Research #28 -Associated Alcohols & Breweries Ltd

Shows Good Potential...

Here at EquityEdge Research, we make Small-Cap Investing easy for you by Backing you up with Robust & Full-Fledged Research.

Read our Previous Summer Special Coverage Here:

Let’s go!

1. Company Charts

*Comparison charts are Indexed*

Associated Alcohols & Breweries Ltd Performance (1yr- up 125.70%)

Associated Alcohols & Breweries Ltd vs. NSE Nifty

Associated Alcohols & Breweries Ltd vs. NSE Smallcap

2. About Company

Associated Alcohols & Breweries Ltd (AABL) is a leading Indian liquor company based in Indore, Madhya Pradesh. Established in 1989, it operates in two key segments: potable alcohol and ethanol. The company manufactures a range of spirits including whisky, vodka, rum, gin, tequila, and brandy.

Company Journey

Domestic Market Presence

Business Model

Liquor Value Chain

AABAL’S Brand Portfolio

3. Management Overview

KMP's Remuneration

Product Business

AABAL’s Business Segment Financials

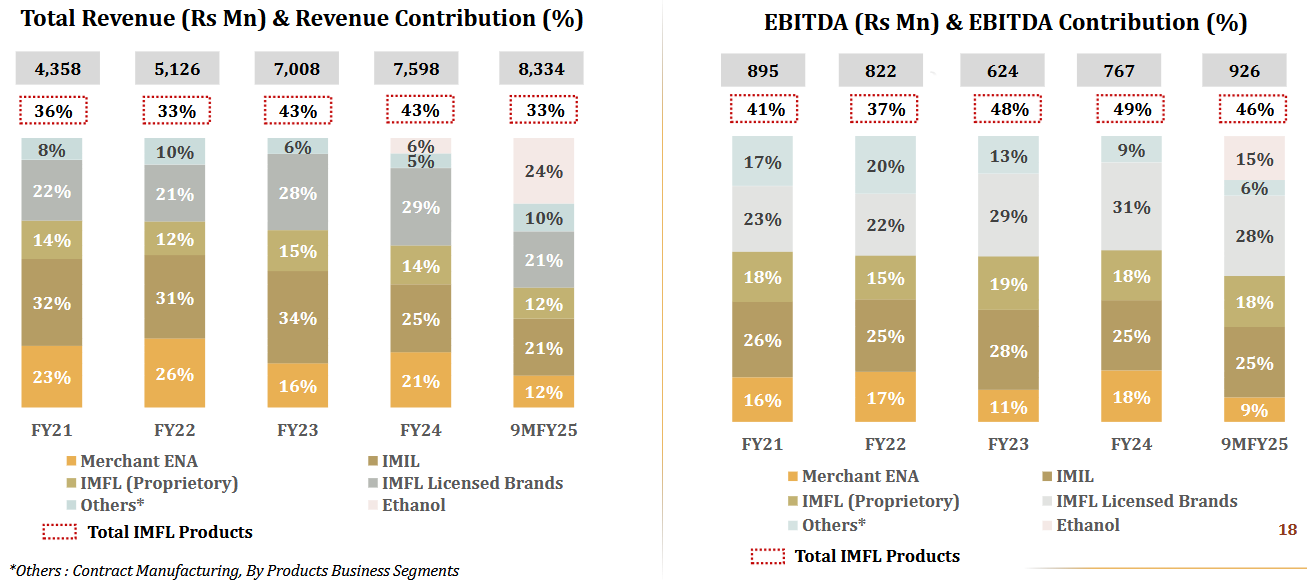

4. Segment-Wise Performance

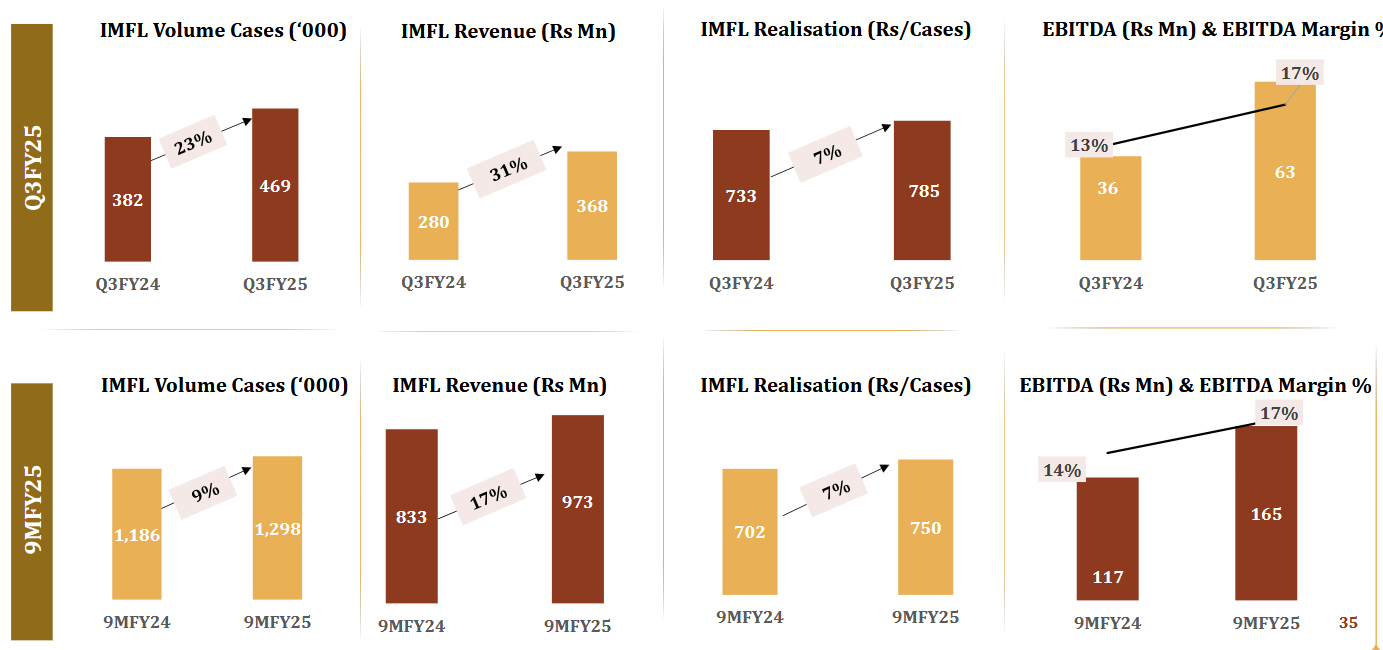

IMFL (PROPRIETARY)

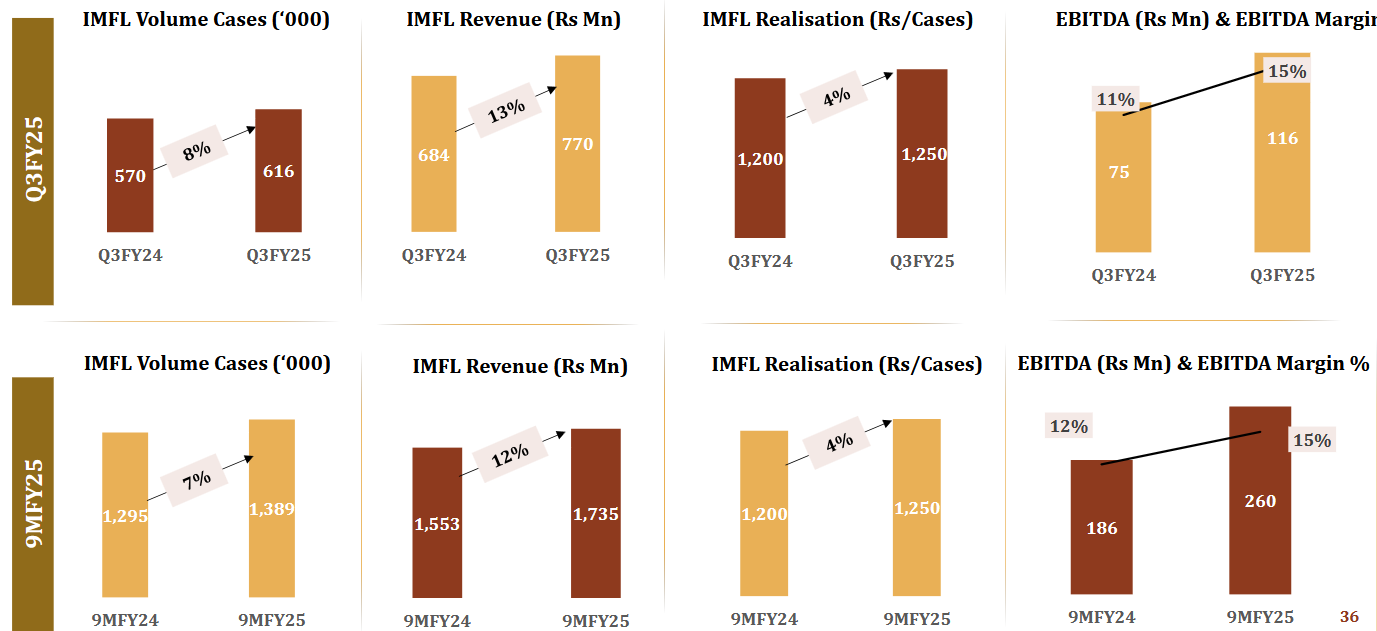

IMFL (LICENSED)

IMIL

MERCHANT ENA

ETHANOL

If you like the hard work we put in, you can invest in us:

For our Non-Indian audience: You can donate to us through PayPal. Click here.

For our Indian audience, UPI QRs are given below:

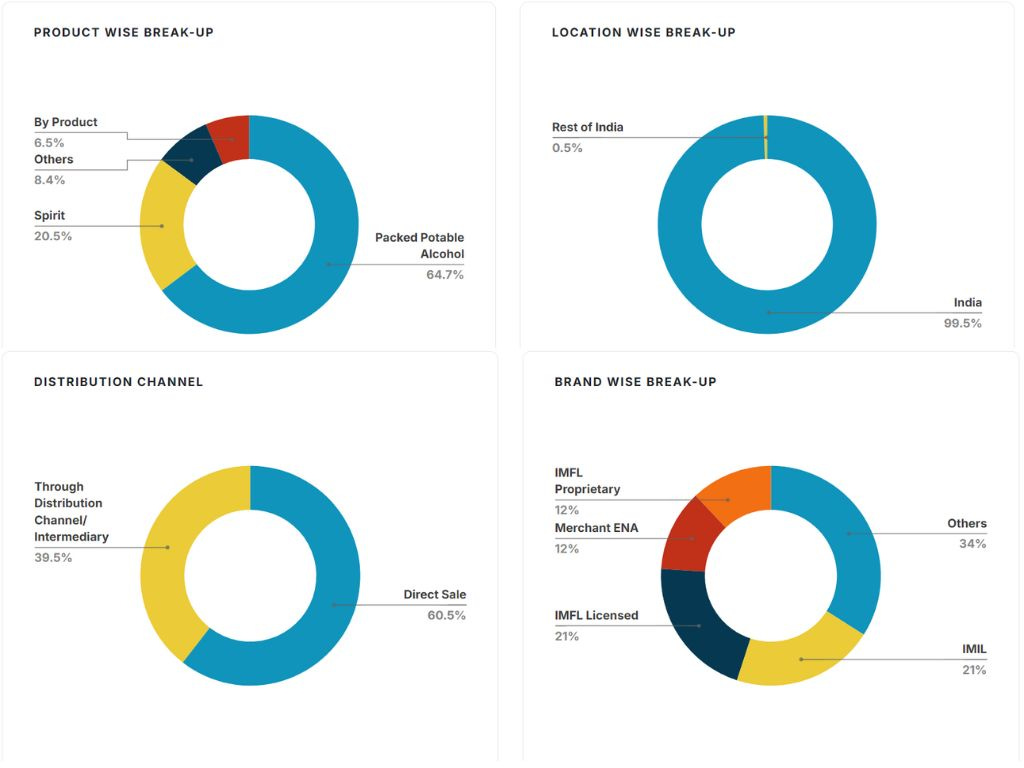

5. Revenue Breakdown:

6. Company’s Financial Analysis:

SALES:

Sales have grown at a CAGR of ~11% in the past 10 years. March 2021 Performance drop was due: to

COVID Lockdowns – Liquor shops, bars, and restaurants were shut or restricted, hitting retail and institutional sales.

Production Disruptions – Factory shutdowns and supply chain issues affected output and distribution.

Lower Demand – With weddings, parties, and travel on pause, alcohol consumption dropped.

State Policies – Some states raised taxes or added COVID cesses, impacting margins and volumes.

GROSS PROFIT:

Gross Profit has increased at a CAGR of ~13% for the past 10 years. The Margin improved during FY21, FY22 and FY23 due to fall in Material Costs and Other Mfr Expenses.

EBITDA:

EBITDA has increased at a CAGR of ~11% for the past 10 years. Even though the Revenue was down in FY21, EBITDA was up due to fall in Material costs and Other mfr Expenses. Recently, the EBITDA is down due to increase in costs again.

Net Profit Margin %

Net profits have continuously increased at a CAGR of ~17% for the past 10 years.

BALANCE SHEET:

Common-Size Balance Sheet:

Cashflow Statement:

Cash Conversion Cycle:

7. KEY RATIOS:

8. Shareholding Pattern:

9. SWOT ANALYSIS:

10. Concall Analysis Q3FY25:

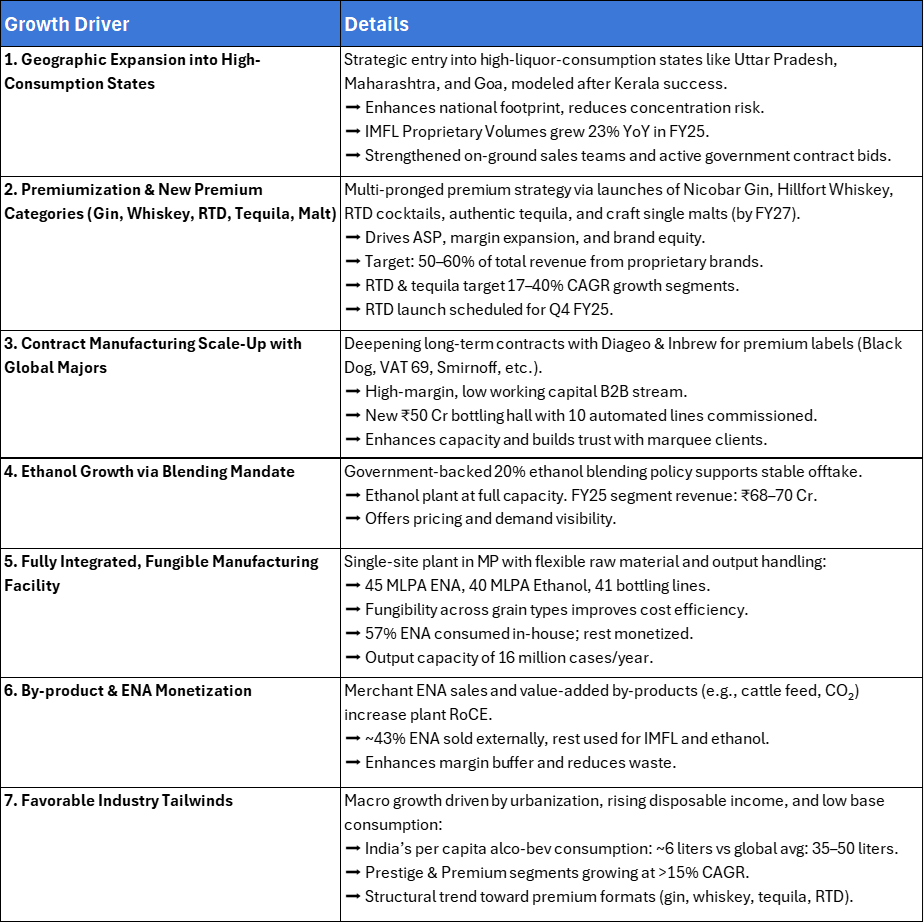

Opening Remarks: Strategic Positioning & Growth Story

CEO Anshuman Kedia set the tone by highlighting:

AABL’s resilience in a dynamic market, driven by festive and winter demand.

Strength in vertical integration across the liquor value chain – this gives them control over input costs and margins.

Three key strategic pillars: premiumization, operational excellence, and geographical expansion.

They’re leaning hard into premiumization, with a focus on RTDs, brandy, and tequila in Q4 FY25, tapping into the "quality over quantity" trend.

Product Strategy: Premiumization in Motion

CFO Tushar Bhandari dove into the execution side:

Premium products like Nicobar gin and Hillfort whiskey were launched recently, selling a modest 3,000 cases so far.

IMFL proprietary brand volumes grew 23% YoY, showing early traction.

Entry into UP, Maharashtra, and Goa is imminent – supply expected to begin within the month.

Ethanol Update:

Running at full capacity, with OMC allocation of 29,724 KL.

Ethanol revenue was INR 72 crore for the quarter, suggesting strong offtake and margins around 7–9%.

Regulatory Landscape: Madhya Pradesh Excise Policy

The proposed MP Excise Policy FY26 includes:

Closure of 47 shops – minimal impact (only 1.5% of MP retail).

Duty hike of 20% on shop license renewals – expected to be absorbed by retailers.

Digitalization and ethanol policies – welcomed by AABL.

Introduction of 60-proof country liquor and beer/wine-only bar licenses – aligns well with AABL’s RTD strategy.

Management is confident there’s no threat of a larger liquor ban, calling the changes progressive and pro-industry.

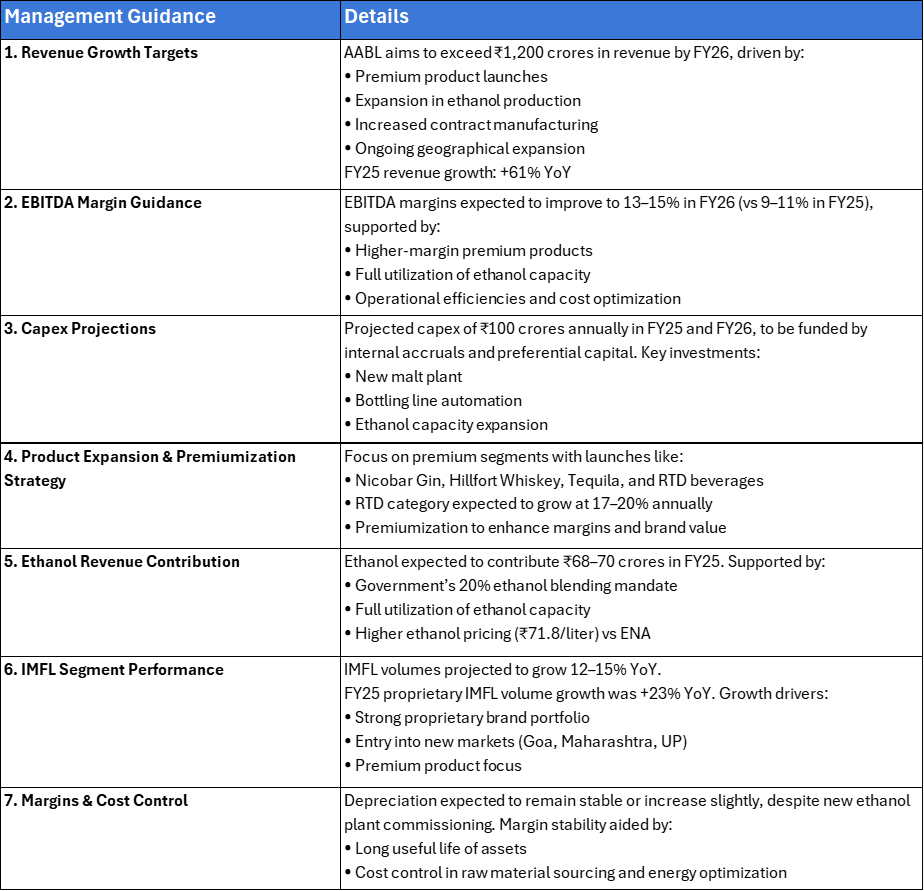

Margin Guidance: Why Still 9–11%?

A puzzling moment—despite premium products and ethanol kicking in, guidance was pegged at 9–11% EBITDA margin for FY25. The reasoning:

Premium products are too nascent to move the needle yet.

Full margin benefit expected to reflect from FY26, targeting 13–15%.

Capex and Expansion

Capex Guidance: ₹100 cr each in FY25 and FY26, funded via internal accruals and preferential issue.

Bottling expansion: 41 lines now, with 10 new ones recently added.

Single Malt Plant: Commissioning by April 2025, product expected by FY27 post aging.

Geographic Strategy

Now among top 5 in Kerala.

Entering UP, Maharashtra, Goa – states with massive liquor markets.

Long-term target: proprietary IMFL to contribute 50–60% of topline.

Other Key Highlights

RTD launch delayed due to imported machinery stuck in customs.

Marketing spend at 3–5% now, could rise to 6–7% as premium products scale.

Gin (Nicobar) and Whiskey (Hillfort) priced at ₹8,100 and ₹3,100 per case respectively.

Tequila launch to feature 100% agave, imported from Mexico. Minimal domestic competition currently.

Analyst Q&A – Key Takeaways

Margins will only improve significantly when premium products scale and ethanol RM cost stabilizes.

Ethanol revenues are expected to stay steady; plant is running at peak.

Raw material cost relief expected due to FCI rice at ₹22,500 and maize cultivation ramp-up.

AABL wants to build full portfolios in whiskey, vodka, rum, and RTDs—across all price segments.

CSD entry (defense canteens) in progress—seen as high-potential channel post-ban on imported brands.

11. Growth Drivers

12. Management Guidance

13. Competiors in the Market

1. Radico Khaitan Ltd

Strong Brand Portfolio: Owns popular brands like Magic Moments Vodka, 8PM Whisky, and Rampur Indian Single Malt.

Pan-India Distribution: Operates across all major states with a strong sales and distribution network.

2. United Spirits Ltd (Diageo India)

Market Leader: Largest spirits company in India by volume and revenue.

Global Backing: Backed by UK-based Diageo, giving access to global best practices and premium international brands like Johnnie Walker and Smirnoff.

3. Globus Spirits Ltd

Diversified Revenue Streams: Operates in IMFL, country liquor, and bulk alcohol.

Strong Focus on North India: Key markets include Haryana, Rajasthan, and Bihar.

4. Som Distilleries & Breweries Ltd

Product Mix: Engaged in both beer and IMFL; brands include Hunter Beer and Black Fort.

Export-Oriented: Also exports products to international markets including Africa and the Middle East.

5. Tilaknagar Industries Ltd

Brand Revival: Known for Mansion House Brandy, recently witnessing a turnaround in performance.

Focus on Brandy Segment: Among the top players in the Indian brandy market, especially in southern India.

14. Industry Overview

Introduction:

The Indian liquor industry is one of the largest and fastest-growing in the world, driven by rising incomes, urbanization, and changing social norms. It spans multiple segments, including Indian Made Foreign Liquor (IMFL), country liquor, beer, and premium spirits. Despite regulatory challenges and regional disparities, the sector is poised for significant growth, with increasing consumption across various demographic groups and rising demand for premium products. This overview provides insights into the market size, key trends, growth drivers, and regional dynamics shaping the future of the Indian liquor industry.

1. Market Size & Forecast (FY24–FY30):

The Indian alcoholic beverages market was valued at around ₹5.5 lakh crore (~$66 billion) in FY24.

It is expected to grow at a CAGR of 6–8%, reaching approximately ₹8.5 lakh crore (~$102 billion) by FY30.

India is the third-largest liquor market globally by volume, after China and the US.

2. Key Segments:

Indian Made Foreign Liquor (IMFL): Includes whisky, rum, vodka, gin, and brandy. Whisky dominates IMFL sales with over 60% share.

Country Liquor (CL): Low-cost alcohol with strong rural demand; accounts for ~35% of total consumption by volume.

Beer: Accounts for ~15% of industry value. Growing steadily, though from a lower base compared to spirits.

Wine & Premium Spirits: Small but fast-growing, driven by urban affluence and evolving tastes.

3. Key Trends:

Premiumisation: Consumers are trading up from regular to premium and super-premium spirits.

Rise of Craft and Boutique Brands: Growing demand for small-batch gin, whiskey, and flavored spirits among millennials.

Changing Social Norms: Increased alcohol consumption among urban women and youth, especially in metros.

Growth in RTD (Ready-to-Drink) and Mixology Culture: Especially in metros and tier-1 cities.

E-commerce and Digital Ordering: Emerging in some states (e.g., Maharashtra, West Bengal), especially post-COVID.

4. Growth Drivers:

Demographic Dividend: A large population of legal drinking age (~485 million as of 2024) with rising incomes.

Urbanization & Lifestyle Changes: Greater acceptance of alcohol consumption in urban centers.

Hospitality & Tourism Sector Expansion: Boosts consumption through restaurants, bars, and hotels.

Ethanol Blending Policy: Supports distillery capacities and financials, especially for dual-product companies (ethanol + liquor).

5. Regional Insights:

South India:

Highest per capita consumption.

Dominated by brandy in Tamil Nadu and Kerala.

North India:

High demand for whisky and country liquor in UP, Punjab, and Haryana.

West India:

Maharashtra and Goa are strong beer and premium liquor markets.

Dry States:

Liquor prohibition in Gujarat, Bihar, parts of Nagaland and Mizoram creates unorganized market issues and smuggling risks.

6. Recent Developments:

Policy Reforms: States like Delhi and Uttar Pradesh are experimenting with retail privatization and new excise regimes.

Investment in Capacity Expansion: Major players (e.g., Radico Khaitan, United Spirits) are expanding distilleries and launching premium lines.

Sustainability & ESG Focus: Use of biomass, wastewater recycling, and green distilleries gaining traction.

M&A & Brand Acquisitions: Focus on acquiring niche/craft brands to capture premium market share.

7. Challenges:

High Taxation: Liquor is one of the most heavily taxed industries in India; taxes account for up to 70% of retail price.

State-Level Licensing & Regulation: Fragmented and complex regulatory environment hinders national expansion.

Illicit Market & Counterfeits: Especially prevalent in country liquor and rural markets.