PG Electroplast Ltd.

Here at EquityEdge Research, we make Small-Cap Investing easy for you by Backing you up with Robust & Full-Fledged Research.

Please Fill the form Below if you are interested in our Services and would like a Free Sample of our Equity Research Report covering a Small/Micro-cap Company.

Read our Previous Report here:

Let’s go!

1. Key Highlights:

1.1 Record-Breaking FY25 Performance:

Operating revenue surged 77% YoY to ₹4,869 crore.

Product business alone contributed ₹3,525 crore, up 111% YoY.

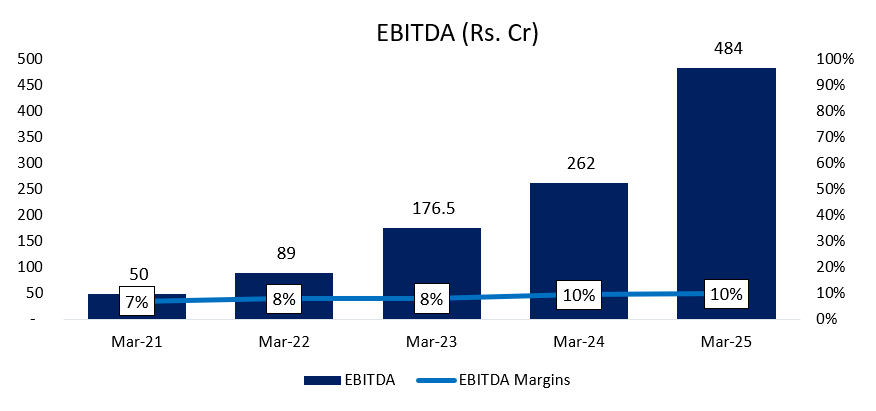

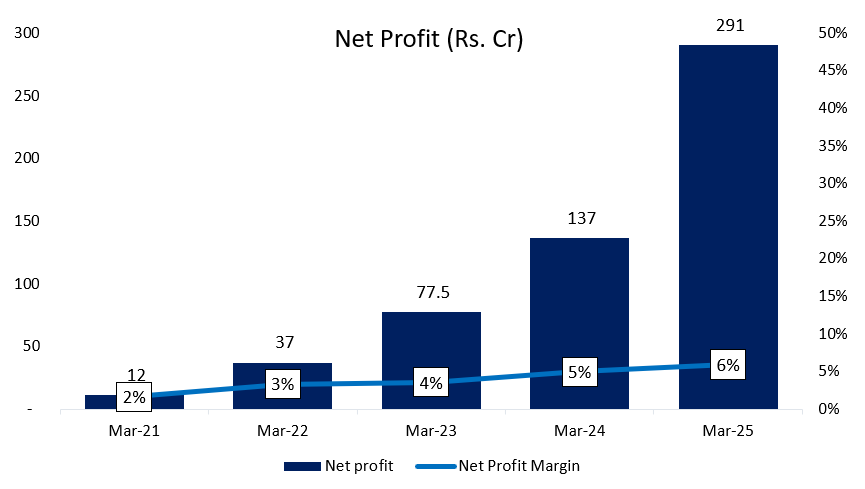

Net profit jumped 112% YoY to ₹291 crore, while EBITDA rose 81% to ₹519 crore.

Q4 FY25 revenue was ₹1,910 crore (+77%), with net profit at ₹146.4 crore (+105%).

1.2 Strong Growth in Key Segments:

Room AC business grew 128% YoY to ₹3,009 crore.

Washing machines rose 43%, and air coolers grew 80% YoY.

Despite a 5% drop in ASPs in some categories, volume growth drove the overall performance.

1.3 Aggressive FY26 Guidance:

FY26 group-level revenue guidance: ₹7,200 crore (+33% YoY).

Net profit guidance: ₹405 crore (+39%).

Product business expected to grow 35% to ₹4,770 crore.

CAPEX of ₹800–900 crore, including a refrigerator plant in South India and new Greenfield facilities for RAC and washing machines.

1.4 Solid Balance Sheet & Capital Efficiency:

Company is now net cash positive with ₹980 crore in cash.

FY25 CAPEX of ₹488 crore; net fixed asset turnover crossed 5x.

High working capital build-up due to compressor inventory (amid BIS concerns), but manageable and strategic.

1.5 Strategic Expansion & Future Initiatives:

Compressor manufacturing plant to be operational by Q4 FY26 – largely for in-house use, expected to be margin accretive.

New refrigerator business launch in FY27, with R&D and team already in place.

Continued investment in R&D with plans to expand into front-load washing machines.

Goodworth JV expected to become profitable in FY26 with a revenue target of ₹855 crore.

2. Company Chart Analysis:

*Comparison charts are Indexed*

PG Electroplast Ltd. Performance (1yr- up 199.13%)

PG Electroplast Ltd. vs. NSE Nifty

PG Electroplast Ltd. vs. NSE Smallcap

3. About the Company

PG Electroplast Ltd. (PGEL) is a leading Indian company in the Electronics Manufacturing Services (EMS) space. Established in 2003, the company operates as an ODM (Original Design Manufacturer) and OEM (Original Equipment Manufacturer) partner for various consumer durable and electronic brands. It offers integrated solutions including product design, tool making, plastic molding, PCB assembly, and final product assembly.

Business Segments

Product Assembly & ODM

Full-product manufacturing of items like washing machines, air conditioners, air coolers, and LED TVs.

Offers end-to-end design-to-delivery solutions for brands.

Plastic Injection Molding

Supplies precision-molded plastic components to a wide range of industries including electronics, automotive, and appliances.

One of the earliest services offered by the company.

Electronics Manufacturing (PCBA & Box Build)

Offers printed circuit board assembly and full electronics product assembly.

Supports products like set-top boxes, TVs, and medical devices.

Tool Manufacturing

In-house tooling division designs and manufactures molds and dies.

Supports rapid prototyping and mass production.

Business Verticals

Key Clients

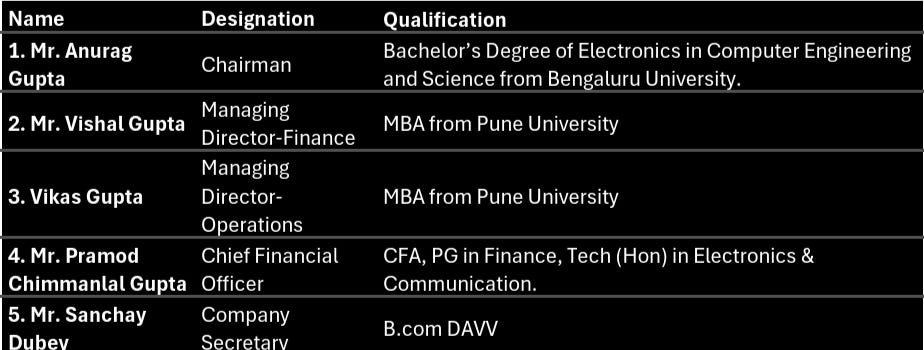

4. Management Overview

We are Proud to Announce Our New Launch of the Premium services where we Deep-dive into the Business and back you up with Robust Research.

We Provide services for different Level of Investors. You can Email us directly to start your journey!

5. Revenue Breakdown:

(Source: Screener.in)

1) Products (61% of revenue in FY24 vs. 44% in FY22)

PG Electroplast’s product business has seen rapid growth, driven by strong demand and capacity expansion. The segment includes:

Room Air Conditioners (RAC):

Offers indoor, outdoor, and window AC units.

2nd largest ODM player in India, serving over 30 leading brands.

Revenue grew 340%+ from FY22 to FY24, fueled by new launches and expanded capacity.

Washing Machines:

Provides semi-automatic (6-14 kg) and fully automatic (6.5-7.5 kg) models.

2nd largest ODM player in India, supporting 25+ brands.

Revenue grew 20% in FY24 and 56% in FY23, driven by new product ranges.

Air Coolers:

Offers window, desert, and personal coolers.

FY24 revenue was flat due to unseasonal rains.

2) Plastic Moulding (25% in FY24 vs. 49% in FY22)

Largest manufacturer of high-precision plastic components for consumer durables & electronics in India.

Revenue grew 27% from FY22 to FY24, supported by demand in sanitaryware and fan segments.

3) Electronics (13% in FY24 vs. 6% in FY22)

Provides PCB assembly and turnkey solutions for TV manufacturers.

Revenue surged 430%+ from FY22 to FY24, but the TV business (82% of segment revenue) was shifted to JV Goodworth Electronics in FY25, leading to an expected decline.

4) Tool Manufacturing (1%)

Supports specialty plastic moulding with custom tooling solutions.

Acts as an enabler for in-house production capabilities.

6. Company’s Financial Analysis:

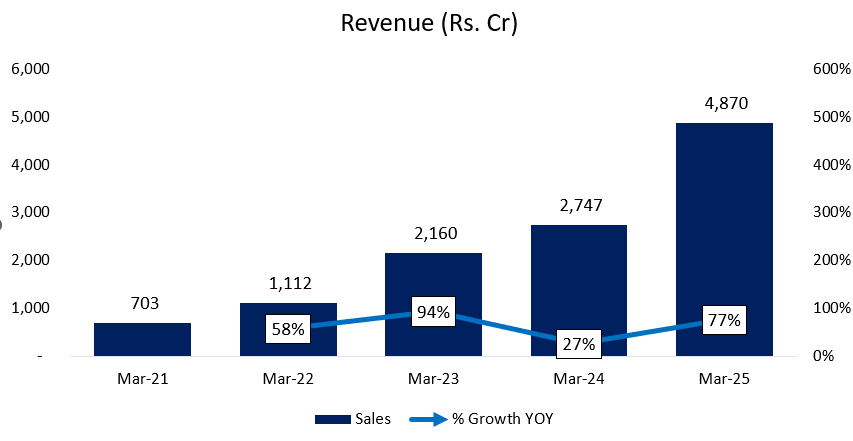

6.1 REVENUE:

Revenue has grown at a CAGR of ~62% in the past 5 years.

Why Growing so fast?

FY23: Revenue ~₹2,160 crore, up 94% YoY:

In FY23, PG Electroplast saw a breakout year driven by an aggressive scale-up in its product business. Revenue nearly doubled as the company capitalized on strong demand for room air conditioners, washing machines, and air coolers. The room AC segment stood out with a 180% jump in revenue, while washing machines grew 57% and air coolers surged by 169%. This was enabled by enhanced manufacturing capabilities and strong traction from both existing and new customers.

The company focused heavily on capturing cost leadership through efficient product design and began migrating portions of its component sourcing from overseas to domestic vendors. With new product introductions and broader customer acceptance, volumes soared. Margins improved too, supported by lower commodity prices and improved operating leverage, as more revenue was generated from the same fixed infrastructure. This set the tone for an aggressive growth path going forward.

FY24: Revenue ~₹2,746 crore, up 27% YoY:

FY24 marked a consolidation year where PG Electroplast grew despite macro headwinds like unseasonal rains and falling ASPs (average selling prices). Product business grew 24% even though ASPs for some categories dropped by up to 8%. Room AC revenue rose to ₹1,317 crore, up 26%, and washing machines delivered 20% growth, but air coolers remained flat due to price pressure. Despite these challenges, the company sustained volume growth across segments.

The year was also notable for capacity additions. A new greenfield plant at Bhiwadi came online, and a significant land acquisition (NGM) ensured infrastructure readiness for future expansion. The company also made a strategic shift by hiving off its low-margin TV business into a joint venture with the Jaina Group, forming Goodworth Electronics. This move reduced margin drag and positioned PGEL to focus on higher-value segments.

The company started receiving formal incentive payouts under the Production Linked Incentive (PLI) scheme, with ₹15 crore in PLI and about ₹4.7 crore in state incentives recognized as revenue. These incentives, along with better cost control and a leaner business structure, contributed to a 77% increase in net profit despite modest topline growth.

FY25: Revenue ~₹4,869 crore, up 77% YoY:

FY25 was a blockbuster year. The company reported 77% growth in revenue and a 112% increase in net profit. Product business was the primary engine, surging by 111% to ₹3,525 crore. The standout performer was the room AC segment, where revenue skyrocketed to ₹3,009 crore—a 128% jump—thanks to stronger market demand, better client coverage across 35+ brands, and full utilization of expanded capacities at Supa and Bhiwadi.

Washing machines also had a strong year with 43% growth, driven by increased penetration and early results from the Whirlpool partnership. Air coolers rebounded sharply, posting 80% growth after a flat year in FY24.

The company benefited from scale-driven efficiency and cash-rich operations. It ended the year with ₹980 crore in cash and turned net cash positive. Margins improved slightly due to commodity deflation and continued operating leverage. Incentive income continued to play a role, with ₹30 crore of PLI and ₹6 crore of state incentives booked in FY25. This added a cushion to profitability while supporting cash flow for future investments.

A major CAPEX cycle began, with ₹488 crore spent during FY25 and ₹800–900 crore planned for FY26. This includes a new refrigerator plant in South India, a compressor unit, and new greenfield projects for washing machines and RAC components. Management also guided for FY26 revenues of ₹7,200 crore and net profit of ₹405 crore, reinforcing their confidence in maintaining momentum.

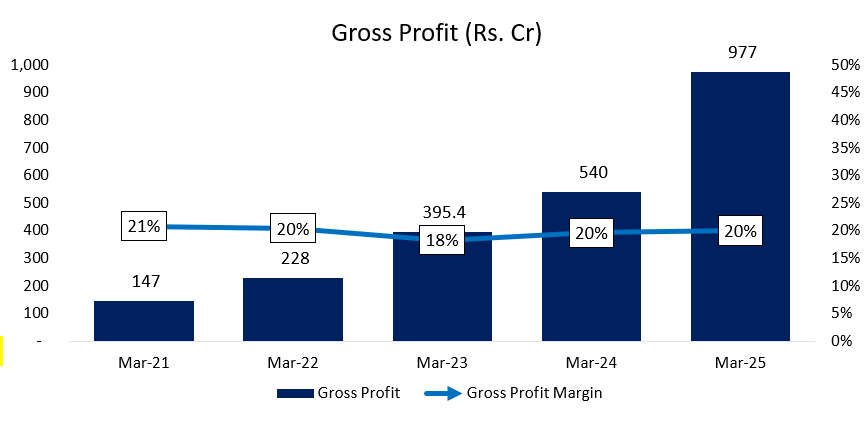

6.2 GROSS PROFIT:

Gross profit has increased at a CAGR of ~61% for the past 5 years. The Margins are stable.

6.3 EBITDA:

EBITDA has increased at a CAGR of ~77% for the past 5 years. The Margin has improved on accounts of a reduction in Other operating expenses (Employee costs was at 10% in FY21 vs 6% in FY25).

6.4 Net Profit:

Net profits have continuously increased at a CAGR of ~124% for the past 5 years. The increase in margin is due to decrease in Depreciation & Interest along with a fall in Tax rates by ~300bps since FY21.

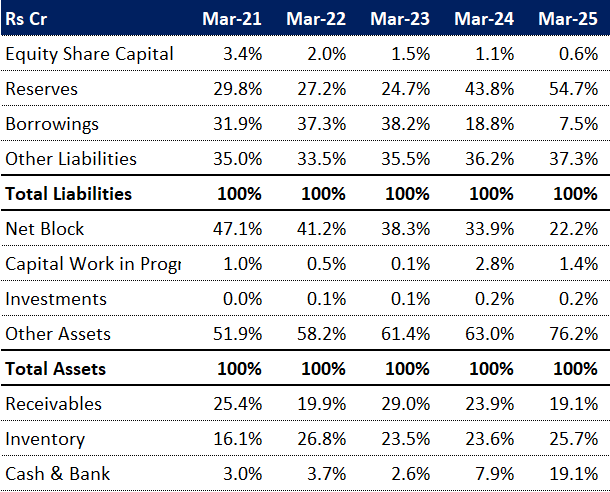

6.5 Balance Sheet:

6.6 Common-Size Balance Sheet:

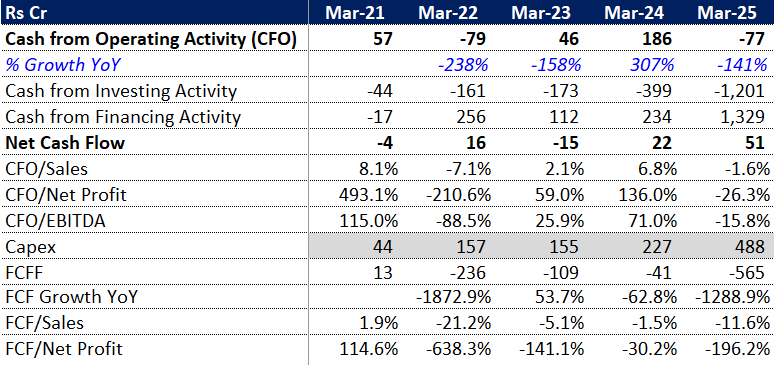

6.7 Cashflow Analysis:

In FY25:

CFO has gone negative due to WC adjustments (drastic increase in Receivables and Inventory).

CFI outflow increased massively due to Bank Deposit having maturity more than 3 months worth ~₹747 crs. and capex of ~₹488crs.

CFF has increased significantly. PG Electroplast Ltd. successfully raised ₹1,500 crore through a Qualified Institutional Placement (QIP) of equity shares.

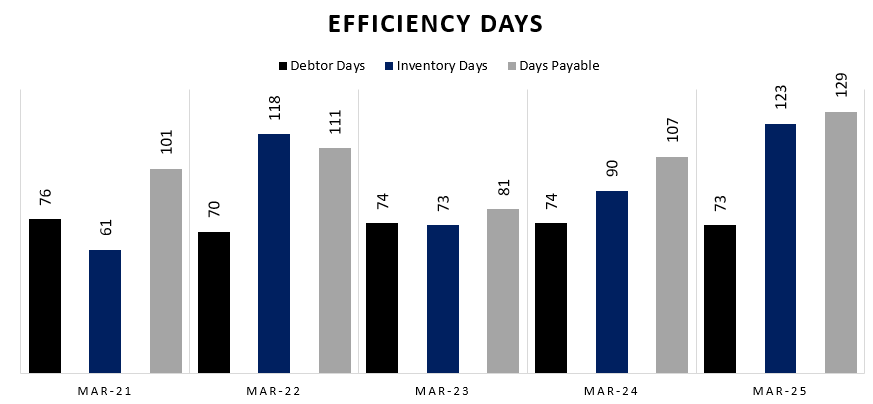

6.8 Cash Conversion Cycle:

7. KEY RATIOS:

8. Shareholding Pattern:

The sale is expected to enhance liquidity and broaden institutional ownership in the company.

On May 27, 2025, PG Electroplast's promoters—Vikas Gupta, Anurag Gupta, and Vishal Gupta—sold a combined 5.3% stake in the company, amounting to ₹1,132 crore, through open market transactions. They offloaded 1.5 crore shares at prices ranging from ₹754.83 to ₹755.73 per share. This sale reduced the promoters' collective holding from 49.37% to 44.07% .

The stake sale attracted significant institutional interest. The Government of Singapore acquired 38.18 lakh shares (1.35% stake) for ₹288 crore, while Motilal Oswal Asset Management Company purchased 15.89 lakh shares (0.56% stake) for ₹120 crore. Both entities bought shares at an average price of ₹754.80 each, totaling ₹408.22 crore in combined transactions.

Following these developments, PG Electroplast's stock price rose 3.5% to an intraday high of ₹792 on May 28, reflecting positive market sentiment towards the increased institutional participation and the company's strong financial performance.

9. Concall Analysis—Q4FY25:

📦 Business Strategy & Growth Drivers:

PGEL serves over 35 brands, which helps buffer against weak demand from any one client. While peers cited cautious demand due to erratic summer patterns, PGEL's diversified exposure kept momentum intact.

Capacity expansion is a key theme. The company is guiding ₹6,355 crore in standalone revenue for FY26, and ₹855 crore from Goodworth Electronics JV. Group revenue is projected at ₹7,200 crore, implying 33% YoY growth. Net profit is expected to rise to ₹405 crore (up 39%).

A CAPEX of ₹800–900 crore is planned for FY26. Projects include a new RAC plant in Bhiwadi, a washing machine plant in Greater Noida, a refrigerator facility in South India, and a compressor manufacturing line.

🧱 Capital Efficiency & Funding:

PGEL closed FY25 as a net cash company with ₹980 crore. It spent ₹488 crore on CAPEX during the year. Most future expansion will be funded through internal accruals. The fixed asset turnover has crossed 5x, and management is targeting 4–4.5x sustainably.

Over the next two years, the gross block is expected to nearly double from ₹1,200 crore to over ₹2,200 crore.

⚙️ Business Segments Outlook:

The product business remains the growth engine, with strong demand for RACs and washing machines. The new refrigerator segment will kick in from FY27.

The plastics division is expected to grow just 5–10% in FY26 due to lower raw material prices, which are passed through to clients.

Goodworth Electronics (JV) posted ₹544 crore in FY25 revenue with a small loss. FY26 revenue is guided at ₹855 crore, with 1.5–2% EBITDA margin expected.

Compressor manufacturing will begin in Q4 FY26, primarily for captive use. This should boost margins as compressors are currently imported (85–90% market share).

The EV assembly business is on hold pending regulatory clearances. Once approved, production can begin within 3–4 months.

🔬 R&D and Innovation:

While R&D spend is modest at 0.5–0.75% of turnover, management noted strong internal innovation. Products developed by PGEL have become industry benchmarks, with some even copied by clients. The R&D teams for ACs and washing machines have been scaled up significantly.

💰 Working Capital & Inventory:

Operating cash flow was negative ₹70–80 crore in FY25. This was due to a deliberate inventory build-up, especially compressors, in light of regulatory uncertainty. Inventory stood at ₹1,300 crore at year-end and is expected to normalize over FY26.

GST credits and capital advances also inflated the "Other Current Assets" line, but these will unwind over time.

📈 Management Outlook:

Management expects 30–35% annual growth for the next 2–3 years, driven by expanded capacity, increased outsourcing by brands, and scale benefits. Margins are expected to remain stable. Major Greenfield projects will start contributing meaningfully only from FY27.

Refrigerator production, compressors, and EVs will add to growth in the medium term. PGEL also sees opportunity in component PLI schemes and is actively exploring partnerships in China and Taiwan.

10. SWOT ANALYSIS:

11. Growth Drivers:

12. Competiors in the Market

Dixon Technologies (India) Ltd.

Source - The Economic Times The largest EMS player in India.

Manufactures LED TVs, mobile phones, washing machines, lighting products, and set-top boxes.

Strong ODM capabilities and a key supplier for global brands.

Amber Enterprises India Ltd.

Source - Dr Vijay Malik Specializes in manufacturing components and products for room air conditioners.

Also offers end-to-end solutions like PGEL.

Supplies to major AC brands like Voltas, Daikin, Hitachi, etc.

Kaynes Technology India Ltd.

Source - IPO watch A high-end EMS company with a focus on embedded systems, automotive electronics, and industrial automation.

Offers design-led manufacturing and IoT solutions.

Syrma SGS Technology Ltd.

Source - IPO Watch Offers electronics design and manufacturing, especially in RFID, power electronics, and PCBA.

Serves diverse sectors including automotive, healthcare, and industrial electronics.

Elin Electronics Ltd.

Source - IPO Watch Provides EMS for products like fans, lighting, kitchen appliances, and small home appliances.

Also engaged in manufacturing fractional horsepower motors and plastic molded parts.

Thank You So Much For Reading!!

Researched By- Naresh, Mayank and Vaibhav

All information is sourced from the company's annual reports, Press Release, News Articles, GoIndiastocks.in, Screener.in, industry reports and Economy Outlook reports.

Disclaimer: We do not recommend buying or selling any stock. You should consult your financial advisor before buying or selling any financial instrument.

We are Proud to Announce Our New Launch of the Premium services where we Deep-dive into the Business and back you up with Robust Research.

We Provide services for different Level of Investors. You can Email us directly to start your journey!

If you like the hard work we put in, you can invest in us:

For our Non-Indian audience: You can donate to us through PayPal. Click here.

For our Indian audience, UPI QRs are given below: