Industry Report: Education Technology Industry

From Pandemic Boom to Profit Test: The New Phase of EdTech

Here, at EquityEdge Research, we deep dive into complex Articles and Reports and make it easier for you by presenting everything, RIGHT HERE!!

Please Fill the form Below if you are interested in our Services and would like a Free Sample of our Equity Research Report covering a Small/Micro-cap Company.

Check out our Previous Industry Report:

What do you mean by the Education Technology Industry?

Global Education Technology Industry.

Indian Education Technology Industry.

Industry Segmentation.

Key Trends/Growth Drivers:

Industry Risk and Future Challenges.

Major Players in India.

Conclusion.

1. What do you mean by the Education Technology Industry?

The education technology (EdTech) industry refers to the sector that integrates digital technology with education to enhance teaching, learning, and administrative processes. It includes the development and delivery of software platforms, online courses, virtual classrooms, learning management systems, and educational applications that facilitate remote and personalized learning. The industry serves a wide range of users, including schools, universities, corporate training programs, and individual learners, offering solutions such as video-based learning, AI-driven assessments, adaptive learning systems, and skill development platforms. The value chain typically involves content creation, platform development, distribution through web and mobile applications, and continuous user engagement through analytics and feedback systems. Growth in the EdTech industry is driven by increasing internet penetration, rising smartphone usage, demand for flexible and affordable education, and the shift toward digital learning models, making it a rapidly expanding segment within the global education ecosystem.

Sources: Statista; HolonIQ; Grand View Research; Fortune Business Insights; Mordor Intelligence.

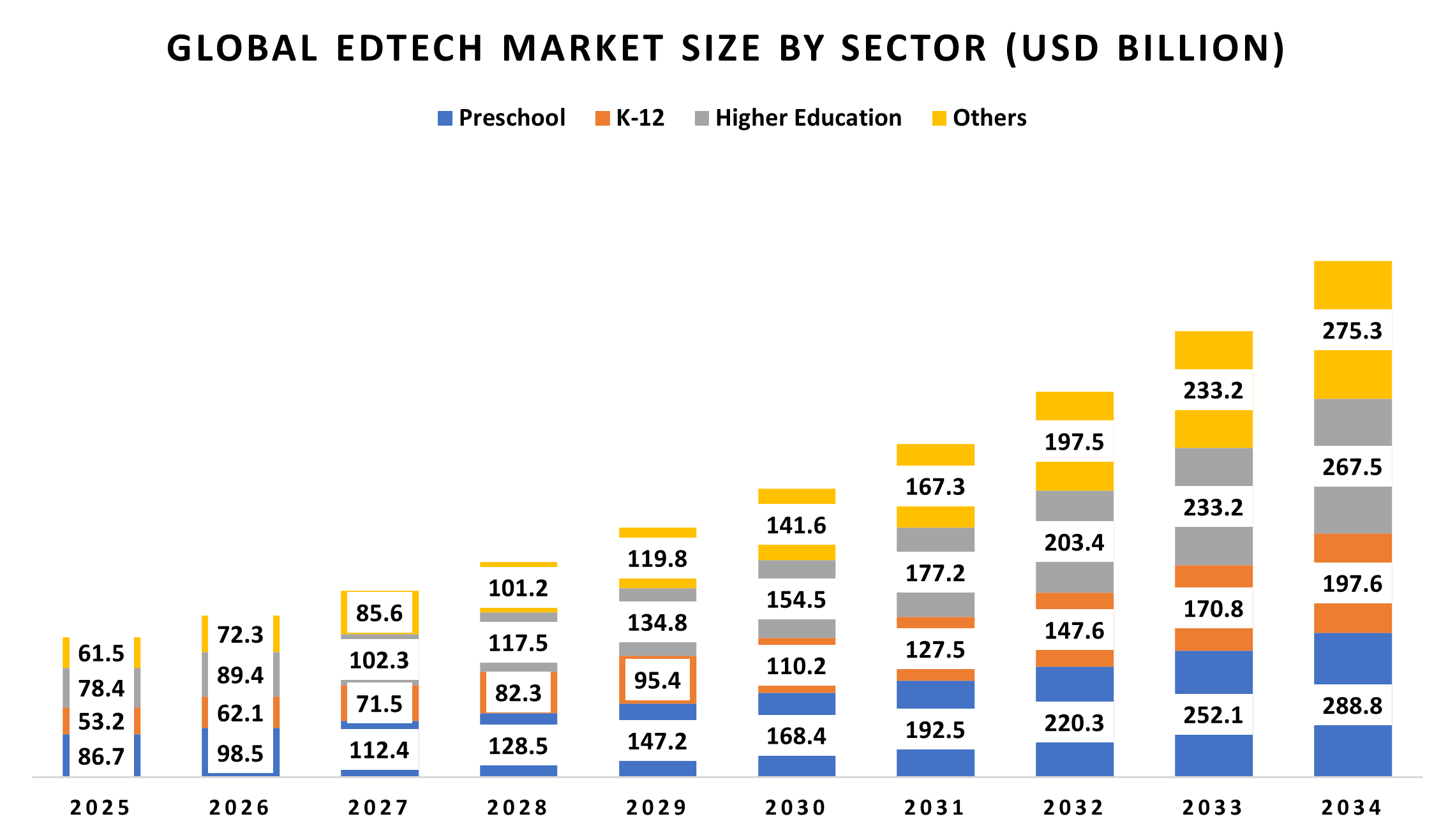

2. Global Education Technology Industry:

2.1 Market Size and Growth

The global education technology market is entering a phase of rapid expansion, currently valued at approximately $214.2 billion in 2026.

This trajectory is supported by a robust compound annual growth rate of over 14%, with projections suggesting the market could exceed $545 billion by 2032.

This growth is largely fueled by the massive shift toward cloud-based infrastructure, which now accounts for nearly 57% of the total market share, as educational institutions replace legacy on-premise systems with more flexible, interoperable digital ecosystems.

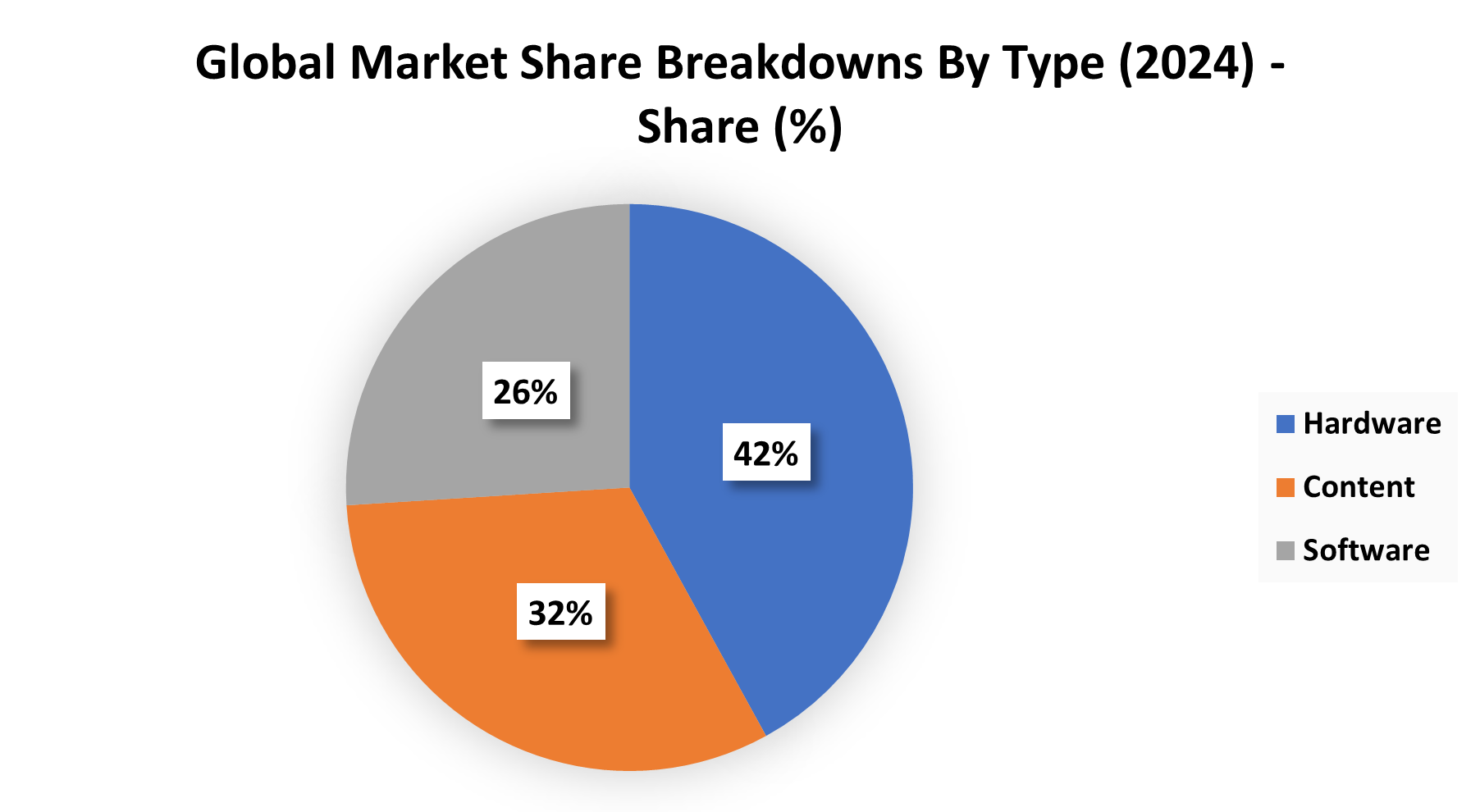

2.2 Key Segments

The industry is categorized into hardware, software, and content, with hardware currently maintaining a dominant lead at over 40% of the market value.

However, the K-12 and Higher Education sectors are the primary revenue drivers, with Higher Education alone commanding a 45% share as universities compete to offer hybrid and career-focused degree programs.

Specialized niches, such as language learning platforms and corporate upskilling, are also seeing significant upticks, reflecting a global emphasis on workforce mobility and lifelong learning.

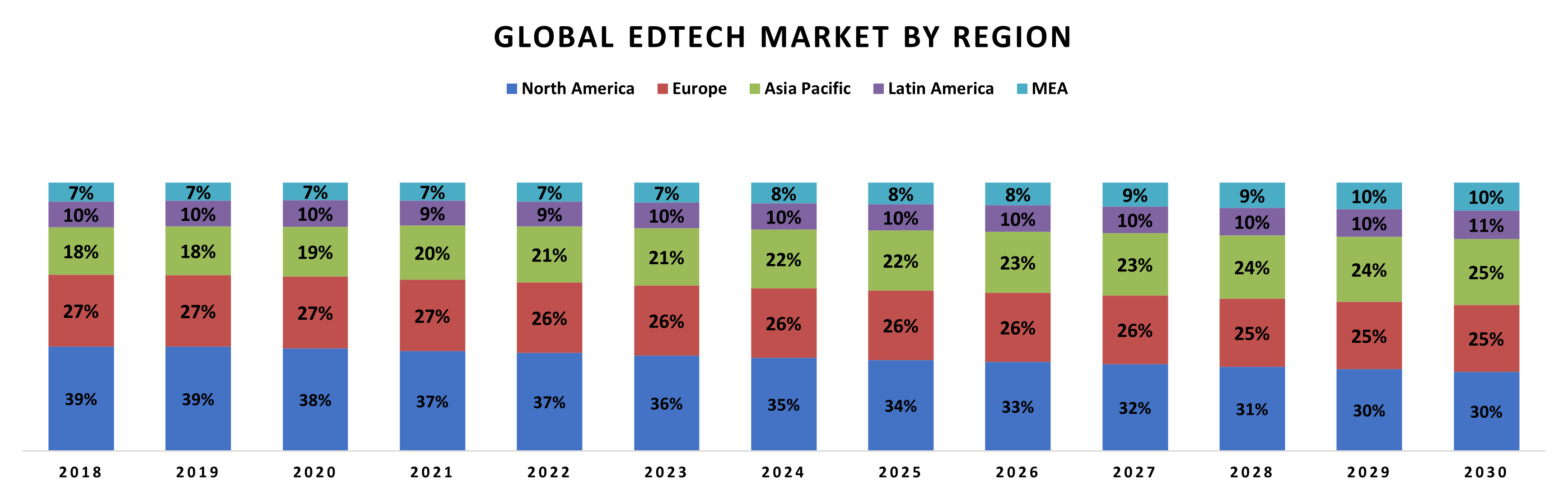

2.3 Regional Highlights

North America remains the largest regional market, holding roughly 36% of the global share due to its mature digital infrastructure and heavy investment in AI-driven personalized learning.

In contrast, the Asia-Pacific region is the fastest-growing market, projected to hold 28% of the global share by the end of 2026.

India has emerged as a critical hub, not only as a primary source for outbound students but also as a leading market for digital curriculum tools and early childhood education technology.

2.4 Technology Drivers

Artificial Intelligence and Machine Learning are the most significant catalysts for change, transitioning from experimental tools to core components of the digital architecture.

These technologies enable hyper-personalized learning paths that adapt in real-time to student performance and engagement. Additionally, immersive technologies like Augmented and Virtual Reality (AR/VR) are becoming standard in STEM education, while blockchain is increasingly used to provide secure, verifiable digital credentials for academic and professional achievements.

2.5 Key Challenges

Despite the rapid growth, the industry faces substantial hurdles, most notably the digital divide and infrastructure limitations in developing regions.

Data privacy and cybersecurity have become paramount concerns as educational ecosystems expand, requiring more sophisticated encryption and ethical oversight.

Furthermore, there is a growing challenge for educators to distinguish between general-purpose AI tools that merely boost task performance and specialized pedagogical tools that actually facilitate deep, long-term learning.

2.6 Major Industry Participants

The competitive landscape is a mix of established global giants and specialized service providers. Leading players such as IDP Education, Navitas, and Study Group dominate the student recruitment and pathway sectors, while technology-first companies like ApplyBoard and Leverage Edu are redefining how students access global opportunities through digital platforms.

Additionally, major content and software providers like Kaplan and Global University Systems (GUS) continue to hold significant influence by integrating technology directly into institutional operations and student support services.

Sources- Source: Grand View Research , Fortune Business Insights, IMARC Services Private Limited.

3. Indian Education Technology Industry:

3.1 Market Size and Growth

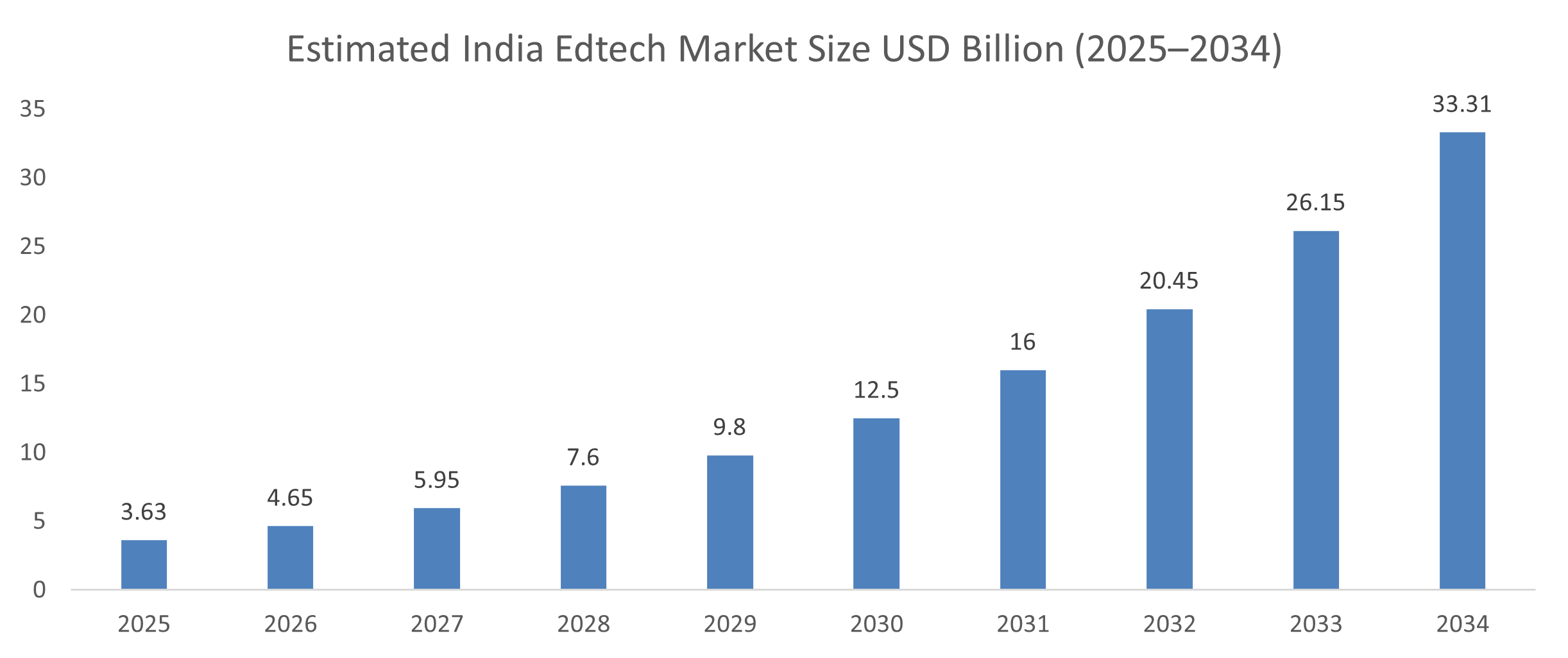

The Indian Edtech market has entered a sophisticated phase of maturity following the heavy consolidation of the mid-2020s. As of early 2026, the industry is valued at approximately USD 7.5 Billion when accounting for the massive shift toward hybrid-offline centers.

This sector is maintaining a powerhouse trajectory with a Compound Annual Growth Rate (CAGR) of 27.94%, positioning it to potentially cross the USD 33 Billion mark by 2034.

This growth is no longer driven by pandemic-era necessity but by a fundamental shift in the Indian middle-class “education wallet,” where digital supplements are now viewed as essential rather than optional.

3.2 Key Segments

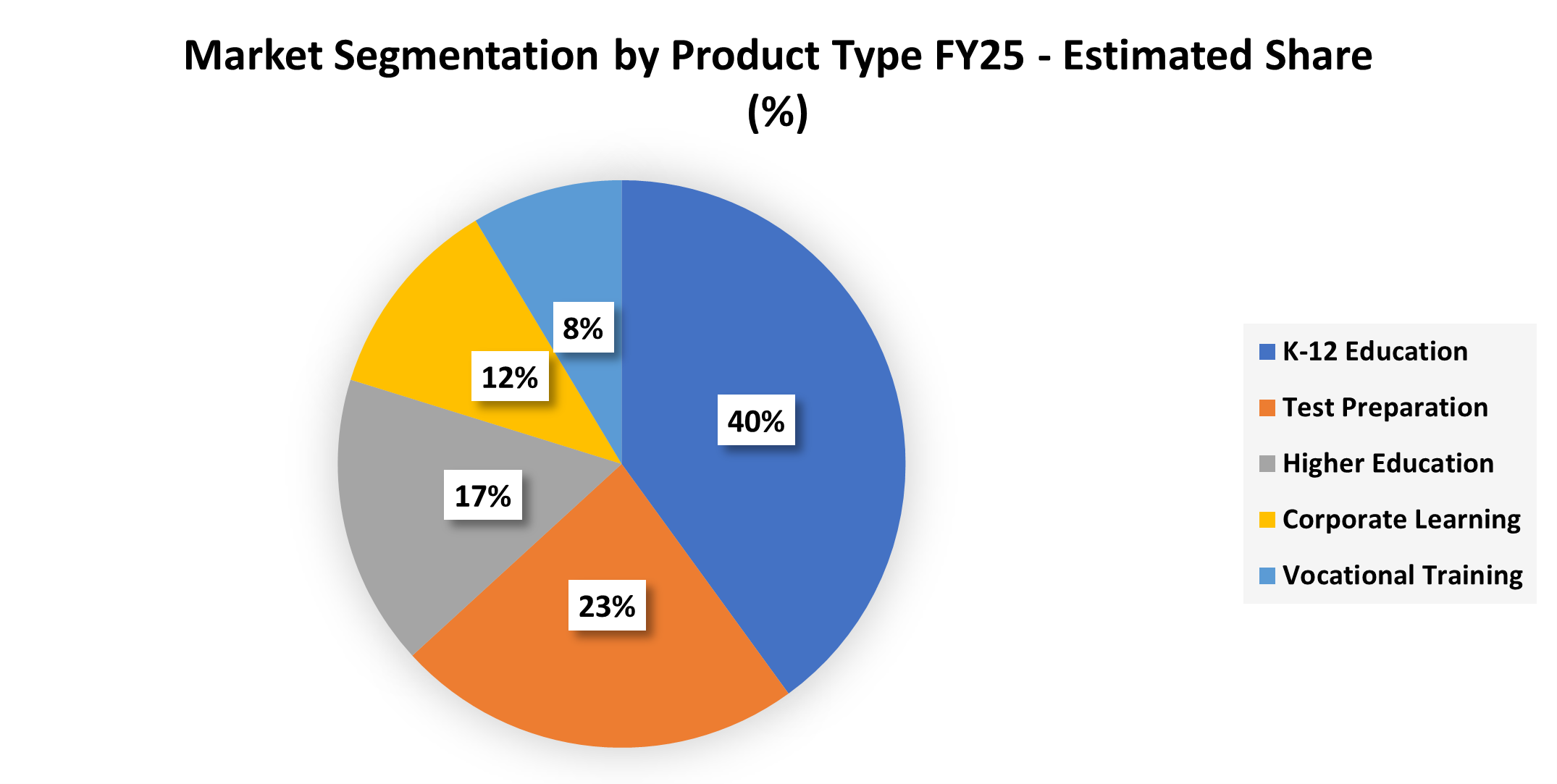

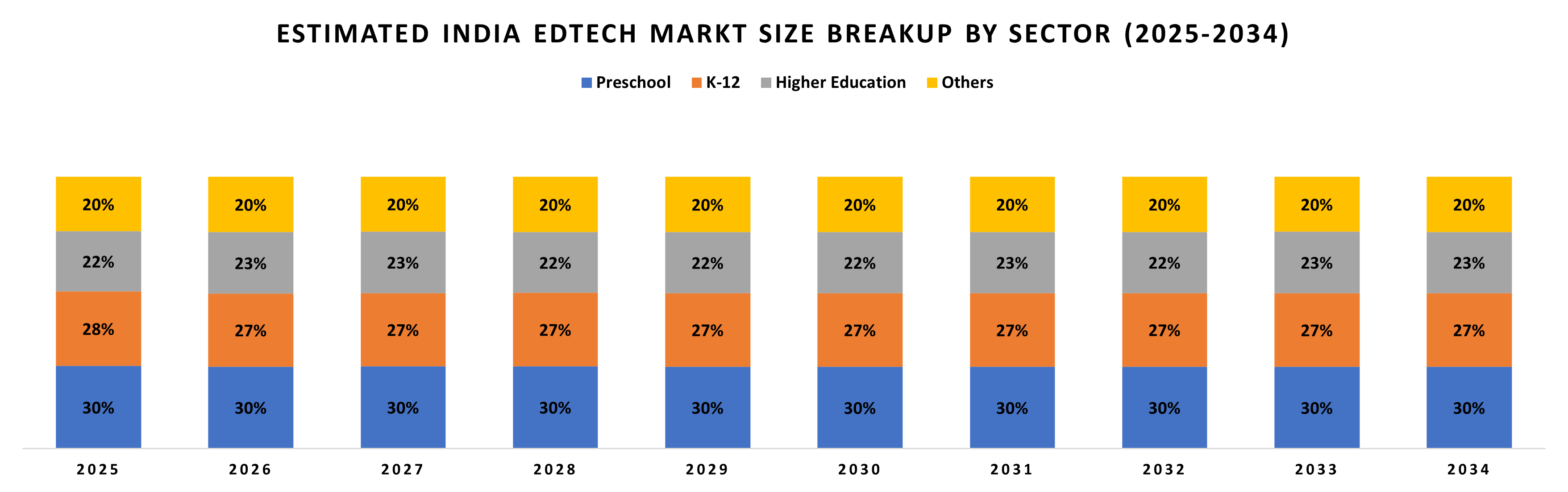

The K-12 segment continues to serve as the industry’s bedrock, commanding a dominant 43% market share by providing digital curriculum support to India’s massive school-age population.

Closely following is the Test Preparation vertical, which remains the most lucrative due to the high-stakes nature of competitive exams like JEE, NEET, and UPSC.

Meanwhile, the Higher Education and Upskilling segment has carved out a significant niche by focusing on “degree-linked” outcomes, where platforms partner with universities to offer recognized credentials to working professionals.

3.3 Regional Highlights

North India remains the primary revenue engine, contributing roughly 30% of the total market share due to the concentrated presence of established coaching hubs and high digital literacy in the National Capital Region.

However, the most compelling story of 2026 is the “Vernacular Surge” in Tier-2 and Tier-3 cities. Regions across Western and Southern India are seeing rapid adoption as platforms move away from English-only content, instead offering comprehensive courses in regional languages to tap into the next 100 million learners who were previously underserved by high-cost urban models.

3.4 Technology Drivers

The technological landscape has shifted from simple video streaming to the era of Agentic AI. Today’s leading platforms utilize autonomous AI tutors that can sense a student’s cognitive load and adjust the difficulty of a lesson in real-time without human intervention.

Furthermore, cloud-based deployment has become the industry standard, representing over 80% of the infrastructure. This shift has allowed for the delivery of high-quality interactive content even in low-bandwidth rural environments, effectively bridging the geographical gap in educational quality.

Sources- Source: IMARC, Ken Research Analysis.

4. Industry Segmentation:

5. Key Trends/Growth Drivers:

5.1 Rapid increase in internet and smartphone penetration

EdTech adoption is highly correlated with digital access. For example, if internet penetration in a country rises from 50% to 70% across a population of 1.4 billion, that adds 280 million new potential online learners, directly expanding the addressable market for EdTech platforms.

5.2 Shift toward online and hybrid learning models

Institutions are increasingly adopting blended learning (offline + online). If a university with 10,000 students moves 30% of its curriculum online, it creates demand for learning management systems, digital content, and assessment tools at scale.

5.3 Rising demand for skill-based and employability-focused courses

Traditional degrees are being supplemented with short-term certification programs. For instance, if 20% of graduates (say 5 million out of 25 million annually) enroll in online skill courses, it creates a massive recurring revenue stream for EdTech platforms.

5.4 Growth in corporate training and upskilling

Companies are investing in employee training to keep up with technological change. If a firm with 10,000 employees allocates ₹10,000 per employee annually for digital training, that represents a ₹100 crore market opportunity from just one large enterprise.

5.5 Adoption of AI-driven personalized learning

EdTech platforms are increasingly using AI to tailor content to individual learners. For example, adaptive learning systems can improve completion rates from 40% to 60%, increasing user retention and lifetime value for platforms.

5.6 Expansion of K-12 digital education

Parents are increasingly supplementing school education with online tutoring. If 30% of K-12 students in a country of 250 million students adopt EdTech solutions, that implies a user base of 75 million students, significantly driving platform growth.

Sources: Statista; HolonIQ; Grand View Research; Fortune Business Insights, Mordor Intelligence and World Bank.

6. Industry Risks and Future Challenges:

6.1 Profitability Challenges & High Customer Acquisition Costs

Many Indian EdTech companies operate on aggressive marketing-led growth strategies, leading to high customer acquisition costs (CAC) and delayed profitability.

Several major EdTech firms have reported significant losses in recent years

Marketing expenses for large platforms often range between 20–30% of revenue

Subscription-based models face high churn rates, particularly in K-12 segments

This creates sustainability risks, especially when funding slows or growth moderates.

Additionally, the sector has witnessed valuation corrections, including the sharp decline of once-highly valued companies, highlighting financial sustainability concerns.

6.2 Funding Volatility & Investment Cycles

The Indian EdTech sector saw massive funding during the pandemic, followed by a slowdown post-2022.

Funding declined significantly after COVID-19 demand normalized

Investment rebounded partially in H1 2025 with a ~5x increase, driven by AI-focused platforms and upskilling solutions

However, investor focus has shifted toward profitability rather than growth

This creates uncertainty for startups dependent on venture capital.

6.3 High Competition & Market Fragmentation

The Indian EdTech market is highly fragmented with 3,000+ startups operating across segments such as:

Test preparation

K-12 learning

Skill development

Higher education

Study abroad

Fragmentation leads to:

Price competition

High marketing expenses

Lower customer retention

Moreover, K-12 dominates the EdTech market with ~43% share, intensifying competition in this segment.

6.4 Digital Infrastructure & Accessibility Constraints

Although India has over 800 million internet users, digital access quality remains uneven across rural areas.

Key constraints include:

Limited broadband penetration in rural regions

Device affordability issues

Low digital literacy in certain demographics

These challenges limit adoption and scalability, particularly outside urban markets.

6.5 Low Engagement & Learning Outcome Concerns

EdTech platforms face engagement challenges, especially in long-duration courses:

Course completion rates in online learning platforms typically range between 10–20% globally

Students often prefer hybrid learning over fully online models

This creates retention challenges and reduces subscription renewals.

6.6 Regulatory & Policy Risks

The education sector is highly regulated in India. Increasing scrutiny on:

Misleading advertising

Course pricing

Student financing schemes

Data privacy and student protection

could impact growth models.

Government intervention and policy changes may increase compliance costs for EdTech companies.

(Sources: India Brand Equity Foundation – Indian EdTech Market Growth, Grand View Research – Market Size & CAGR, IMARC Group – Market Share & Segment Data, Reuters & Economic Times – EdTech funding and valuation developments, Industry reports from IAMAI and Grant Thornton.)

7. Major Players in India:

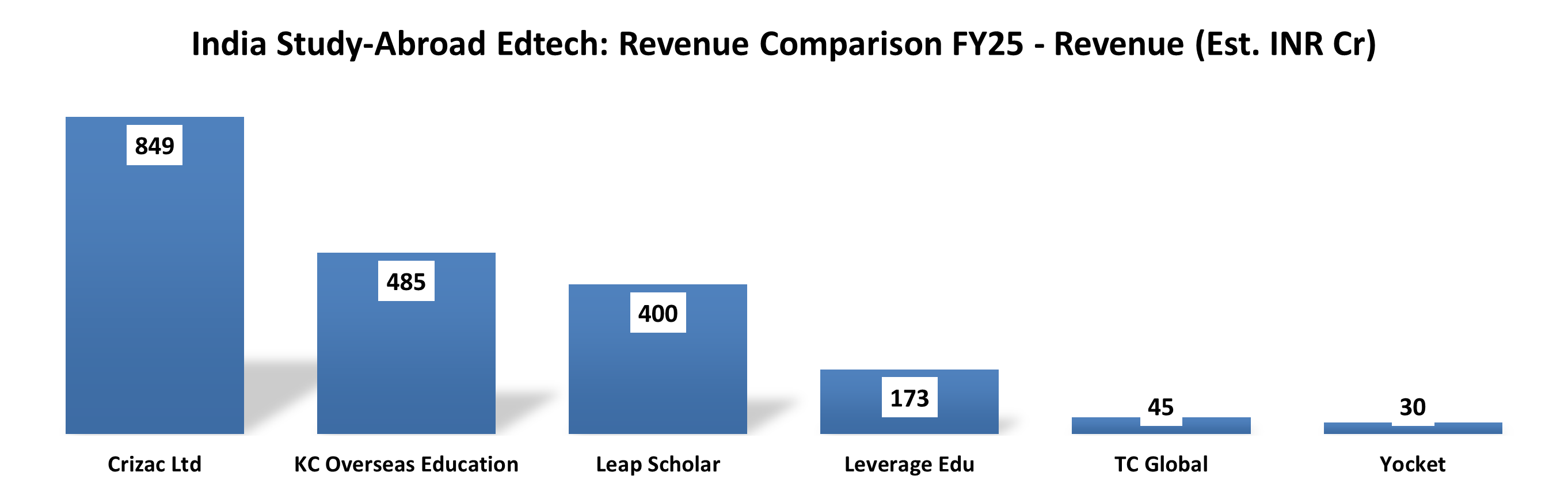

7.1 Crizac Ltd.

Crizac Ltd. is one of the leading study-abroad focused EdTech platforms that provides student recruitment and admission solutions to international universities across the UK, Canada, Ireland, Australia, and New Zealand. The company operates a technology-driven platform connecting agents, students, and institutions globally. In FY25, Crizac reported revenue of approximately ₹849 crore, making it the largest player among those listed. The company processed 2.76 lakh student applications across 75+ countries and maintains partnerships with 173 global universities, highlighting its strong scale and global reach.

7.2 KC Overseas Education

KC Overseas Education is a prominent overseas education consultancy offering services such as university admissions, visa assistance, and career counseling. The company has expanded its presence across India and international markets including Southeast Asia and Africa. With estimated FY25 revenue of ₹485 crore, KC Overseas benefits from growing demand for international education among Indian students. Its hybrid model combining digital platforms with physical counseling centers supports scalable student acquisition.

7.3 Leap Scholar

Leap Scholar is one of India’s fastest-growing study-abroad platforms offering IELTS preparation, university admissions, financial services, and visa support. The platform has helped 500,000+ students pursue overseas education and partnered with 750+ global universities. The company has raised significant funding from global investors and continues to expand its digital-first ecosystem. With estimated FY25 revenue of ₹400 crore, Leap Scholar remains a key technology-driven player in the study-abroad segment.

7.4 Leverage Edu

Leverage Edu provides AI-based university matching, admission support, test preparation, and student financing solutions. The company focuses on simplifying overseas education through a digital-first approach. With estimated FY25 revenue of ₹173 crore, Leverage Edu has expanded rapidly through partnerships with universities and financial institutions. The company is also investing in AI-driven counseling tools and end-to-end student lifecycle management.

7.5 TC Global

TC Global is one of the older players in the international education space, operating since 1995 and providing student recruitment, global university partnerships, and career guidance services. The company has built a strong alumni and institutional network across multiple countries. With estimated FY25 revenue of ₹45 crore, TC Global continues to focus on community-driven global education platforms and hybrid counseling services.

7.6 Yocket

Yocket is a digital-first study-abroad platform offering university discovery, application tracking, counseling, and community-based student engagement. The platform primarily targets technology-savvy students and operates through a mobile-first model. With estimated FY25 revenue of ₹30 crore, Yocket remains a smaller but growing player in the Indian study-abroad EdTech ecosystem.

Estimates: For the remaining private companies, figures are based on their student placement volumes and the average industry commission rates.

8. Conclusion:

The Indian study-abroad EdTech industry is witnessing strong structural growth, supported by rising outbound student mobility, increasing disposable incomes, and growing preference for international education. India is projected to have ~2 million students studying abroad by 2027, compared to approximately 1.3 million in 2023, highlighting a significant long-term demand opportunity for study-abroad platforms.

Leading players such as Crizac Ltd., KC Overseas Education, Leap Scholar, Leverage Edu, TC Global, and Yocket are shaping the competitive landscape through technology-driven platforms, university partnerships, and end-to-end student services. These companies are increasingly expanding into value-added offerings such as test preparation, student financing, visa support, and career counseling to enhance monetization and customer retention.

However, the industry remains exposed to regulatory risks in destination countries, visa policy changes, currency volatility, and increasing competition among platforms. Additionally, dependence on key destinations such as the US, UK, Canada, and Australia creates concentration risk, while rising marketing costs and student acquisition expenses may impact profitability.

Despite these challenges, long-term growth prospects remain strong, driven by India’s large student base, increasing global mobility, and digital platform adoption. Companies focusing on diversified destination markets, technology-enabled counseling, and integrated service offerings are likely to emerge as long-term leaders. Overall, the Indian study-abroad EdTech industry is expected to witness steady growth with increasing consolidation, as players scale operations and strengthen global partnerships.