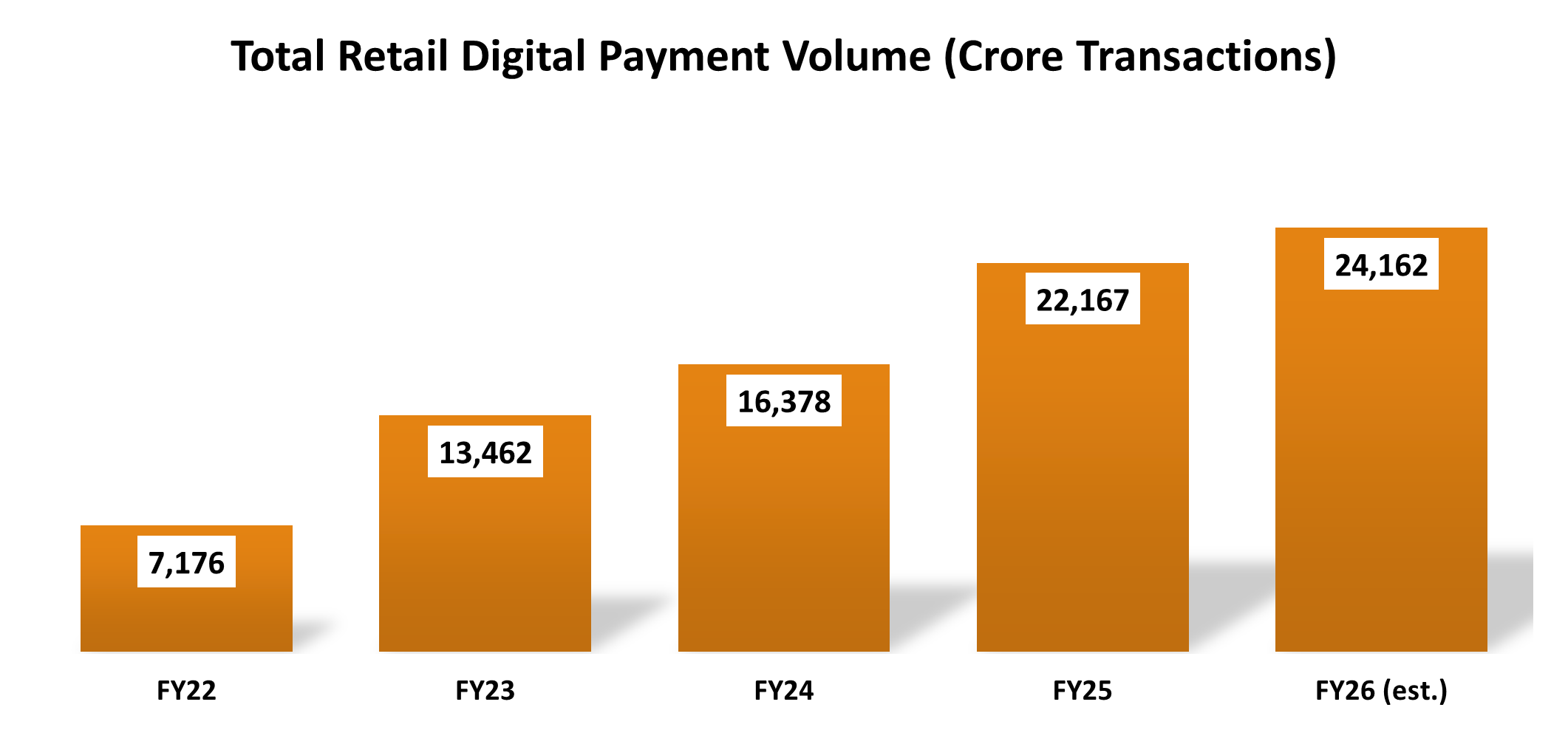

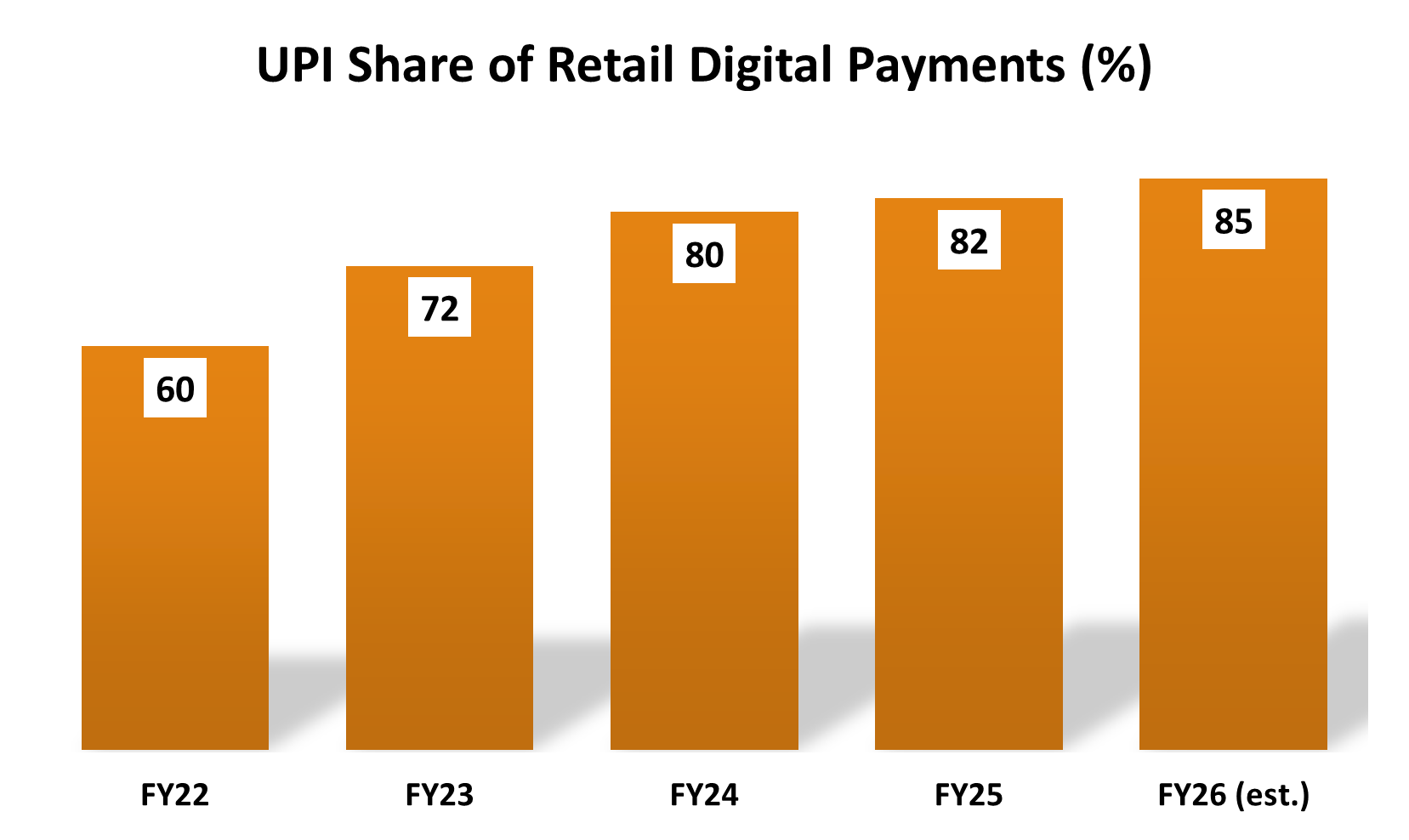

By FY 2024–25, UPI accounted for nearly 81% of all retail digital payments, making it the dominant retail payments infrastructure. Monthly transaction volume crossed 2,163 crore transactions in December 2025, an extraordinary number even by global standards.

To understand scale, consider the trajectory:

Digital retail payment volumes rose from roughly 7,176 crore transactions in FY22 to over 22,167 crore in FY25, while UPI’s share expanded steadily from around 60% to over 81%. By FY26, digital payment volumes were estimated near 24,162 crore transactions, with UPI moving toward an 85% share of retail digital payments.

That is not just payment growth. That is behavioural digitization.

Every scan, every transfer, every merchant settlement, every recurring bill creates an information layer. And once such a layer exists, financial products can sit on top of it.

Payments become rails. Finance becomes the cargo.

The Hidden Logic: Why Financial Services Became the Most Valuable Layer in the Digital Economy

If the earlier internet was about building digital storefronts, the modern internet is increasingly about building toll booths.

That is the hidden logic behind why every platform from food delivery to quick commerce to ride-hailing is inching toward finance.

At first, this may seem odd. Why would a company built to deliver biryani care about lending? Why would a grocery app suddenly want to sell insurance? Why would an e-commerce platform become obsessed with wallets, EMIs, or merchant credit?

Because their original businesses, despite scale and glamour, are often brutally hard ways to make money.

For all the excitement around digital platforms, many of their core businesses remain low-margin, highly competitive, and operationally exhausting. Delivering groceries sounds futuristic until you remember someone still has to pick the tomatoes, pack them, fuel the bike, manage spoilage, and reach your doorstep before you begin angrily tracking the rider after 8 minutes.

Convenience is expensive.

And logistics is even more expensive.

Take food delivery and quick commerce. These businesses run on thin spreads while carrying heavy variable costs—fuel, warehouse rentals, delivery labor, incentives, discounts, refunds, and infrastructure. Scale helps, but not always enough. Swiggy, for instance, reported a consolidated net loss of over ₹3,100 crore in 2025, despite generating more than ₹16,000 crore in revenue.

That single number tells an important economic story.

Revenue is not always profit.

And user growth is not always business quality.

For many digital firms, the platform itself increasingly functions less as a profit center and more as a customer acquisition engine a machine designed to capture attention, behaviour, and trust.

The real monetization opportunity often begins after the grocery basket is delivered.

Why Selling Money Is Often Better Than Selling Goods

A grocery order gives a company a one-time transaction. A financial product gives it a long-term relationship.

That distinction is enormous.

When a platform sells rice, soap, or a food order, it earns a small commission from a single purchase. But when that same platform offers credit, an EMI product, insurance, merchant lending, or wealth products, it enters a business with stronger economics.

The difference is almost unfair.

A physical product must be stored, transported, and fulfilled. A digital financial product, once built, can scale with very low marginal cost. A loan does not need packaging. An EMI does not require warehouse space. Insurance does not spoil in transit.

And a wallet balance does not need a delivery rider apologizing for traffic.

This is why financial services became the most attractive “business layer” in the platform economy.

They transform occasional usage into recurring monetization.

The Five Economic Incentives Behind Platform Financialization

The shift toward finance is not corporate experimentation. It is basic economics.

The first attraction is high margins. Unlike retail goods or logistics-heavy services, financial products can scale with near-zero marginal cost once digital infrastructure exists. A lending algorithm can underwrite one customer or ten million customers without proportionally increasing operational cost.

The second attraction is recurring revenue. Grocery orders fluctuate. Food delivery depends on habits, weather, discounts, and moods. But EMIs, subscription-based wealth products, insurance premiums, and loan repayments create predictable cash flows. Markets love predictability almost as much as investors love pretending they saw it coming early.

The third advantage is daily engagement. Wallets, UPI interfaces, and embedded payment tools bring users back into the app every day even when they are not ordering food or buying products. A platform that owns payment behaviour stays alive in the user’s routine.

The fourth advantage is stickiness. Once users hold an active EMI, merchant loan, salary-linked payment system, insurance cover, or investment product inside a platform, switching becomes painful. Convenience becomes dependence.

And finally, there is the most powerful asset of all: behavioural data.

Every payment, delay, repayment, recharge, order size, merchant settlement, and transaction pattern reveals something.

And information, in finance, is often more valuable than capital.

Why Investors Started Valuing the Financial Funnel More Than the Product

This explains an interesting shift in platform valuation.

Investors increasingly assign premium value not just to the visible business food delivery, shopping, logistics but to the hidden financial opportunities sitting inside that customer flow.

That is partly why high-frequency digital ecosystems like quick commerce became so strategically important.

Take Blinkit.

What looked like a grocery delivery engine was actually something deeper: a high-velocity user funnel.

Users return frequently. Basket sizes vary. Payment behaviour is repetitive. Demand patterns are rich. Merchant data accumulates rapidly.

That creates fertile ground for embedded finance.

By 2026, Blinkit’s valuation reportedly climbed to around $13 billion, even surpassing the implied valuation of some traditional delivery businesses around it.

The market was not merely valuing groceries.

It was valuing frequency, habit, and future financial monetization.

In digital capitalism, repeated user behaviour often matters more than the item being sold.

A toothpaste delivery may be boring.

A repeatable financial relationship built on that toothpaste purchase is not.

The Mathematics of Why Platforms Want Sticky Financial Users

At the heart of this shift lies a simple economic equation: customer lifetime value.

A transactional business earns only when a customer buys something.

That relationship is episodic. A customer may order food today and disappear for weeks.

In a traditional transactional model, profitability depends heavily on repeated purchases and thin margins. Customer value rises slowly because revenue comes only from isolated consumption events.

But a financialized platform changes the equation.

When a user adopts lending, insurance, wallet balances, subscriptions, or wealth products, the relationship becomes recurring. Revenue is no longer tied only to purchases. It becomes linked to financial behaviour.

And more importantly, churn falls. A user can uninstall a shopping app easily.

A user with an EMI, salary-linked wallet, recurring SIP, or active insurance policy is less likely to leave. That lower churn dramatically raises lifetime value.

This is why platforms are willing to make payment rails cheap or even nearly free. UPI, wallets, rewards, cashback, and frictionless payments are not always the final business.

They are often the doorway. Finance sits behind the door.

Why Data Is Becoming the New Collateral

Traditional banking relied on collateral.

Land.

Gold.

Salary slips.

Fixed deposits.

Documents thick enough to emotionally damage first-time borrowers. But this model excluded millions of people, especially in emerging economies.

Informal workers, gig workers, freelancers, micro-merchants, and thin-file borrowers often had income but lacked formal proof.

This created a classic economic problem: information asymmetry. The borrower knew their repayment ability. The lender did not.

Banks solved this through collateral and credit history. Platforms solved it through behaviour. That changed the lending model.

Instead of asking, “What property do you own?” The digital economy increasingly asks, “How do you behave?”

That is a radical shift.

Underwriting Risk Through Digital Footprints

In platform finance, behaviour becomes a proxy for trust. Every interaction turns into a signal. Purchase frequency may indicate stable income flow. Consistent utility bill payments can reflect repayment discipline.

Location stability may act as a proxy for employment or residential reliability. App usage behaviour may reveal financial maturity. Merchant settlement consistency may indicate working-capital quality.

Even device behaviour has been studied in risk modelling. Higher-end devices, updated operating systems, regular payment app engagement, and stable digital usage patterns can correlate with repayment reliability.

It sounds futuristic. Sometimes slightly creepy. Occasionally both.

But from an economic perspective, this is rational underwriting. A digital platform does not merely see a transaction. It sees probability.

In many cases, this allows lending to people traditional banks would classify as invisible. That is both financially powerful and socially significant.

Embedded Finance and the Rise of the Data Moat

This entire transformation has a name: Embedded Finance. At its core, it refers to financial products payments, lending, insurance, savings, and wealth management being seamlessly inserted into experiences that were never traditionally financial.

The user is no longer required to “go to a bank” in the conventional sense. Instead, the bank quietly arrives wherever the user already spends time.

It appears inside a grocery delivery app offering instant credit, inside a ride-hailing platform enabling wallet payments, inside an e-commerce checkout page suggesting EMI financing, or within a social commerce ecosystem nudging insurance or savings products. Finance stops being a separate destination and becomes an invisible layer embedded within everyday digital behaviour.

This convenience is not just a consumer feature; it is a powerful economic strategy. When financial products are integrated directly into high-frequency digital experiences, platforms gain access to scale at a speed traditional institutions often struggle to match.

A grocery app may begin by selling vegetables, but if it can also offer BNPL, insurance, or a pre-approved credit line, it transforms from a transaction platform into a financial gateway. The real asset is not merely the product being sold it is repeated user interaction.

That repeated interaction creates something far more durable than convenience: a data moat. Every payment, every order, every recharge, every repayment, and every behavioural signal adds to a growing intelligence layer around the user. The more people transact on a platform, the more data the platform accumulates.

The more data it accumulates, the sharper its underwriting models become. Better underwriting improves risk pricing, lowers default probability, and enables more personalized offers. Improved pricing then attracts more users, which generates even more behavioural data. The result is a self-reinforcing feedback loop a classic data network effect where scale continuously strengthens predictive power.

This is where traditional lenders face structural disadvantage. Banks may possess capital, regulatory depth, and institutional trust, but many still rely on static financial documents, historical credit scores, and relatively slower underwriting frameworks.

Platforms, by contrast, operate on live behavioural signals and real-time engagement. They understand not only whether a customer can repay, but often how that customer spends, moves, shops, subscribes, and behaves economically across daily life. In modern finance, velocity of information increasingly matters as much as the money itself.

Payments Are the Entry Point, Not the Business

If finance is the most profitable layer of the digital economy, then payments are the front door.

And like most front doors, they are not where the money is made.

This is one of the great paradoxes of modern fintech. Platforms today process extraordinary amounts of money, yet the payment itself often generates little or sometimes no direct revenue.

At first glance, that seems absurd.

Why would companies aggressively compete for a business that often earns almost nothing?

Why would firms spend billions on rewards, infrastructure, user acquisition, QR expansion, and payment rails if a simple scan-and-pay transaction barely pays?

Because payments were never meant to be the final business.

They were meant to be the entry point.

The Real Funnel Starts After the Payment

Modern fintech and digital platforms do not see payments as a revenue line. They see them as the first stage of a monetization funnel.

At the entry stage, products are often low-margin or nearly free. Peer-to-peer transfers, QR scans, wallet top-ups, and UPI payments create frequency. These are habit-building actions.

Then comes engagement.

Bill payments, mobile recharges, travel bookings, subscriptions, utility settlements, and merchant interactions deepen behavioural visibility. The platform learns what you spend on, when you spend, how regularly you spend, and how sensitive you are to timing.

Only then comes monetization. This is where the real economics begin.

A user may be offered BNPL credit, personal loans, merchant financing, insurance cross-selling, co-branded credit cards, or wealth products like mutual funds and gold investments.

And finally comes retention.

Once the user moves into SIPs, recurring payments, merchant services, salary-linked payments, or integrated credit behaviour, the platform becomes financially embedded.

The app is no longer just something you use. It becomes something your money depends on. That is a deeper relationship.

EMI, Autopay, and the Architecture of Inertia

Consider a user who buys a phone using EMI financing through a platform ecosystem. That customer is no longer making a one-time purchase.

They now have recurring repayments tied to that financial system. Leaving the ecosystem becomes harder.

Not impossible. But inconvenient. And convenience, in digital economics, often defeats intention.

Then comes UPI Autopay, which quietly became one of the strongest retention tools in platform finance. Subscriptions for OTT apps, insurance premiums, utility bills, SIPs, memberships, and recurring services increasingly operate on automated mandates.

Once set up, payments happen in the background. The user stops actively deciding. Behaviour becomes automatic. This creates consumer inertia.

A person is far less likely to cancel or switch providers if it requires manually revoking a mandate, resetting payment preferences, and rebuilding that system elsewhere.

Economists would call this switching cost. Users simply call it “I’ll do it later.”

Often, they never do. That is retention by design.

The Psychology of Stored Money

Another subtle retention mechanism is the stored balance.

Wallet ecosystems, cashback credits, and pay-later balances create a powerful psychological effect. If a user has ₹500 sitting in a platform wallet, they are more likely to return to that app than begin fresh elsewhere.

This is not just convenience. It taps into behavioural economics.

The endowment effect makes people value what they already “own” more than an equivalent alternative. Similarly, loyalty points create a mild version of the sunk-cost effect. Once users accumulate rewards, they keep transacting to justify what they already earned.

So money sitting in a wallet is not idle. It acts like emotional glue. Stored money creates stickiness. Sticky money creates repeat behaviour. Repeat behaviour creates lifetime value. That loop matters enormously.

Why Consumers Are Moving Toward Credit-Driven Ecosystems

India’s payment behaviour reflects this shift.

Between 2021 and 2025, credit card transaction volumes rose sharply—more than 2.6 times while debit card usage, particularly for basic withdrawal-led functions, declined significantly.

That movement tells a larger story. Consumers increasingly prefer instruments that offer credit, rewards, flexibility, cashback, EMI options, and financial layering.

A debit card mostly moves your money. A credit-linked ecosystem can lend, reward, insure, and integrate. Naturally, platforms prefer the second model.

Because the more financial layers added to a user, the deeper the ecosystem lock-in becomes.

Why Big Tech Wants Banking—Without Becoming a Bank

Here is where the story gets more interesting. Most major digital platforms do not actually want to become full banks.

That may sound surprising. After all, if finance is so profitable, why not simply become one?

Because banking is profitable. Regulation is expensive.

Becoming a licensed deposit-taking bank requires heavy capital, compliance obligations, periodic regulatory reporting, prudential supervision, liquidity requirements, and a level of institutional patience that tech companies usually reserve for software updates.

Instead of becoming banks, platforms increasingly partner with NBFCs and established financial institutions.

This structure is elegant. The bank or NBFC carries the regulated balance sheet, compliance burden, and often ultimate credit exposure.

The platform handles the customer interface, behavioural data, underwriting signals, and distribution.

In simple terms: One side brings money. The other side brings intelligence.

Together, they scale faster.

That is why co-branded cards, embedded lending, merchant credit, checkout EMIs, and fintech partnerships exploded. A user may think they are borrowing from an app.

In reality, they are often borrowing through a bank, via a platform.

The platform owns the relationship. The lender owns the legal infrastructure.

This division became one of the defining architectures of modern digital finance.

Conclusion: When Convenience Learns to Underwrite You

The bigger story is not that apps are becoming banks. It is that finance is quietly blending into everyday life.

Earlier, financial decisions happened in clear and separate places. You went to a bank for a loan, bought insurance from an agent, and opened an investment account when you wanted to save. Finance was visible, formal, and often wrapped in paperwork thick enough to feel like a punishment for wanting your own money.

That wall is disappearing.

Today, finance shows up inside daily habits. Your food delivery app can offer credit. Your cab app can insure your ride. An online checkout page can quietly suggest EMI financing before you even finish buying headphones. Banking is no longer always a place; it is becoming a feature.

And that matters because convenience is never free.

Platforms are no longer just competing to sell products or complete transactions. They want something deeper: your financial relationship. A one-time purchase brings revenue. A wallet creates habit. Credit creates dependence. And data creates power.

That is the real shift. In the past, businesses valued factories, land, or scale. Then the internet valued attention. Now digital finance values predictability. Who spends before salary day? Who pays on time? Who responds to discounts? Who is safe to lend to? These small behaviours now act like a financial biography, built not by forms and branch managers, but by clicks, scans, repayments, and everyday digital habits.

This changes power in the economy. Traditional banks own capital. Platforms increasingly own behaviour. And in finance, behaviour can be more valuable than money itself, because better information reduces risk and reducing risk has always been one of the oldest ways to make money.

There is real upside here. Embedded finance can make credit easier, reduce friction, and include people who were once ignored by formal banks. A small merchant may get quick working capital without explaining his life story to a branch manager who still treats Excel like advanced artificial intelligence.

But there is a trade-off.

When a few apps control shopping, payments, lending, insurance, and savings, they stop being just service providers. They become financial gatekeepers.

So the real question is not whether your grocery app can offer you a loan. Of course it can. The real question is what we are giving up when we exchange financial visibility for convenience.

Every era has had its key asset. Land built feudal power. Factories built industrial power. Data built internet power. Increasingly, financial behaviour may become the next powerful asset.

Somewhere between scanning a QR code, ordering groceries, and clicking “Pay Later,” we may have entered a world where the most valuable thing we produce is not what we buy but what our behaviour quietly reveals.

Sources- PIB, Research & Market, Quashbugs, Business Standard, ET, Business World, Worldline, JM Financial Services, Enterslice & GlobalNewsWire.