Here, at EquityEdge Research, we deep dive into complex Articles and Reports and make it easier for you by presenting everything, RIGHT HERE!!

Please Fill the form Below if you are interested in our Services and would like a Free Sample of our Equity Research Report covering a Small/Micro-cap Company.

Check out our Previous Industry Report:

What Will We Discuss Today?

What is IT?

Global IT Industry.

Indian IT Industry.

Import & Export Dynamics.

Industry Segmentation.

Key Trends/ Growth Drivers.

Risk and Challenges.

Major Players in India.

Conclusion.

1. WHAT IS IT?

Information Technology (IT) is the use of computers, software, and the internet to manage, store, and share information. It helps organizations work faster, smarter, and more securely by automating tasks, connecting people, and protecting data.

For example, when you use BHIM UPI to pay your vegetable vendor, the app securely connects your bank to theirs in seconds. This happens through a backend IT system managed by NPCI (National Payments Corporation of India). Similarly, when you check your CBSE exam results online, you're accessing a database stored and managed using IT infrastructure. Even platforms like IRCTC, Aadhaar, Paytm, and Swiggy rely on IT to handle millions of users, transactions, and real-time data every day.

Key components of IT:

Hardware – Physical devices like computers, servers, routers, and storage drives.

Software – Applications and operating systems that run on hardware.

Networking – Connecting systems through the internet or internal networks.

Databases – Organized storage systems to manage large amounts of information.

Cybersecurity – Protecting IT systems from data breaches and attacks.

IT Services – Support functions like helpdesks, system administration, cloud services, etc.

2. GLOBAL IT SERVICES INDUSTRY:

1. Market Size & Forecast

In 2024, the global IT services market was valued at approximately USD 1.28 trillion, up from USD 1.36 trillion in 2023.

Forecasts suggest the market will grow to between USD 1.50 and 1.61 trillion in 2025, and further to USD 2.59–2.98 trillion by 2030–34, reflecting a CAGR of 7–9%.

One research firm projects a market size of USD 2.57 trillion by 2033, at a CAGR of 8.1% from 2025–2033.

Another source estimates growth from USD 1.50 trillion in 2024 to USD 2.98 trillion by 2034, implying a CAGR of 7.11%.

2. Service Segment Composition

Consulting/professional services led the industry with a ~64% market share in 2024, equating to approximately USD 820 billion.

Managed services accounted for about 37%, and global managed service spending stood at approximately USD 289 billion in 2024, with a projected value of USD 650 billion by 2033, growing at CAGR of 9.4%.

Cloud services constituted the fastest-growing segment, capturing around 53–55% of IT services revenue, growing at a rate of ~16–16.4% and generating over USD 700 billion in 2024.

AI/ML services experienced rapid expansion with a growth rate of ~31.8%, reaching approximately USD 200–250 billion.

Cybersecurity services accounted for ~18% of total IT services spend, with a growth rate of ~13.7%.

3. Regional & Enterprise Segmentation

North America led the global market with a 38% share, representing ~USD 486 billion in 2024.

Europe followed with an estimated value of ~USD 358 billion, and Asia–Pacific contributed ~USD 333 billion.

Asia–Pacific is expected to witness the highest growth through 2033, with potential to reach USD 746 billion.

Large enterprises made up around 60–62% of total IT services spending, while SMEs grew faster at ~11.3%, particularly in managed and cloud-based services.

4. Key Growth Drivers & Trends

Rapid cloud migration, multi-cloud adoption, and hybrid infrastructure deployment became central to enterprise IT strategies.

Cybersecurity spending surged due to increased cyber threats and compliance requirements.

Widespread deployment of generative AI, automation platforms, and advanced analytics drove growth in consulting and managed services.

Pricing models transitioned toward outcome-based service contracts, replacing legacy time-and-material models.

5. Margin Trends & Cost Structures

Providers faced near-term margin pressure due to investments in AI talent, cloud capabilities, and automation infrastructure.

Operational cost management via offshoring, automation, and platform-based delivery helped maintain profitability.

Competitive intensity and client-side consolidation exerted downward pressure on pricing, especially in managed and cloud integration contracts.

3. INDIAN IT SERVICES INDUSTRY:

1. Industry Size and Growth

The Indian technology industry, as per NASSCOM's Strategic Review 2025, generated total revenues of approximately USD 282.6 billion in FY2025, reflecting a year-on-year growth of 5.1%. This includes IT services, BPM, engineering R&D, software products, and hardware.

The IT Services segment alone contributed around USD 137.1 billion, accounting for the largest share of the total industry. Growth in this segment was moderate at ~4.3%, largely due to cautious discretionary spending by global clients and project delays in key verticals like retail and technology.

Export revenues constituted a significant portion, standing at approximately USD 224 billion, while the domestic market contributed around USD 58.2 billion. The sector remains export-led, but demand from Indian enterprises is steadily growing, particularly in digital transformation and government-led infrastructure modernization.

Source- Statista

2. Employment and Talent Trends

The Indian IT sector employed around 5.8 million professionals in FY2025, with a net addition of over 126,000 jobs. While hiring remained subdued compared to earlier boom years, it remained stable due to demand for talent in next-gen technologies.

One of the most notable trends was a decline in attrition rates, which fell to ~12–13%, down significantly from the peak levels of over 22% observed in FY2022–23. This helped ease wage pressures and improve employee retention.

India continues to dominate the global talent pool in software services. The country now has more than 5 million software engineers, and according to NASSCOM and GitHub data, India is projected to surpass the United States in the number of active developers by 2027.

3. Operating Margins and Cost Dynamics

As per ICRA’s FY2025 outlook, the operating profit margins of large IT services companies remained robust at ~22–23%, despite rising costs in select areas. The margin resilience was driven by improved pyramid optimization, lower attrition-related costs, and increased offshoring.

The sector also saw a reduction in subcontracting and a move toward automation-based delivery, especially in infrastructure and application support services. Cost-saving initiatives such as hybrid workforce models and rationalized bench strength supported profitability.

4. Client Demand & Vertical Trends

Demand remained strong in BFSI, manufacturing, and energy/utilities, while technology, telecom, and media saw some weakness. Clients in North America and Europe, the two largest geographies, were cautious in committing to long-term discretionary projects, reflecting macroeconomic uncertainties.

The Global Capability Centre (GCC) model gained considerable traction. India is now home to over 1,700 GCCs, representing more than 50% of all GCCs globally, positioning it as a critical hub for global enterprise operations, R&D, and platform delivery.

5. Technology Drivers

The industry continues to be reshaped by major shifts in technology focus. The largest growth vectors in FY2025 were:

Cloud transformation: Continued investments in cloud-native applications and hybrid cloud infrastructure, especially among Fortune 1000 clients.

Cybersecurity services: Rising demand due to increased regulatory scrutiny and remote workforce vulnerabilities.

AI and GenAI adoption: Most top IT service providers initiated large-scale deployment of AI solutions for clients, with internal productivity enhancements using Generative AI copilots.

Data engineering and analytics: Enterprises are scaling data platforms for real-time intelligence, fueling demand for high-end analytics and AI/ML skillsets.

6. Mid-Tier Players and Competitive Landscape

According to NASSCOM's segmentation data, the revenue share of the top five IT services exporters declined slightly, reflecting the rise of mid-tier players. Companies such as Persistent Systems, Coforge, and LTIMindtree grew faster than the large players in specific verticals like healthcare, BFSI, and engineering services.

This signals a broadening of the delivery ecosystem, with emerging players increasingly taking on complex transformation deals, especially in North America and Europe.

7. Outlook for FY2026

NASSCOM and ICRA expect the Indian IT services industry to cross USD 300 billion in total revenues in FY2026. IT Services is forecast to grow at 4–6% in USD terms, supported by improved global demand conditions, increased technology budgets, and scaling of GenAI deployments.

However, headwinds persist due to macroeconomic uncertainty in developed markets, continued pressure on discretionary IT spending, and the potential for pricing pressure in commoditized services.

4. EXPORT PERFORMANCE (FY2023-24)

Total Software Services Exports

Including foreign affiliates: USD 205.2 billion.

Excluding overseas commercial presence: USD 190.7 billion (up 2.8% YoY).

Key Export Destinations

1. United States remains India's largest export market, accounting for 54.70% of software exports at $109.40 billion. Other major destinations include:

United Kingdom: $28.70 billion (14.35%).

Singapore: $7 billion (3.50%).

China: $5.50 billion (2.75%).

2. Breakdown by Destination (Software Services)

United States- 54%

Europe- 31% (UK major within Europe)

Other15%

3. Mode & Delivery

Cross-border supply: 83.5% of software services exports.

Off-site services: 90% of total software exports (up from 80% ten years ago).

Overseas commercial presence: Declined to 7.0% from 7.5% in FY23.

4. Domestic vs. Export Revenue (IT Services)

Domestic IT services revenue: USD 54.4 billion (up 5.9% YoY).

Export-only IT services revenue: USD 199 billion (up 3.3% YoY in constant currency).

Sources- ET, BUSINESS STANDARD, DECCAN HERALD.

5. INDUSTRY SEGMENTATION:

1. IT Services

Focuses on providing technology support and solutions to other businesses.

Examples: TCS, Infosys, Wipro, HCLTech.

Services: Software development, consulting, system integration, infrastructure management.

Customers: Banks, governments, telecoms, healthcare, retail.

2. Business Process Management (BPM) / BPO

Handles back-office tasks and customer support on behalf of other companies.

Examples: Genpact, WNS, Concentrix, TCS-BPO.

Services: Call centers, finance & accounting, HR services, insurance claims processing.

Common clients: Global banks, airlines, ecommerce companies.

3. IT Products / Software Products

Creates and sells ready-made software tools or platforms.

Examples: Zoho, Freshworks, Tally Solutions.

Products: CRM, accounting software, HR tools, enterprise platforms.

Customers: SMEs, large corporations, government.

4. Hardware & Networking

Provides the physical backbone of IT—devices and connectivity.

Examples: HCL Infosystems, Dell India, HP, Cisco.

Products/Services: Servers, routers, laptops, data centers, network support.

5. Cloud Computing & Data Centers

Offers on-demand computing, storage, and application services over the internet.

Examples: Amazon Web Services (AWS India), Microsoft Azure, NTT India, CtrlS.

Services: Cloud hosting, SaaS, IaaS, backup, disaster recovery.

6. Cybersecurity

Protects digital systems and data from threats and attacks.

Examples: Quick Heal, TAC Security, Lucideus.

Services: Antivirus, firewall, data protection, penetration testing.

7. Artificial Intelligence (AI) & Machine Learning (ML)

Focus: Data analysis, automation, predictions, natural language processing.

Examples in India: Tata Elxsi (AI for automotive), Fractal Analytics, Arya.ai.

Use Cases: Chatbots, fraud detection, predictive healthcare, recommendation engines.

8. Blockchain

Focus: Decentralized and tamper-proof data storage and transactions.

Examples in India: Tech Mahindra (Blockchain for telecom contracts), Signzy (digital banking KYC), Polygon (Web3 infrastructure).

Use Cases: Supply chain tracking, digital identity, smart contracts, crypto.

9. Internet of Things (IoT)

Focus: Connecting physical devices to the internet for real-time data exchange.

Examples in India: Bosch India, Tata Communications, Stellapps (agritech IoT).

Use Cases: Smart homes, industrial automation, smart agriculture, fleet tracking.

10. Augmented Reality (AR) & Virtual Reality (VR)

Focus: Enhancing or simulating real-world experiences using digital interfaces.

Examples in India: Imaginate (enterprise AR/VR), Scapic (acquired by Flipkart).

Use Cases: Virtual training, immersive retail experiences, remote maintenance.

11. Robotics & Process Automation (RPA)

Focus: Automating repetitive tasks using software robots or physical robots.

Examples in India: UiPath India, Automation Anywhere, Addverb Technologies.

Use Cases: Invoice processing, assembly lines, logistics, HR onboarding.

12. Quantum Computing (nascent in India)

Focus: High-performance computing using quantum mechanics.

Examples in India: TCS, IISc, QNu Labs (quantum encryption).

Use Cases: Drug discovery, cryptography, weather modeling (early stage).

6. KEY TRENDS/ GROWTH DRIVERS:

1. The Silent Rise of GovTech in Tier-3 India

India’s small-town and rural governance is quietly undergoing a digital overhaul. From platforms like DIGIT (Digital Infrastructure for Governance, Impact & Transformation) used for smart municipal functions, to eOffice udeployments across state secretariats, small IT vendors are bagging contracts to digitize everything from land records to local water billing systems.

These are not flashy startups or unicorns—but slow, stable, and revenue-assured projects funded by government schemes and World Bank programs. GovTech is evolving into a long-tail IT segment most people aren’t watching.

2. Legacy Tech Is the New Goldmine

While the buzz is all about cloud and GenAI, much of India’s IT export revenue still depends on legacy systems—think COBOL (Common Business-Oriented Language) for insurance, mainframes for core banking, and Oracle DB (Database) for enterprise apps.

As younger developers avoid these “outdated” skills, mid-career techies who’ve stuck with legacy tech are finding themselves in high demand—especially from global BFSI (Banking, Financial Services, and Insurance) clients. Indian firms are now running global compliance updates and critical migrations that no one wants but everyone needs.

3. Spiritual-Tech: Digitizing Faith at Scale

Temples, ashrams, and spiritual trusts are modernizing. India’s religious institutions are investing in e-donation portals, virtual darshan (viewing of deities) livestreams, CRM (Customer Relationship Management) tools for devotee management, and AI-based crowd control analytics at events like the Kumbh Mela.

Organizations like ISKCON and Tirumala Tirupati Devasthanams are onboarding tech teams, while niche startups are offering ERP (Enterprise Resource Planning) tools customized for spiritual institutions. It’s a low-profile but high-volume sector with loyal users and massive seasonal traffic.

4. Africa and Gulf Are the Quiet Growth Engines

While the US and Europe dominate headlines, Indian IT exporters—especially mid-sized firms—are rapidly gaining ground in Africa, the Gulf, and Southeast Asia. Countries like Kenya, Oman, Nigeria, and Vietnam are digitizing public healthcare, education, and tax systems—and looking to Indian IT firms for cost-effective solutions.

These contracts are small individually but stack up over time. IT consultancies based in Pune, Noida, and Ahmedabad are even opening local delivery centers in Nairobi and Muscat. This "silent south-south" trade could be the next ₹1,000 crore play.

5. Domain Experts, Not Engineers, Are Building the Next Micro-SaaS Wave

A quiet revolution is underway where non-tech professionals—bankers, doctors, HR managers—are launching software products using no-code or low-code platforms like Bubble, Glide, and Zoho Creator. Their edge is deep domain insight and clarity on user pain points.

These founders are building micro-SaaS (Software-as-a-Service) tools for GST filing, hospital queue management, attendance compliance, or small-school CRMs. Many are bootstrapped, profitable, and growing in niche verticals where VC-funded giants aren’t looking.

7. RISKS & CHALLENGES:

1. Rising Digital Protectionism in Global Markets

Indian IT firms are increasingly facing data localisation mandates and digital protectionism in countries like Germany, Australia, and Saudi Arabia. Clients now demand that data be stored and processed locally, which eats into India's cost advantage.

With stricter DPDP (Digital Personal Data Protection)-style regulations globally, Indian exporters may need to set up in-country cloud zones, hire local staff, and navigate unfamiliar compliance regimes—shrinking margins and delaying delivery timelines.

2. Mid-Level Workforce Redundancy Crisis

India’s IT sector has a massive layer of mid-level project managers and tech leads (8–15 years of experience) whose roles are increasingly threatened by automation, agile delivery models, and GenAI-based coding assistants.

Unlike entry-level coders who can reskill fast, these professionals are stuck with outdated tools or bloated managerial layers. This “sandwich layer” is under-utilized but overpaid, creating internal cost-pressure and silent layoffs, especially in Tier-1 firms.

3. SME Clients Are Defaulting on Digital Transformation Projects

A growing number of small and mid-sized Indian enterprises (SMEs) are jumping onto IT projects—ERP (Enterprise Resource Planning), CRM (Customer Relationship Management), custom apps—but midway, many run out of budget, shift priorities, or ghost vendors.

For small IT firms, this leads to high receivables, project delays, and legal hassles. The Indian SaaS and IT consulting market faces a trust gap when dealing with non-enterprise clients, especially in Tier-2/3 cities.

4. Vendor Fatigue in Government Tech Projects

While GovTech is booming, many IT vendors complain of delayed payments, tender opacity, unrealistic SLAs (Service-Level Agreements), and bureaucratic inefficiencies. Even when contracts are awarded, fund disbursal often takes 6–12 months, leading to working capital strain.

Projects under Smart Cities Mission, state eGovernance initiatives, and municipal platforms often get paused mid-way due to elections or policy reversals—making government work a risky bet for smaller IT players.

5. AI-Created IP (Intellectual Property) Is a Legal Grey Zone

With widespread adoption of AI code assistants (like GitHub Copilot) and content generation tools, IT firms now face uncertainty around IP ownership, copyright liabilities, and auditability. If an AI writes code, who owns it? If it reuses open-source content, is it plagiarized?

Indian clients, especially in BFSI and pharma, are starting to demand manual audit trails for AI-written components, increasing delivery costs and legal exposure. The legal framework in India hasn’t caught up yet, leaving firms in a compliance vacuum.

Source:

DPDP Act, 2023 – India

OECD Report on Digital Trade Barriers

NASSCOM – Workforce of the Future

LiveMint – Mid-career IT job squeeze

Economic Times – Govt vendor payment delays

Business Standard – SME SaaS failure rates

The Hindu – IP & AI Legal Uncertainty

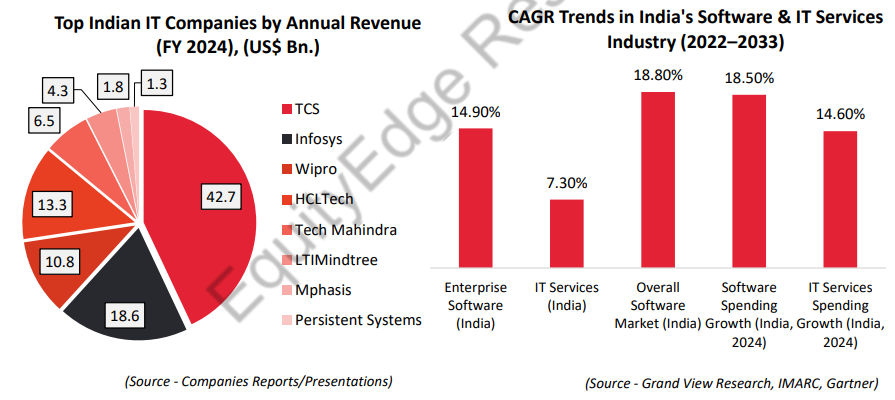

8. Major Players in India:

1. Tata Consultancy Services (TCS):

Tata Consultancy Services, a part of the Tata Group, is the largest IT services company in India by revenue and market cap. Established in 1968, TCS provides a wide range of services including IT consulting, software development, infrastructure support, business process outsourcing (BPO), and enterprise solutions. The company serves clients across industries such as BFSI, retail, healthcare, manufacturing, and telecommunications. With its strong focus on digital transformation, AI, and cloud services, TCS operates in over 46 countries and is known for its robust delivery model and large-scale workforce.

2. Infosys:

Founded in 1981, Infosys is a global leader in next-generation digital services and consulting. The company offers services in areas such as application development, cloud computing, digital transformation, AI, data analytics, and enterprise software implementation. Infosys caters to clients in banking, insurance, retail, energy, and healthcare sectors. With innovation hubs in the U.S., Europe, and India, the company has invested heavily in upskilling, sustainability, and automation platforms such as Infosys Cobalt and Infosys Topaz, to drive efficiency and deliver business value to clients globally.

3. Wipro:

Wipro is one of India's oldest and most diversified IT companies, originally started as a consumer goods company before pivoting to technology services in the 1980s. It now provides end-to-end IT services, consulting, and business process solutions. Wipro operates across segments such as cybersecurity, cloud services, digital engineering, and enterprise application services. With a presence in over 60 countries, Wipro serves industries including BFSI, energy, retail, and healthcare. The company is also focusing on sustainability and innovation through its Wipro Holmes AI platform and Designit for digital strategy.

4. HCLTech:

HCL Technologies, now branded as HCLTech, is a global IT services company that focuses on engineering and R&D services, cloud computing, cybersecurity, and digital transformation. It started as a hardware company in 1976 and evolved into a major player in software and services. HCLTech has a strong presence in North America and Europe and serves sectors such as banking, automotive, life sciences, and telecom. Its notable platforms include DRYiCE for automation and AI-driven service delivery, and the company is recognized for its deep partnerships with hyperscalers like Microsoft and Google Cloud.

5. Tech Mahindra:

Part of the Mahindra Group, Tech Mahindra is known for its strong focus on telecom, engineering services, and digital transformation. The company provides IT solutions across various industries, with a major emphasis on 5G, cloud infrastructure, blockchain, and artificial intelligence. It serves clients in sectors like telecommunications, manufacturing, BFSI, and healthcare. With its acquisition of companies like Comviva and LCC, Tech Mahindra has reinforced its telecom and network engineering capabilities and is driving innovation through its Makers Lab R&D centers.

6. LTIMindtree:

LTIMindtree is a merged entity formed in 2022 between Larsen & Toubro Infotech and Mindtree, both previously separate IT companies under the L&T Group. The combined firm offers a strong portfolio of digital transformation, cloud, data, and engineering services. LTIMindtree caters to clients in BFSI, manufacturing, CPG, and media, and is known for blending scale with agility. The company focuses on digital-native solutions and domain expertise to deliver high-impact business outcomes and has been expanding its global delivery centers to support large-scale IT modernization projects.

7. Persistent Systems:

Persistent Systems is a mid-sized IT services firm headquartered in Pune, known for its strong focus on software product engineering and digital transformation services. The company works extensively with ISVs (Independent Software Vendors), healthcare providers, and BFSI clients. It offers services in data management, cloud, AI/ML, and DevOps, and has partnered with leading tech companies like Microsoft, Salesforce, and AWS. Persistent is well-regarded for its product mindset and capabilities in building scalable digital platforms.

8. Mphasis:

Mphasis is an IT services and solutions provider focused on cloud and cognitive services. Originally part of Hewlett-Packard, Mphasis now operates independently and specializes in serving the banking, financial services, and insurance (BFSI) sectors. The company has developed proprietary platforms like NextLabs and NextAngles for digital and risk analytics. Mphasis has a strong delivery model known as Front2Back™ Transformation, which uses customer-centric approaches to redesign core business processes using cloud, AI, and automation.

9. Coforge (formerly NIIT Technologies):

Coforge is a mid-tier IT services company with a strong vertical focus on BFSI, travel & transportation, and healthcare. Known for its deep domain expertise, Coforge offers services in cloud, digital integration, analytics, and low-code/no-code solutions. The company has expanded globally, with key delivery centers in India, the U.S., and Europe. It has also invested in developing its own IPs and platforms for insurance, asset management, and airline operations.

10. Birlasoft:

Part of the CK Birla Group, Birlasoft specializes in enterprise application services, especially around ERP and digital transformation using platforms like SAP, Oracle, and Salesforce. The company caters to manufacturing, life sciences, BFSI, and utilities sectors. It has a growing presence in data analytics, cloud migration, and product lifecycle management, combining domain knowledge with emerging technologies to streamline complex business processes.

9. CONCLUSION:

The Indian IT industry stands at a quiet but crucial crossroads. For decades, it thrived on cost arbitrage, large workforces, and predictable client contracts, especially from the West. But the ground is shifting. With generative AI automating code, testing, and even support, the traditional delivery models that built this sector are now under threat. Most large firms are still focused on headcount growth and incremental service deals, while innovation and deep-tech R&D remain limited to a few outliers.

Yes, there are new revenue streams in government tech, legacy maintenance, and emerging markets but these are survival plays, not scalable growth stories. The global tech narrative is moving toward productization, automation, and IP-led platforms. Indian IT hasn’t yet carved out a clear moat in this future, be it AI infrastructure, enterprise SaaS, or vertical-specific platforms.

The industry can either evolve into a high-skill, innovation-led ecosystem or risk being reduced to a low-margin execution shop in an AI-first world. The choice isn’t five years away, it’s already here...

So, the question isn’t whether Indian IT is doing well today.

The real question is what’s going to keep it relevant tomorrow?

THANK YOU FOR READING!!

Hope you liked our work. Please Subscribe so that we can reach out to more People like you!

We are Proud to Announce Our New Launch of the Premium services where we Deep-dive into the Business and back you up with Robust Research.

We Provide services for different Level of Investors. You can Email us directly to start your journey!