Here, at EquityEdge Research, we deep dive into complex Articles and Reports and make it easier for you by presenting everything, RIGHT HERE!!

Please Fill the form Below if you are interested in our Services and would like a Free Sample of our Equity Research Report covering a Small/Micro-cap Company.

Check out our Previous Industry Report:

What do you mean by the Electronic Component Industry?

Global Electronic Component Industry.

Indian Electronic Component Industry.

Industry Segmentation.

Key Trends/Growth Drivers:

Industry Risk and Future Challenges.

Major Players in India.

Conclusion.

1. What do you mean by the Electronic Component Industry?

The electronic component industry refers to the sector involved in the design, manufacturing, and supply of fundamental parts used in electronic devices and systems. Electronic components are the basic building blocks that enable electronic circuits to function by controlling, transmitting, or storing electrical signals and energy. These components include active components such as semiconductors, integrated circuits, transistors, and diodes, as well as passive components like resistors, capacitors, inductors, and connectors. The industry supports a wide range of end-use sectors including consumer electronics, telecommunications, automotive electronics, industrial automation, aerospace, and healthcare equipment. The value chain typically involves raw material sourcing, semiconductor fabrication, component assembly, testing, and distribution to device manufacturers. Growth in the electronic component industry is closely linked to rising demand for smartphones, computers, electric vehicles, IoT devices, and advanced communication technologies, making it a critical backbone of the global electronics and technology ecosystem.

Sources: Statista; Grand View Research; Fortune Business Insights; Mordor Intelligence; IMARC Group.

2. Global Electronic Component Industry:

2.1 Market Size and Growth

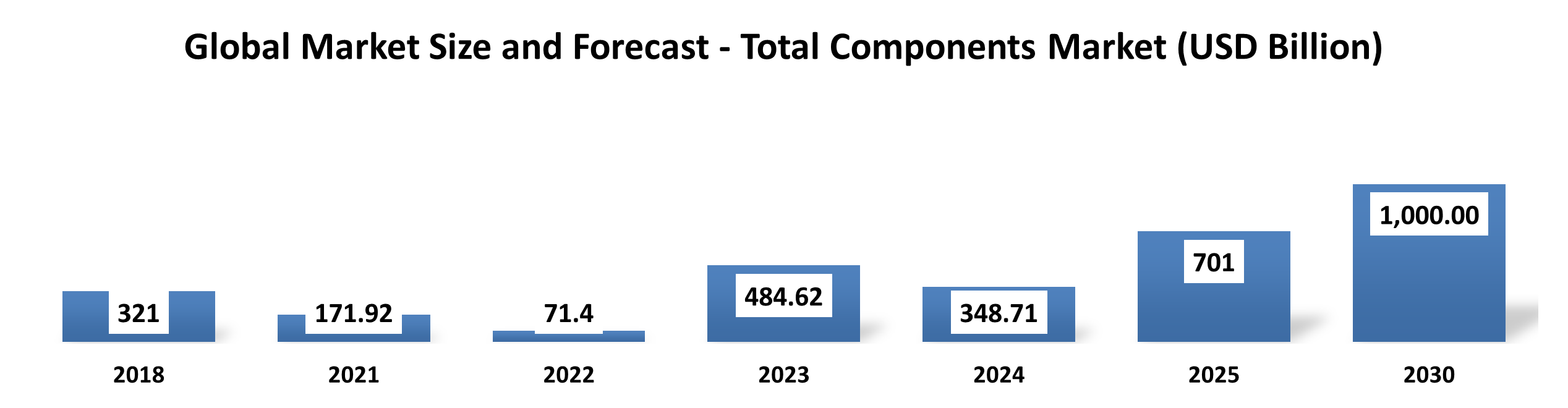

The global electronic components market is experiencing a period of significant structural expansion, with its valuation reaching approximately USD 701 billion in 2025. This sector is projected to cross the USD 1 trillion milestone by 2030, representing a compound annual growth rate (CAGR) of 7.36% during the forecast period.

Broader estimates encompassing the entire electronic component services and manufacturing landscape suggest even higher momentum, with valuations expected to reach USD 1,003.44 billion by 2034, driven by a 10% CAGR.

This growth reflects the industry’s recovery from post-pandemic volatility and its essential role in the ongoing digital transformation of global infrastructure.

2.2 Key Segments

The industry is functionally categorized into active, passive, and electromechanical components, with active devices, such as integrated circuits, transistors, and diodes, commanding a dominant 93.1% share of total market revenue as of 2024.

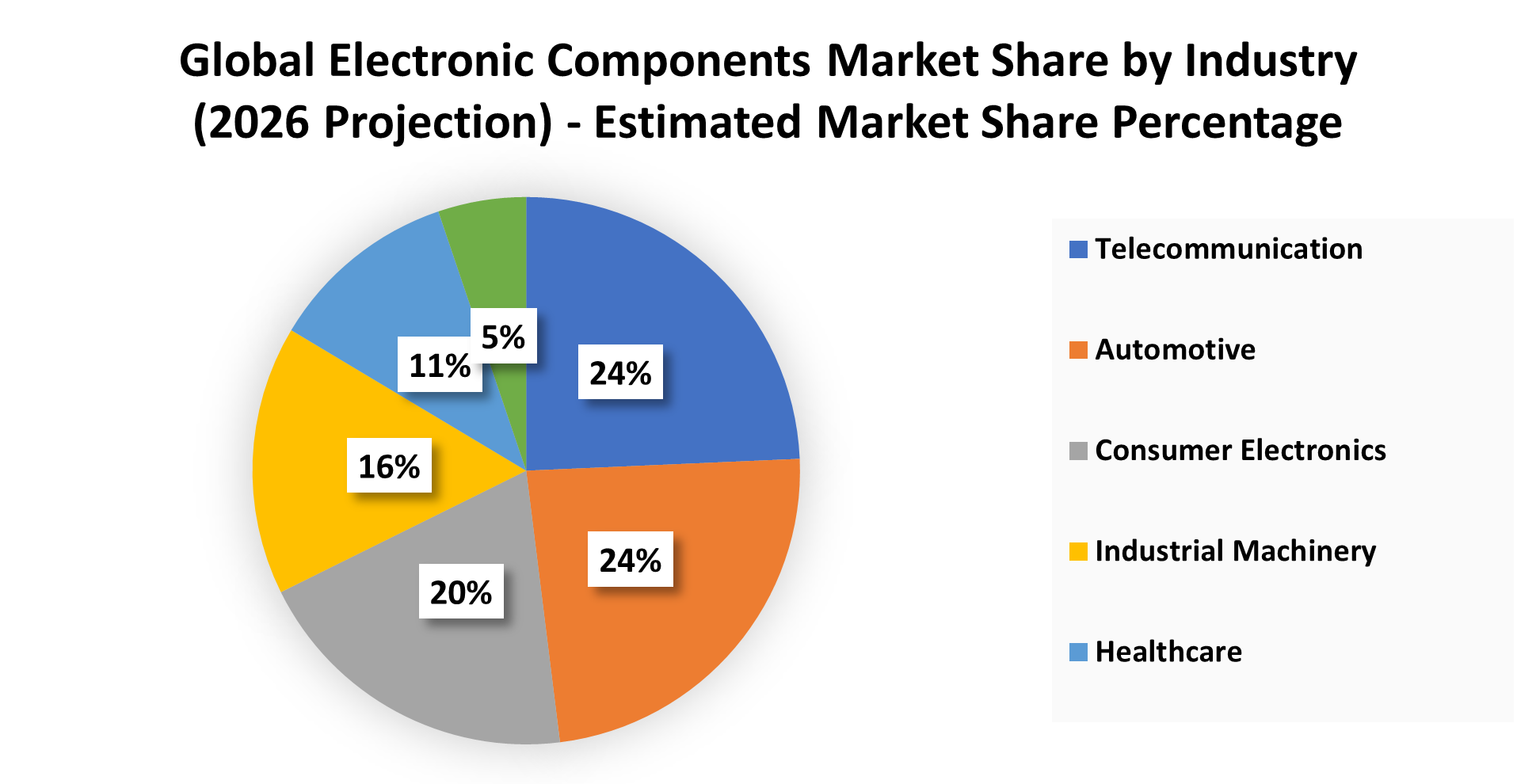

From an end-user perspective, the market is becoming increasingly diversified across high-growth verticals. According to 2026 projections, Telecommunications and Automotive are the primary value drivers, accounting for approximately 24.31% and 23.72% of the market share, respectively.

Consumer Electronics remains a massive pillar of the industry, representing nearly 19.65% of the market, while Industrial Machinery and Healthcare continue to expand their digital footprints, contributing approximately 15.90% and 11.22% to the global share.

2.3 Regional Highlights

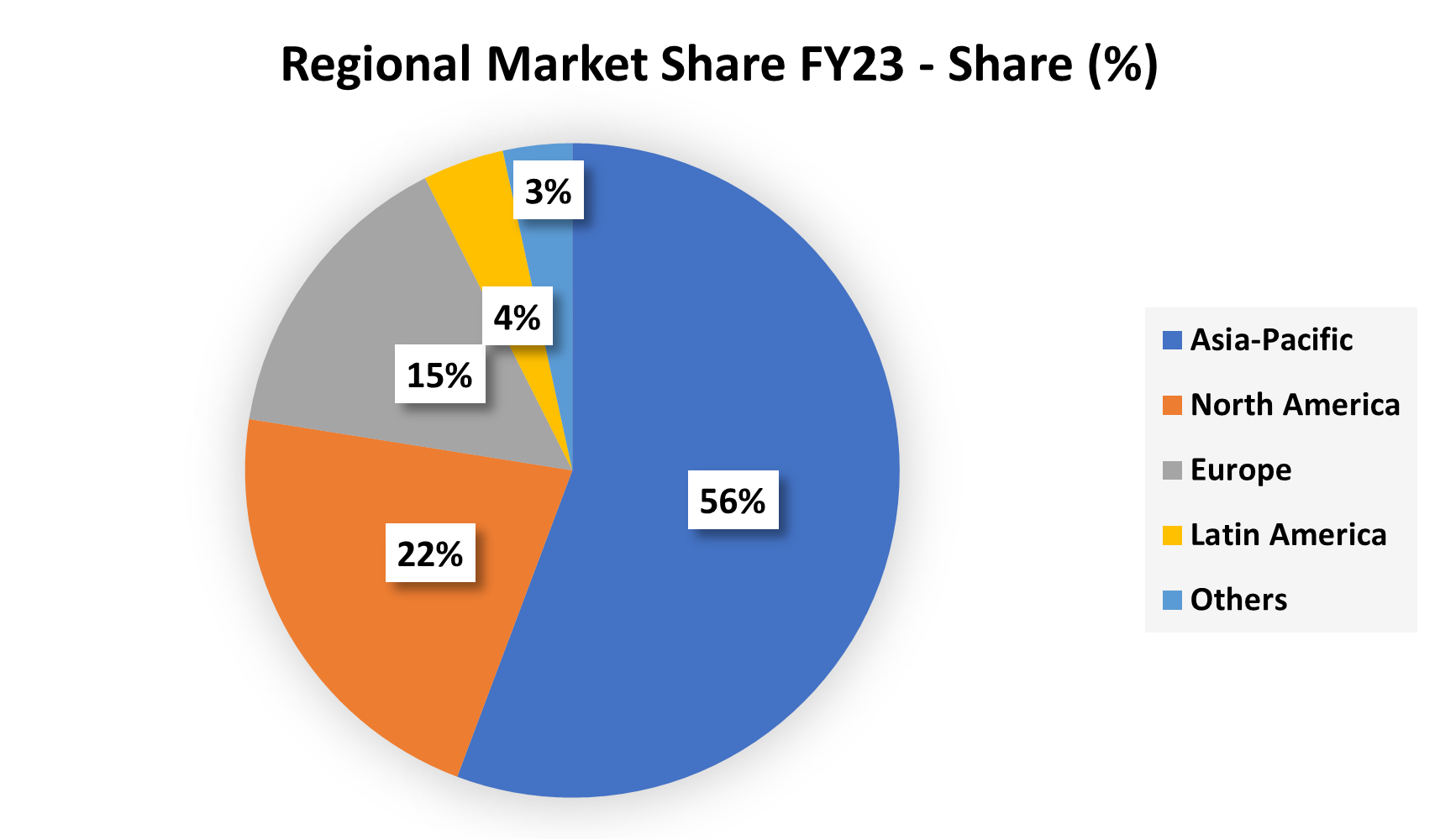

Asia-Pacific remains the undisputed global hub for electronics manufacturing, accounting for 47.5% of total sales in 2024 and maintaining its position as the largest market through 2030.

China, Taiwan, and South Korea lead the region, with China alone producing an estimated USD 874 billion in electronics output as of 2022. North America is identified as the fastest-growing regional market for specific component categories, benefiting from advanced technological infrastructure and high demand for AI-centric logic chips.

Europe maintains a strong manufacturing focus on automotive and industrial electronics, with Germany serving as the largest domestic market in the region.

2.4 Technology Drivers

The primary catalysts for growth in the mid-2020s are the proliferation of generative artificial intelligence and the rollout of 5G infrastructure. AI semiconductors including specialized processors and high-bandwidth memory (HBM), accounted for nearly one-third of total semiconductor sales in 2025 and are expected to represent over 50% of total chip sales by 2029.

The densification of 5G networks is driving record demand for high-frequency RF front-end modules and advanced power ICs. Furthermore, the rapid electrification of the automotive sector is significantly increasing the semiconductor dollar content per vehicle to support Advanced Driver Assistance Systems (ADAS) and EV powertrains.

2.5 Key Challenges

The industry faces persistent structural challenges, most notably the high concentration of advanced node production in limited geographic regions, which creates systemic supply chain vulnerabilities.

Prolonged shortages of critical materials, such as silicon wafers and specialized substrates like ABF, have periodically restricted output for active devices. Rising power densities in next-generation AI chips have introduced complex thermal management hurdles that exceed current packaging capabilities, potentially acting as a drag on performance growth.

Additionally, manufacturers must navigate the volatility of rare-earth pricing and the ongoing risk of counterfeit components undermining original equipment manufacturer (OEM) confidence.

2.6 Major Industry Participants

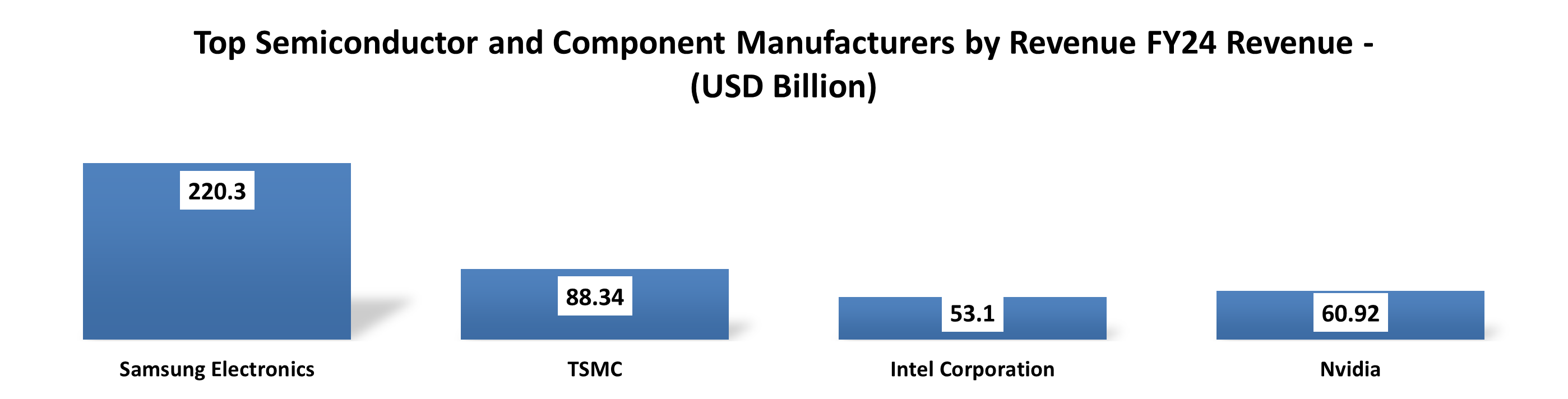

The competitive landscape is defined by massive capital expenditure among global leaders, with NVIDIA becoming the first vendor to surpass USD 100 billion in annual semiconductor sales in 2025.

Samsung Electronics and SK Hynix remain the dominant forces in the memory market, while TSMC maintains an undisputed lead in the foundry sector with a global market share of 64.9%.

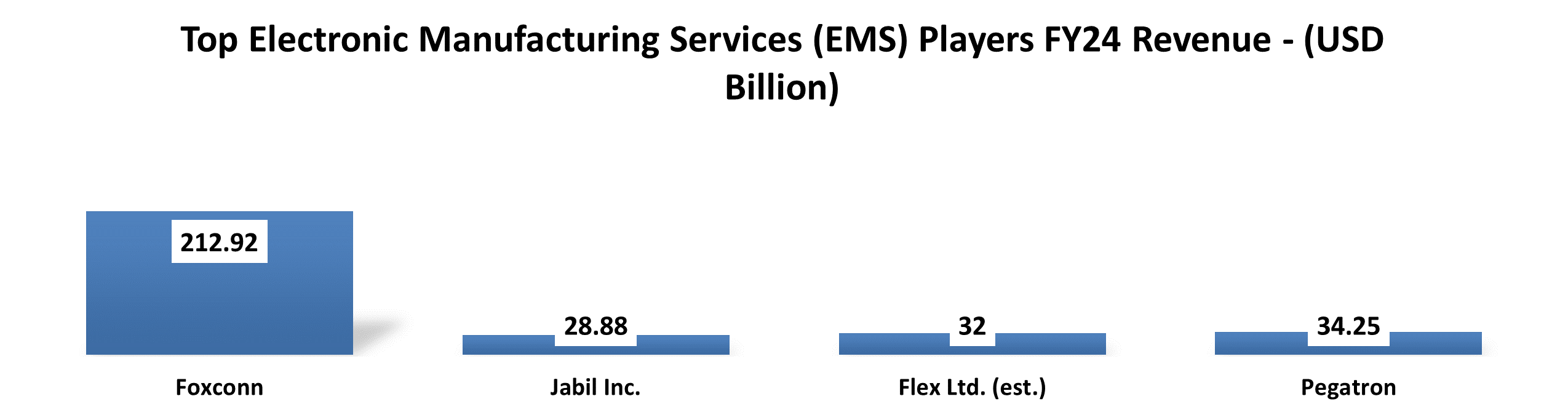

In the electronics manufacturing services (EMS) segment, Foxconn continues to lead with 2024 revenues reaching USD 208 billion, supported by other Tier-1 providers such as Jabil, Flex, and Pegatron. Specialized component leaders like Texas Instruments and Infineon remain pivotal in providing the analog and power solutions essential for the automotive and industrial sectors.

Sources- Mordor Intelligence, Fortune Business Insights, BCC Research, Reed Electronics Research, Straits Research, New Venture Research, Spherical Insights, and UNIDO.

3. Indian Electronic Component Industry:

3.1 Market Size and Growth

The Indian electronics manufacturing sector has evolved from a nascent assembly-focused market into a high-growth global production hub, with production value surging to ₹11.32 lakh crore (approximately US$ 136 billion) in fiscal year 2024–25.

This represents a nearly six-fold increase from the ₹1.9 lakh crore recorded in FY15 . As shown in the market size outlook, the industry has maintained a steady upward trajectory since 2019, when the market was valued at USD 61,643.80 million, and is projected to reach approximately USD 204,500 million by 2029.

Total electronic exports have also seen dramatic expansion, reaching US$ 38.56 billion in FY25, a 32.42% increase from the previous year, which has positioned electronics as India’s third-largest and fastest-growing export category.

3.2 Key Segments

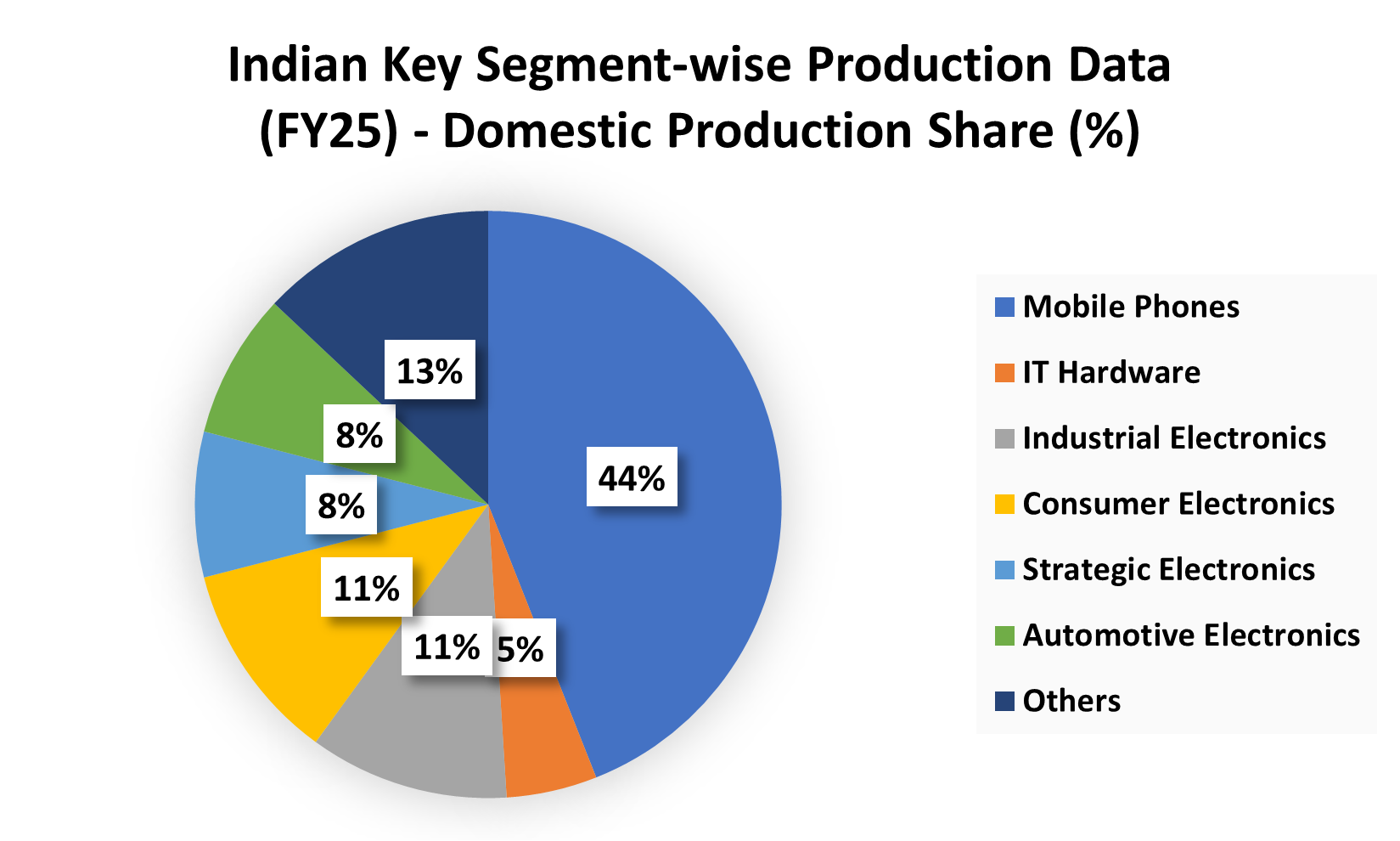

The industry is currently dominated by mobile phone manufacturing, which accounts for approximately 44% of total domestic production value, amounting to ₹5.45 lakh crore by FY25.

While consumer electronics and industrial electronics each represent about 11% to 13% of the production share, the government is aggressively pushing for expansion in IT hardware (laptops, servers, and tablets) through the PLI 2.0 scheme .

Other vital segments contributing to the ecosystem include automotive electronics, which is growing at a 10% CAGR, and strategic electronics for defense and aerospace.

3.3 Regional Highlights

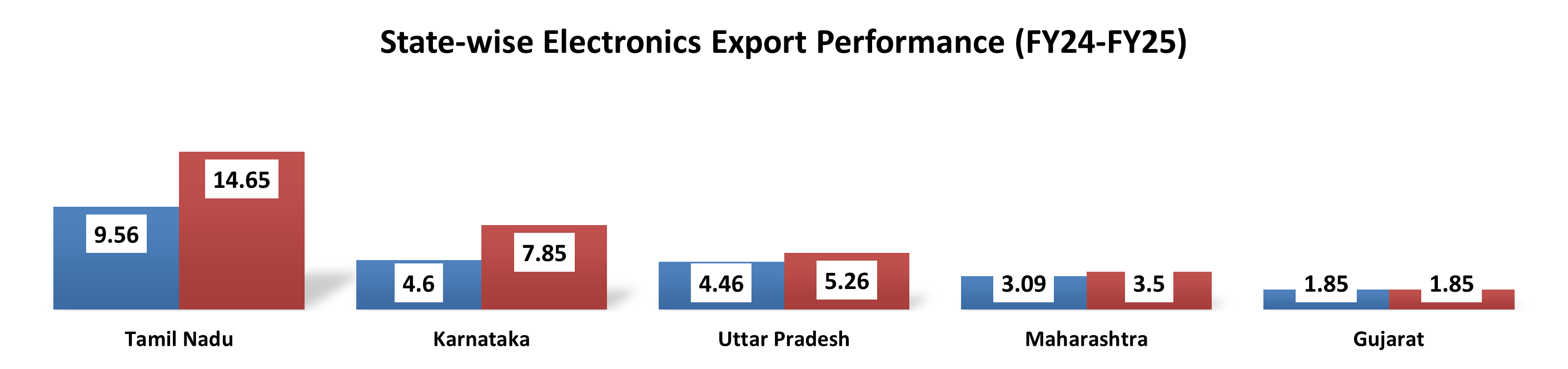

Electronics manufacturing in India is highly clustered in specific industrial zones, with Tamil Nadu emerging as the nation’s primary electronics capital. In FY25, Tamil Nadu accounted for a historic high of 41.23% of India’s total electronics exports, valued at US$ 14.65 billion .

Karnataka follow as the second-highest contributor with a 22.09% share of national exports (US$ 7.85 billion), while Uttar Pradesh holds a 13.63% share, largely driven by the massive mobile manufacturing hub in the Noida-Greater Noida region.

3.4 Technology Drivers

The rapid adoption of 5G infrastructure and the integration of Artificial Intelligence (AI) across devices serve as primary technology drivers, stimulating demand for sophisticated active and passive components .

The Production-Linked Incentive (PLI) schemes have been instrumental in attracting global manufacturers and increasing domestic value addition from 30% to 70% .

Furthermore, the India Semiconductor Mission (ISM) is a critical driver, with projects totaling over ₹1.52 lakh crore in investment approved to build a domestic ecosystem for chip fabrication and advanced packaging.

Sources- Ministry of Electronics and Information Technology (MeitY); PIB; Dataful & technavio.

4. Industry Segmentation:

5. Key Trends/Growth Drivers:

Rapid growth in consumer electronics demand

Consumer electronics such as smartphones, laptops, TVs, and wearables are major consumers of electronic components. For example, producing 1 million smartphones may require 2-3 million integrated circuits, 50-60 million resistors, and 20-30 million capacitors. If global smartphone shipments grow by 5-6% annually, component demand increases proportionally across multiple categories.Expansion of electric vehicles (EVs) and automotive electronics

Modern vehicles are increasingly electronics-driven. A conventional vehicle contains around $400-$500 worth of electronic components, while electric vehicles may contain $1,000-$1,500 worth due to battery management systems, sensors, and power electronics. If EV production grows at 20-25% annually, demand for semiconductors, power modules, and sensors rises significantly.Growth in 5G and telecommunications infrastructure

The global rollout of 5G networks requires advanced semiconductors, RF components, and high-frequency capacitors. A single 5G base station may contain thousands of electronic components, including high-performance chips and connectors. If telecom operators deploy hundreds of thousands of new base stations, component demand rises substantially.Rise of the Internet of Things (IoT)

IoT devices such as smart home products, industrial sensors, and connected appliances rely heavily on microcontrollers and sensors. If the number of connected devices increases from 15 billion to 30 billion globally within a decade, electronic component demand could nearly double for certain categories like sensors and microchips.Industrial automation and robotics adoption

Smart factories and robotics require advanced circuit boards, sensors, controllers, and actuators. If industrial automation spending grows by 10-12% annually, demand for electronic control components and industrial semiconductors increases accordingly.Miniaturization and high-performance electronics

Electronics manufacturers are pushing for smaller, more efficient devices. For example, a modern smartphone motherboard may contain over 1,000 micro components, compared to a few hundred two decades ago. This trend increases the volume of precision electronic components used per device.

Sources: Statista; Grand View Research; Fortune Business Insights; Mordor Intelligence; IMARC Group; International Energy Agency.

6. Industry Risks and Future Challenges:

6.1 High Import Dependence

India remains significantly reliant on imports for electronic components such as semiconductors, PCBs, sensors, and passive components.

Nearly 65–70% of India’s electronic component demand is met through imports

Semiconductor imports alone exceeded $30–35 billion annually in recent years

A substantial portion of these imports originate from China, increasing geopolitical and supply chain risks.

Implication: Supply disruptions, currency fluctuations, and trade restrictions can severely impact domestic manufacturing and cost structures.

6.2 Limited Domestic Value Addition

Despite growth in electronics manufacturing (especially mobile assembly), domestic value addition remains low:

Average value addition in electronics manufacturing is only 15–20%

In mobile manufacturing, localization levels are ~18–22%

Implication: India largely operates as an assembly hub rather than a component manufacturing powerhouse, limiting margin expansion and technological depth.

6.3 Capital Intensity & Technology Barriers

Electronic component manufacturing—especially semiconductors, display units, and advanced PCBs—is highly capital intensive.

Semiconductor fabrication plants (fabs) require investments of $5–10 billion per facility

High-end PCB and EMS facilities require ₹500–1,000 crore+ capex

Implication: High entry barriers restrict domestic capacity creation and favor global incumbents, slowing ecosystem development.

6.4 Supply Chain Concentration Risk

Global electronics supply chains are concentrated in a few countries, particularly Taiwan, South Korea, and China.

Over 75% of global semiconductor fabrication capacity is concentrated in Asia

Taiwan alone accounts for ~60% of advanced chip manufacturing

Implication: Any geopolitical disruption (e.g., Taiwan Strait tensions) can impact component availability and pricing in India.

6.5 Rapid Technological Obsolescence

The electronics industry is characterized by fast innovation cycles:

Product lifecycles in consumer electronics have reduced to 12–24 months

Component specifications (chipsets, sensors, ICs) evolve rapidly

Implication: Inventory obsolescence risk is high, and continuous investment in R&D is required to stay competitive.

6.6 Policy Dependence & Execution Risks

The Indian government has introduced schemes like the Production Linked Incentive (PLI) Scheme to boost domestic manufacturing.

PLI outlay for electronics exceeds ₹38,000 crore

Targets electronics production of $300 billion by 2026

Challenges:

Delays in approvals and disbursements

Execution gaps in infrastructure and logistics

Implication: Policy-driven growth may face delays, affecting investor confidence and project viability.

(Source: Ministry of Electronics & IT (MeitY) – Electronics market data & policy initiatives, India Electronics and Semiconductor Association (IESA) – Industry reports, NITI Aayog – Electronics manufacturing and value addition insights, Semiconductor Industry Association (SIA) – Global supply chain data, Deloitte & EY Reports – Electronics manufacturing trends and projections.)

7. Major Players in India:

7.1 Samsung India Electronics Pvt. Ltd.

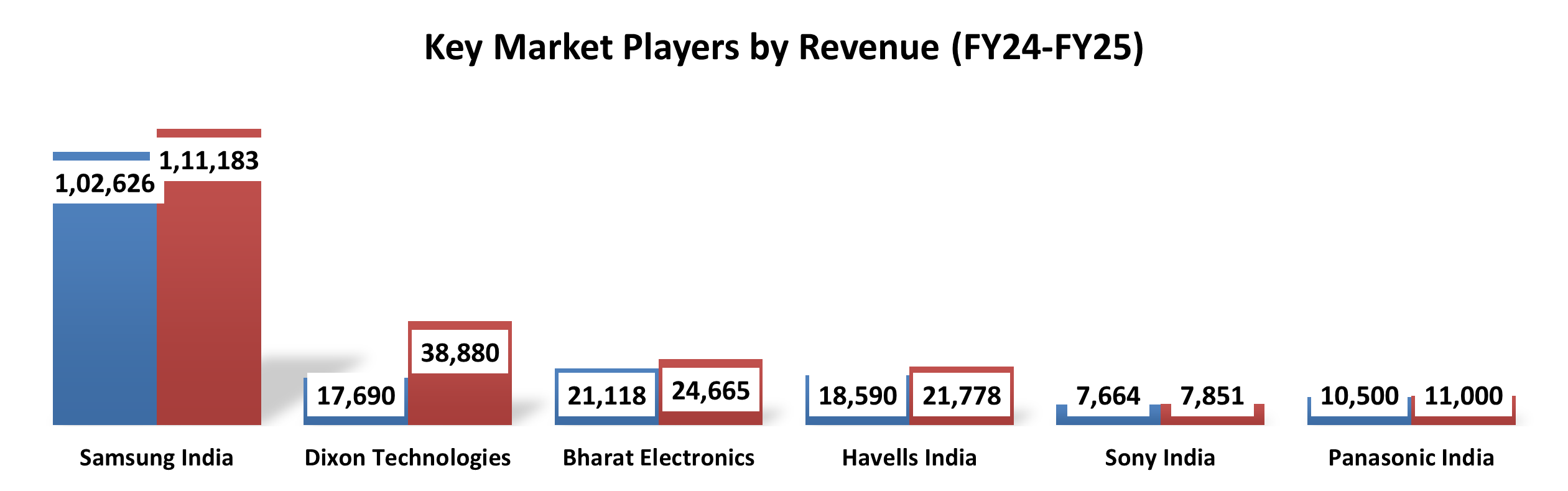

Samsung India is one of the largest electronics manufacturers in the country, operating across smartphones, semiconductors, display components, and consumer electronics. The company plays a critical role in India’s component ecosystem through local manufacturing and supply chain integration. With FY25 revenue of approximately ₹1,11,183 crore, it is the largest player among those listed. Samsung is also actively participating in India’s component localization push under government incentive schemes, strengthening domestic manufacturing capabilities.

7.2 Dixon Technologies (India) Ltd.

Dixon Technologies is India’s leading homegrown Electronics Manufacturing Services (EMS) provider, manufacturing products such as mobile phones, televisions, lighting equipment, and set-top boxes for global brands. The company is expanding into component manufacturing, including display modules and semiconductor assembly. With FY25 revenue of around ₹38,880 crore, Dixon is a key beneficiary of the PLI scheme and aims to deepen backward integration in the electronics value chain.

7.3 Bharat Electronics Ltd.

Bharat Electronics Ltd. (BEL) is a government-owned enterprise specializing in defense electronics, radars, communication systems, and electronic components for strategic applications. With FY25 revenue of approximately ₹24,665 crore, BEL is a dominant player in high-value, technology-intensive electronics manufacturing. Its strong R&D capabilities and focus on indigenization make it a key contributor to India’s electronic component ecosystem.

7.4 Havells India Ltd.

Havells India operates across electrical equipment, consumer appliances, and electronic components such as switchgear, cables, and lighting systems. The company has been increasing its focus on electronics and smart devices. With FY25 revenue of about ₹21,778 crore, Havells benefits from strong domestic demand and growing premiumization trends in electrical and electronic products.

7.5 Sony India Pvt. Ltd.

Sony India is a subsidiary of the global electronics giant and operates in segments such as consumer electronics, imaging devices, and electronic components. With FY25 revenue of approximately ₹7,851 crore, the company contributes to India’s high-end electronics ecosystem, particularly in imaging sensors and premium electronic devices. Sony also relies on global supply chains while gradually increasing local sourcing.

7.6 Panasonic India Pvt. Ltd.

Panasonic India is a diversified electronics manufacturer involved in consumer electronics, industrial devices, automotive electronics, and components. With FY25 revenue of around ₹11,000 crore, the company has a strong presence in appliances and electronic components, and continues to invest in India as a manufacturing hub for both domestic and export markets.

8. Conclusion:

The Indian electronic components industry is at a pivotal stage of transformation, driven by strong domestic demand, increasing digitalization, and supportive government initiatives such as the Production Linked Incentive (PLI) Scheme. With India targeting electronics production of ~$300 billion by 2026, the role of a robust domestic component ecosystem has become increasingly critical.

While the industry has witnessed rapid growth in electronics manufacturing, particularly in mobile assembly and consumer devices, domestic value addition remains relatively low at ~15–20%, reflecting continued reliance on imports for key components such as semiconductors and advanced electronics. This dependence exposes the sector to global supply chain disruptions and pricing volatility.

Leading players such as Samsung India Electronics Pvt. Ltd., Dixon Technologies (India) Ltd., Bharat Electronics Ltd., Havells India Ltd., Sony India Pvt. Ltd., and Panasonic India Pvt. Ltd. reflect a mix of global OEMs, domestic EMS providers, and strategic public sector enterprises shaping the ecosystem. Their increasing focus on localization, backward integration, and advanced manufacturing is expected to gradually strengthen India’s position in the global value chain.

However, challenges such as high capital intensity, technology gaps, infrastructure constraints, and rapid technological obsolescence continue to limit the pace of ecosystem development. The industry must also adapt to emerging trends such as electric vehicles, 5G, IoT, and semiconductor manufacturing, which require significant investments in R&D and capability building.

Overall, the Indian electronic components industry offers strong long-term growth potential, supported by structural demand drivers and policy support. The transition from an assembly-led ecosystem to a high-value, innovation-driven manufacturing base will be the key determinant of sustainable competitiveness in the coming years.

THANK YOU FOR READING!!

Researched By- Naresh and Mayank.

Hope you liked our work. Please Subscribe so that we can reach out to more People like you!

We are Proud to Announce Our New Launch of the Premium services where we Deep-dive into the Business and back you up with Robust Research.

We Provide services for different Level of Investors. You can Email us directly to start your journey!