Q3 Update- Aditya Vision Ltd

YoY is UP!

1. Company Share Price chart & comparison with Index:

Aditya vision Performance

Aditya vision vs Nifty 50

Aditya vision vs Nifty Smallcap 50

2. About the Company

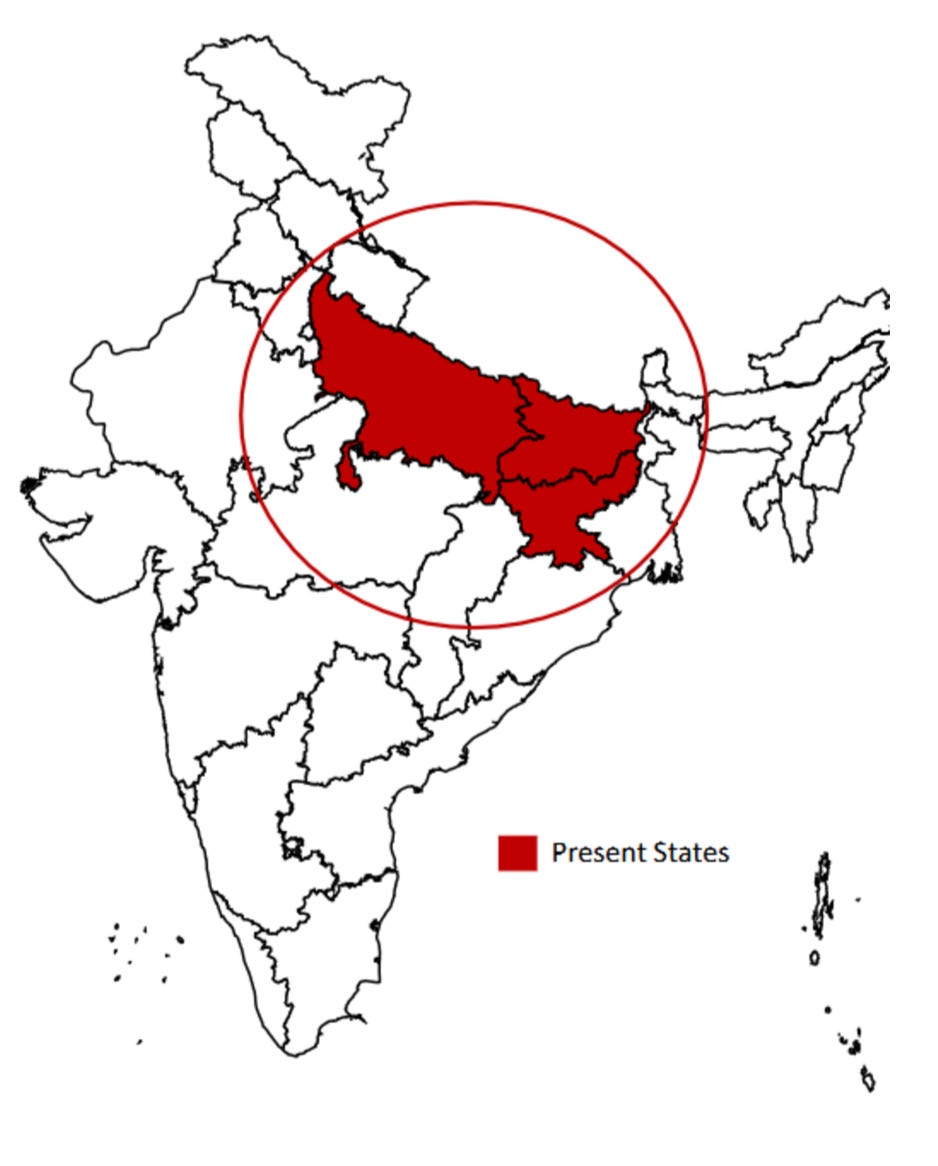

Aditya Vision Limited is a retail chain specializing in consumer electronics and home appliances, primarily operating in Bihar, Jharkhand, and Uttar Pradesh. It follows an omnichannel retail model, selling products through both offline stores and an online platform.

Business Model:

Multi-Brand Retail Stores – It operates exclusive multi-brand outlets offering products from major brands like Samsung, LG, Sony, and Whirlpool.

Regional Focus – It has a strong presence in Tier 2 and Tier 3 cities, catering to underserved markets.

Omnichannel Strategy – The company integrates online and offline sales channels for a seamless customer experience.

EMI & Financing Options – It collaborates with financial institutions to provide easy financing options, boosting affordability.

High Inventory Turnover – Due to its competitive pricing and demand-driven stocking strategy, the company maintains high inventory turnover.

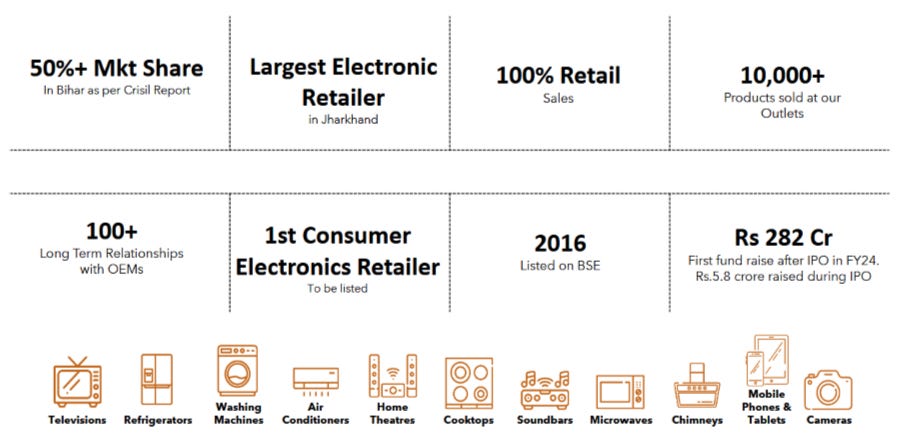

3. Aditya Vision Limited – Key Highlights

Products: Sells 10,000+ consumer electronics, including mobile phones, laptops, TVs, home appliances, and accessories.

Revenue Split (FY24): Home & entertainment – 66%, Digital gadgets – 21%, Others – 13%.

Retail Presence: 145 stores (as of FY24), now 148 (May 2024). The largest retailer in Bihar (105 stores) and Jharkhand (24 stores), expanding in Uttar Pradesh (19 stores). No store closures since inception.

Per Store Economics: ₹55-65 lakh capex, ₹2-2.25 crore working capital, 6-8 months breakeven, 3-year payback period, ₹2-2.25 lakh rent per store.

Market Share: ~50% in Bihar’s organized electronics retail, the largest in Jharkhand.

Business Model: 80% direct OEM supply, 20% via distributors/C&F agents.

Promoter Pledge: Reduced to 0% as of Q1FY24.

GST Raid: UP State GST search in April 2024.

Fund Raise: Raised ₹282 crore from Capital Group (FY24), first since IPO.

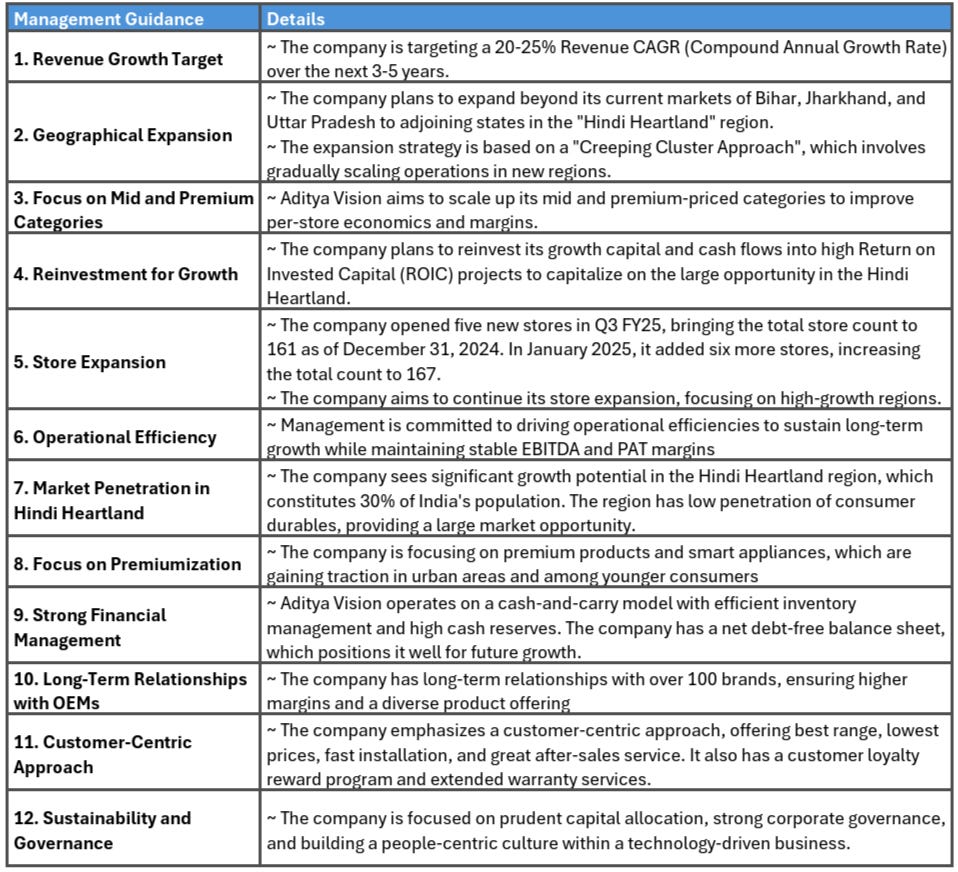

Growth Focus: Aiming for 20-25% revenue CAGR, expanding beyond Bihar, Jharkhand & UP into the Hindi heartland via a “Creeping Cluster Approach.”

(Source - Screener)

4. Aditya Vision at a Glance

Business Model

Presence

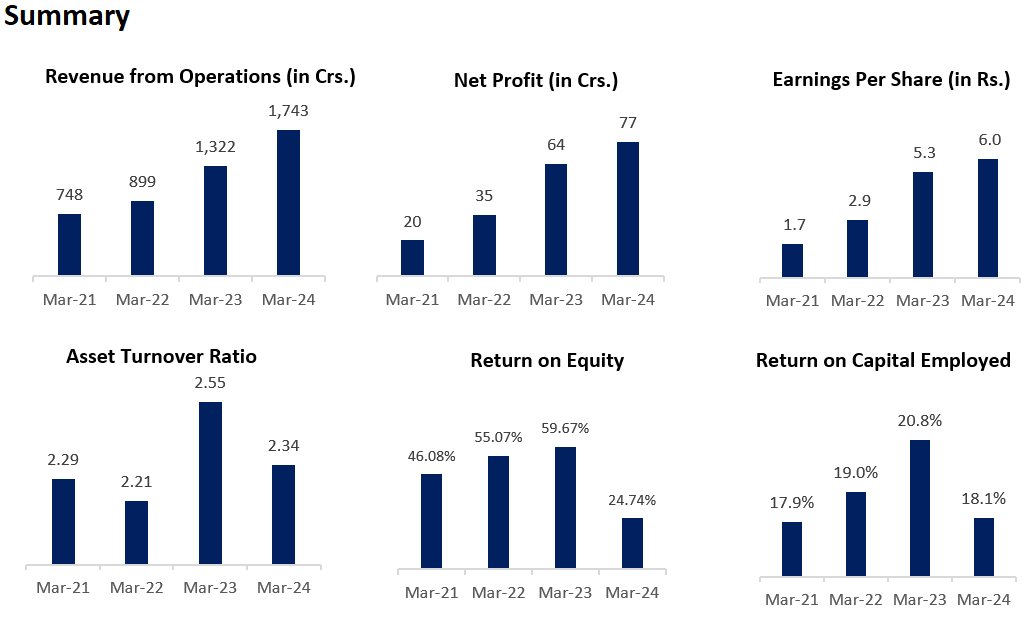

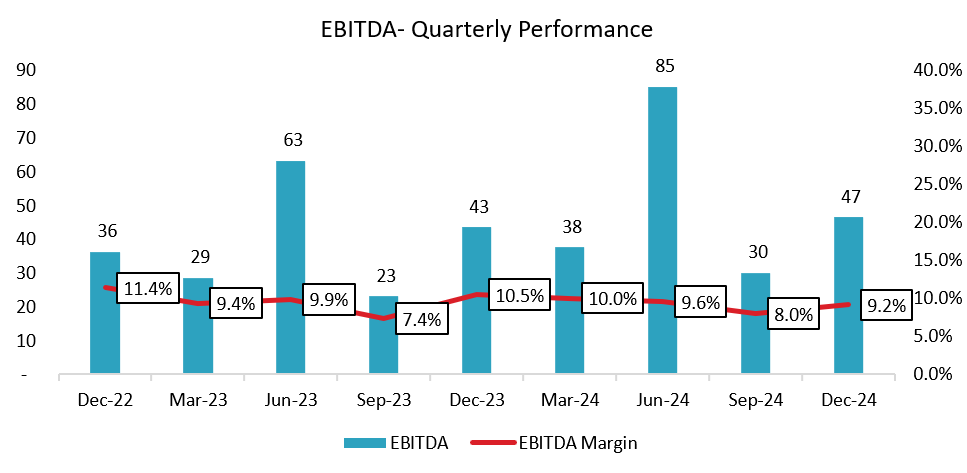

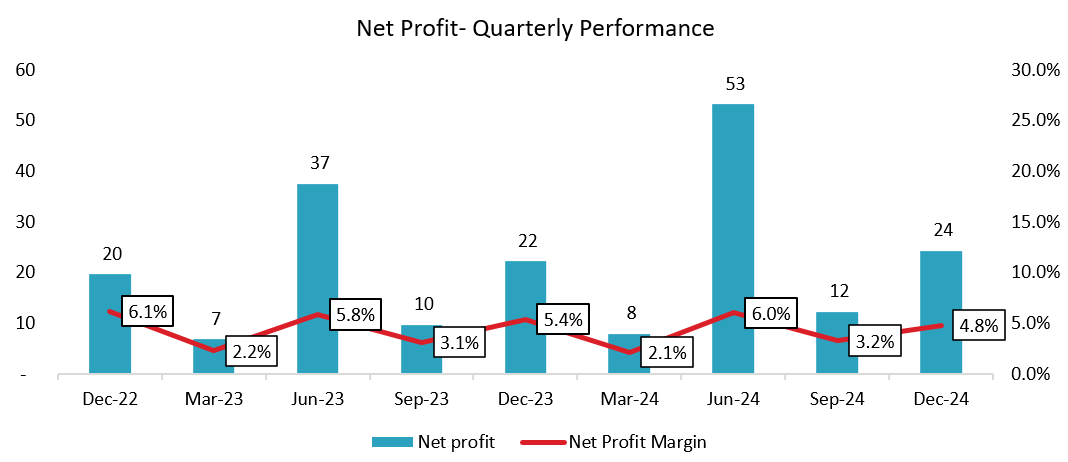

5. Financial Analysis:

Sales: grown at a compounded quarterly growth rate of 7.76% in the past 10 quarters.

EBITDA: grown at a compounded quarterly growth rate of 8.1% in the past 10 quarters.

Net Profit: grown at a compounded quarterly growth rate of 8.79% in the past 10 quarters.

6. Concall Analysis Q3FY25:

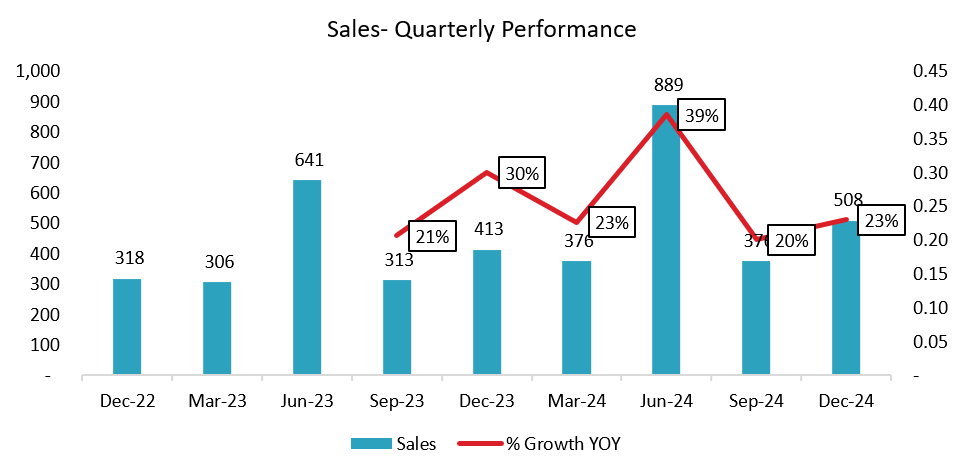

1. Financial Performance (Q3 FY25 vs Q3 FY24)

Revenue Growth: 23% YoY to ₹508 crore (from ₹413 crore).

9M FY25 Revenue: ₹1,773 crore, a 30% YoY growth (from ₹1,367 crore).

EBITDA Margin: 9.16% for Q3 and 9.12% for 9M FY25.

PAT: ₹24.22 crore, up 9.25% YoY (from ₹22.17 crore).

9M FY25 PAT: ₹89.51 crore, up 29% YoY (from ₹69.22 crore).

Gross Margins: 15.58% for Q3, slightly lower due to higher discounting post-festive season.

Same-Store Sales Growth (SSSG): 15% for 9M FY25, 13% for Q3 FY25.

2. Business & Expansion Updates

New Stores:

5 stores opened in Q3, bringing the count to 161 stores as of December 31, 2024.

Currently, 167 operational stores across Bihar, Jharkhand, and Uttar Pradesh.

Plan to add 8-10 more stores by FY25-end, surpassing earlier guidance.

Target: 200+ stores by FY26.

Geographic Expansion:

Strengthened presence in Eastern & Central UP (Lucknow, Varanasi, Gorakhpur, Prayagraj).

Increased revenue share from Jharkhand (13%) and UP (9%); Bihar remains the largest market (79%).

Festive Season Impact:

Strong sales in October, but sluggish demand in November-December led to lower gross margins.

Higher discounting affected profitability in Q3.

Inventory Strategy:

Inventory build-up for the summer season (ACs, refrigerators, cooling products) has already begun.

Early stocking ensures availability amid potential supply chain challenges.

3. Industry & Demand Trends

Macroeconomic Challenges:

High inflation & interest rates impacted demand, especially post-festive season.

Expecting demand revival from February to March 2025.

Product Mix & Competition:

Korean brands (Samsung, LG) maintaining market share.

Strong sales from Whirlpool, Godrej, Haier, IFB in ACs, refrigerators, and washing machines.

IT & mobility products contributed more due to lower demand for large appliances.

Seasonality & Growth Drivers:

Upcoming summer season expected to boost AC & cooling product sales.

Kumbh Mela & increased tourism in Ayodhya, Varanasi to boost demand in UP.

4. Future Outlook & Guidance

Revenue Growth: On track for 20-25% YoY growth in FY25.

EBITDA Margin: Expected to remain in the 8-10% range.

Store Expansion:

175 stores by FY25-end (definite target).

200+ stores by FY26.

Operating Leverage:

New stores maturing within 3 years, expected to improve profitability.

Focus on cost optimization & strategic store locations.

7. Growth Drivers

8. Management Guidance

Thank you for reading till the end! We hope you enjoyed this report.

Researched By- Naresh, Mayank and Vaibhav

All information is sourced from the company's annual reports, GoIndiastocks.in, Screener. in, industry reports and Economy Outlook reports.

Disclaimer- We do not recommend buying or selling any stock. You should consult your financial advisor before buying or selling any financial instrument.

If you like the hard work we put in, you can invest in us:

For our Non-Indian audience: You can donate to us through PayPal. Click here.

For our Indian audience, UPI QRs are given below: