Here, at EquityEdge Research, we deep dive into complex Articles and Reports and make it easier for you by presenting everything, RIGHT HERE!!

Please Fill the form Below if you are interested in our Services and would like a Free Sample of our Equity Research Report covering a Small/Micro-cap Company.

Check out our Previous Industry Report:

Industry Report: Machine Tools Industry

Here, at EquityEdge Research, we deep dive into complex Articles and Reports and make it easier for you by presenting everything, RIGHT HERE!!

What do you mean by the E-waste management Industry?

Global E-waste management Industry.

Indian E-waste management Industry.

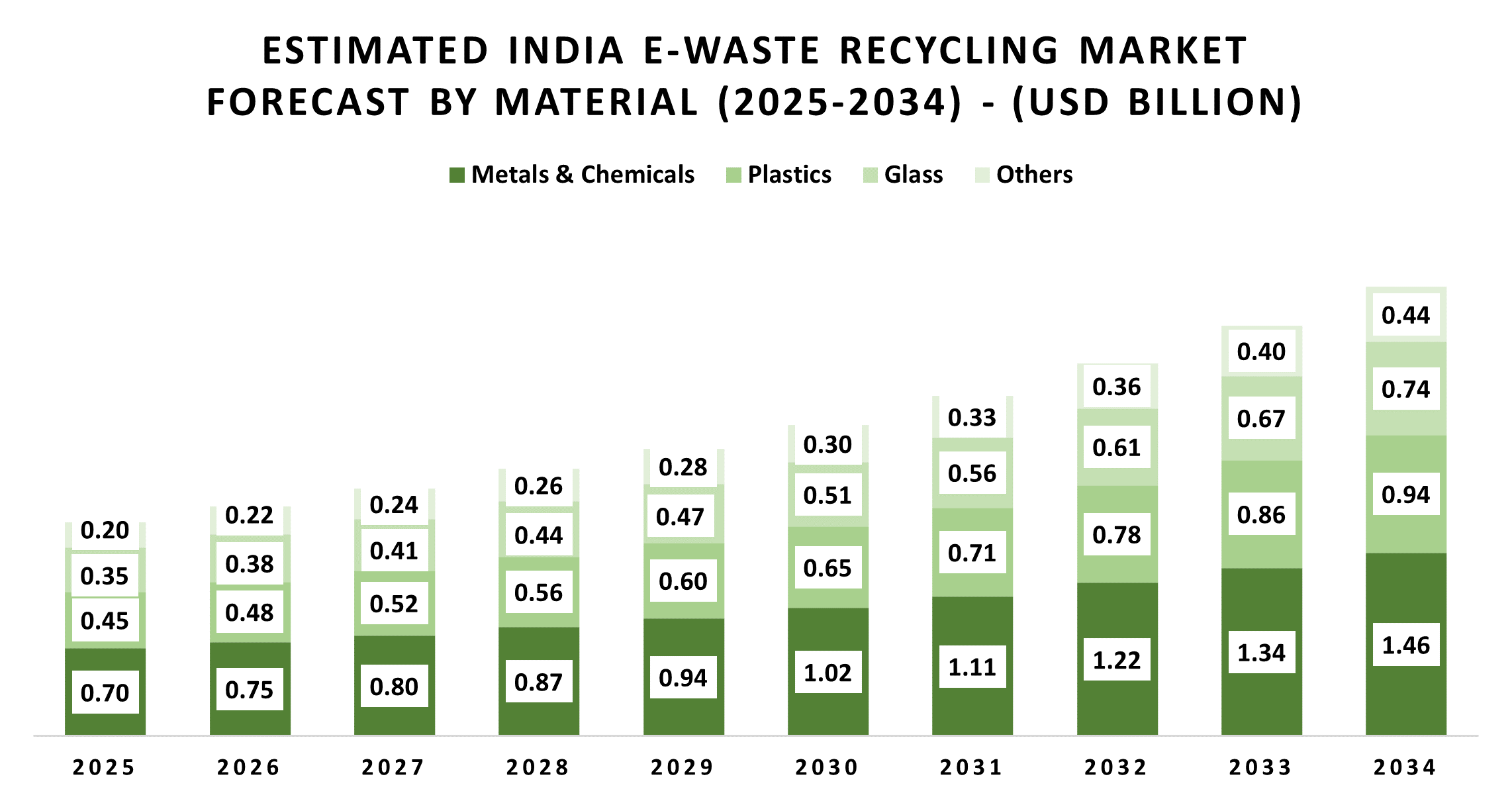

Industry Segmentation.

Key Trends/Growth Drivers.

Industry Risk and Future Challenges.

Major Players in India.

Conclusion.

1. What do you mean by the E-waste management Industry?

The e-waste management industry refers to the sector involved in the collection, recycling, treatment, disposal, and recovery of electronic waste generated from discarded electrical and electronic devices such as smartphones, computers, televisions, batteries, appliances, and industrial electronics. The industry aims to safely manage hazardous materials like lead, mercury, and cadmium present in electronic products while recovering valuable materials such as gold, silver, copper, aluminum, and rare earth metals for reuse. The value chain includes e-waste collection, segregation, dismantling, recycling, material recovery, refurbishment, and environmentally safe disposal. The industry serves governments, businesses, manufacturers, and consumers by reducing environmental pollution, supporting circular economy practices, and minimizing the need for virgin raw material extraction. Growth in the e-waste management industry is driven by rapid technological advancements, shorter electronic product life cycles, increasing electronic consumption, stricter environmental regulations, and rising awareness regarding sustainable waste management practices.

Sources: United Nations Environment Programme; World Health Organization; Global E-waste Statistics Partnership; Grand View Research; Fortune Business Insights

2. Global E-waste management Industry:

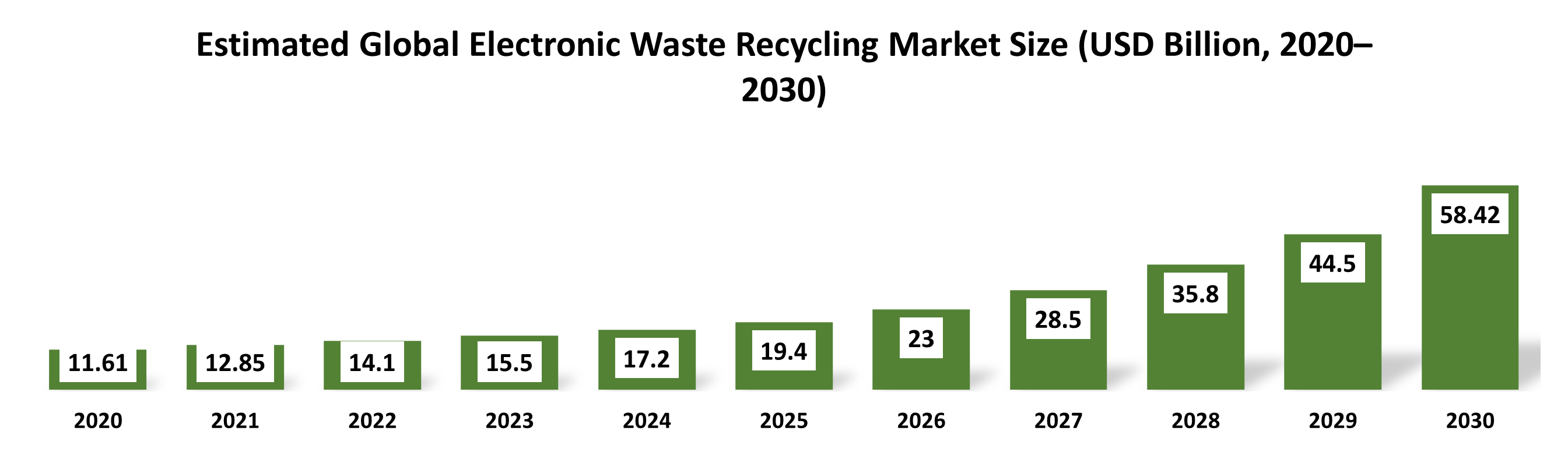

2.1 Market Size and Growth

The global electronic waste recycling market is undergoing a period of rapid expansion, projected to grow from roughly $19.4 billion in 2025 to approximately $58.4 billion by 2030.

This trajectory represents an accelerating compound annual growth rate of 22% for the 2025–2030 period.

The surge is primarily driven by the increasing volume of discarded electronics, estimated to reach nearly 75 million tonnes by 2026 and a global shift toward circular economy models that view e-waste as a source of secondary raw materials rather than mere refuse.

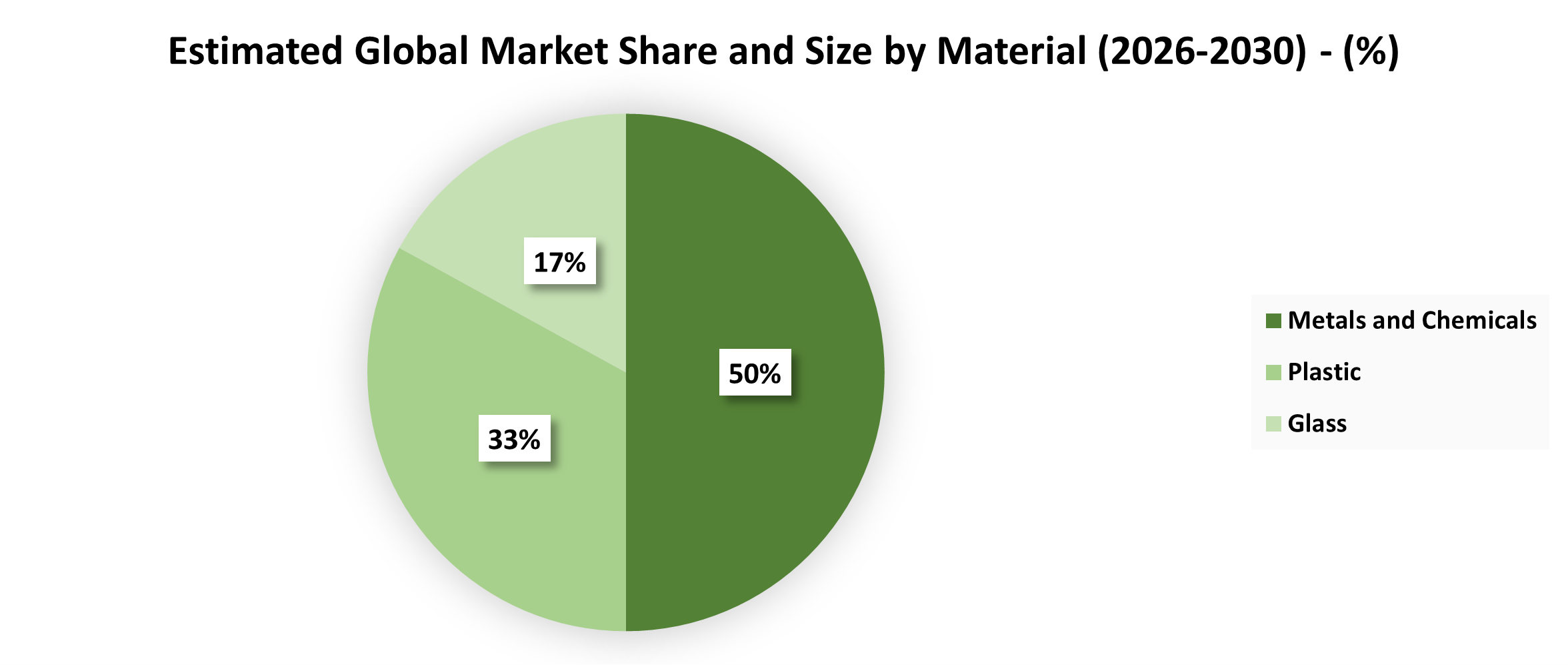

2.2 Key Segments

The industry is structured around three primary material segments: metals and chemicals, plastics, and glass.

Metals and chemicals dominate the market, accounting for approximately 50% of total value due to the high recovery potential of gold, silver, copper, and rare earth elements from circuit boards and batteries.

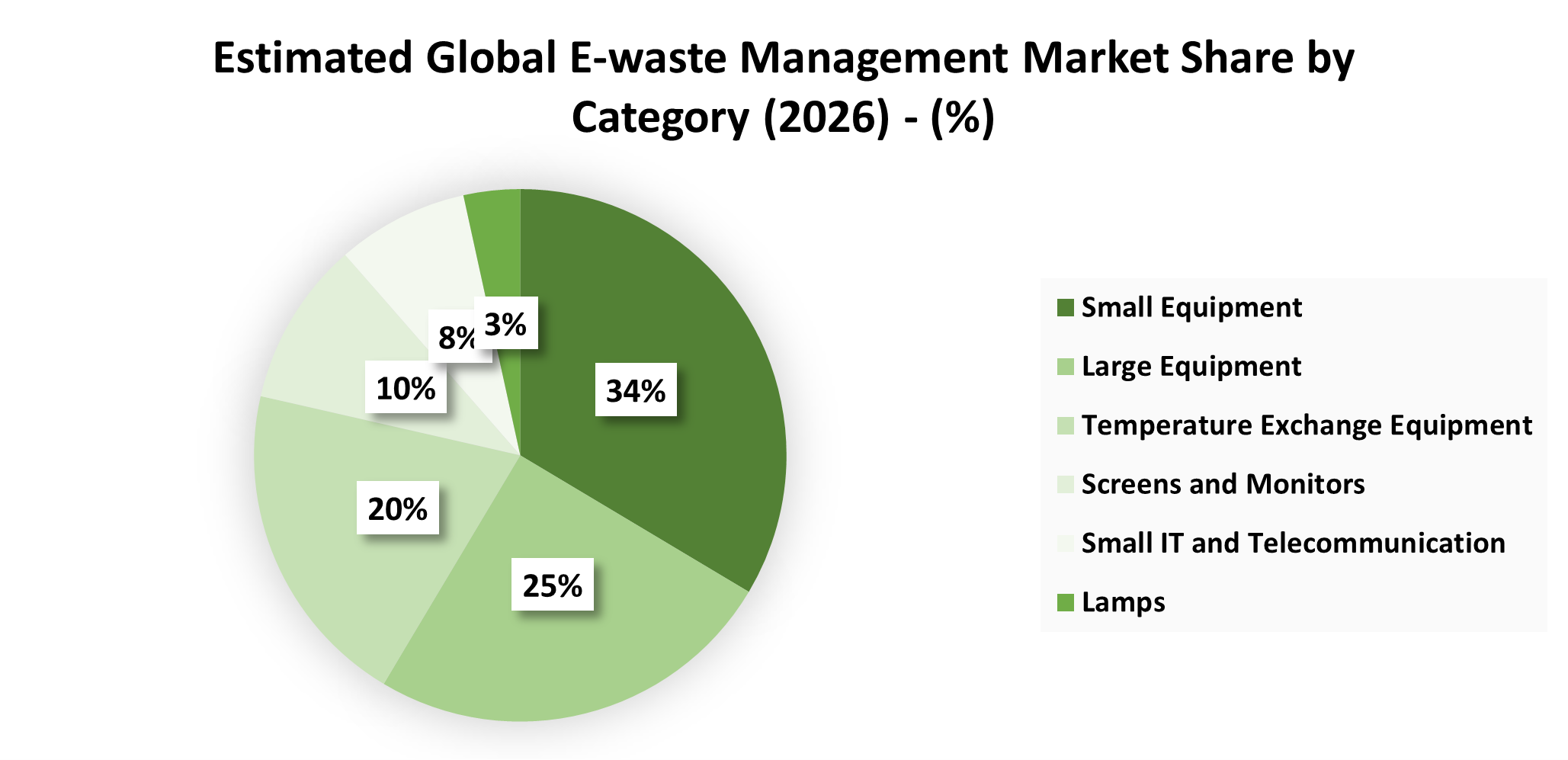

From a category perspective, small equipment, including personal gadgets and household appliances remains the largest source of e-waste, currently representing over 33.57% of the global market share.

Regional Highlights

Regionally, the Asia-Pacific market is the most significant growth engine, fueled by massive electronics consumption in countries like China and India.

By 2026, the region’s e-waste volume is expected to hit 26.41 million tons, outperforming North America in terms of growth rate.

Meanwhile, Europe maintains a leadership position in formal recycling infrastructure and regulatory maturity, holding a substantial portion of the global value and driving high recovery standards through strict environmental directives.

2.3 Technology Drivers

Technology acts as the primary catalyst for modernizing the sector, with AI-powered sorting systems and robotic dismantling now reaching commercial scale.

These innovations allow facilities to segregate complex materials with higher precision and speed than manual labor. Additionally, advancements in hydrometallurgical processing and “urban mining” techniques are making it economically viable to extract high-purity rare earth minerals, reducing the industry’s reliance on traditional, environmentally taxing mining operations.

2.4 Key Challenges

Despite technological progress, the industry faces significant hurdles, most notably the lack of formal collection infrastructure in developing nations, where up to 40% of e-waste still ends up in informal sectors.

“Planned obsolescence” and shorter device lifecycles continue to outpace recycling capacity, creating a mounting backlog of hazardous waste.

Furthermore, the complexity of modern hardware, which often uses adhesives and integrated batteries, makes cost-effective dismantling difficult without specialized, high-investment machinery.

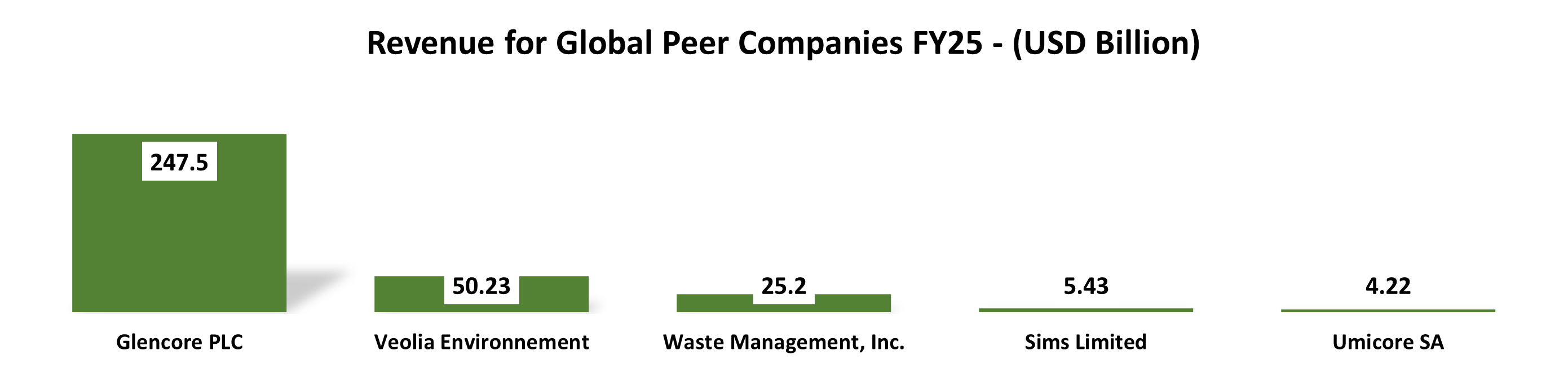

2.5 Major Industry Participants

The competitive landscape is defined by a mix of specialized recyclers and diversified waste management giants. Glencore ($247.5B FY25 revenue) and Umicore ($4.22B FY25 revenue) lead the high-value material recovery segment, specifically focusing on refining precious metals and battery materials.

On the logistical and collection side, firms like Veolia Environnement ($50.23B FY25 revenue) and Waste Management, Inc. ($25.2B FY25 revenue) leverage their vast footprints to handle large-scale municipal and industrial e-waste.

Meanwhile, specialized players like Sims Limited and ERI (Electronic Recyclers International) provide integrated data destruction and recycling services tailored to hardware-heavy corporate sectors.

Source: technavio.com, fortunebusinessinsights.com, Company reports.

3. Indian E-waste management Industry:

3.1 Market Size and Growth

The Indian e-waste management market is experiencing a period of rapid expansion, driven by a massive increase in electronic consumption and shorter product lifecycles.

As of 2025, the market was valued at approximately USD 1.7 to 1.88 billion, and it is projected to grow significantly, reaching over USD 5 billion by 2032. This trajectory is supported by a compound annual growth rate (CAGR) estimated between 6.34% and 7.32% for the upcoming decade.

The growth is heavily influenced by the aggressive digitization of rural and urban areas alike, alongside the implementation of stricter government regulations that aim to move waste from the informal sector into formal recycling channels.

3.2 Key Segments

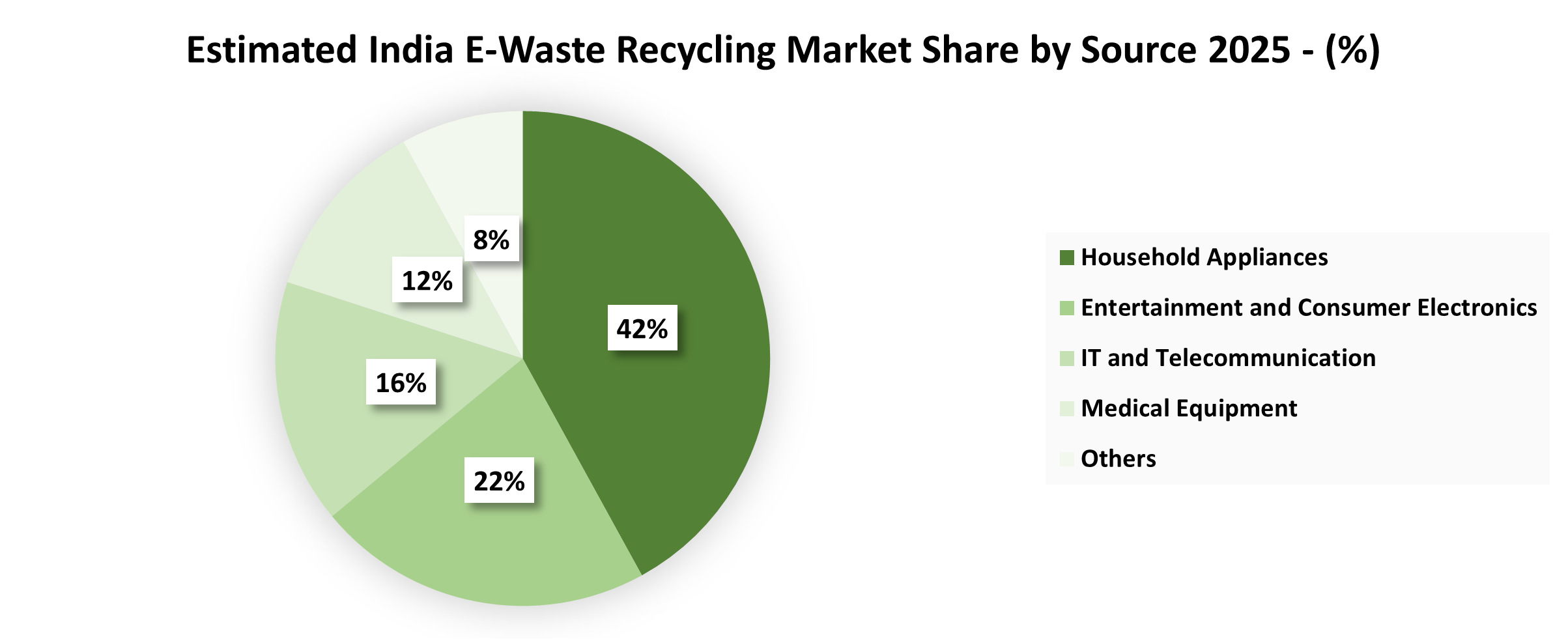

The market is categorized by both the source of the waste and the materials recovered. Household appliances remain the largest source of e-waste, contributing over 40% of the total volume, followed closely by entertainment and consumer electronics.

The IT and telecommunications sector is another significant contributor, especially with the frequent turnover of smartphones and laptops. In terms of material recovery, metals and chemicals form the most valuable segment, accounting for a large portion of the market value due to the high price of recovered precious metals like gold, silver, and copper.

Plastics and glass also represent critical segments, though they face different logistical and processing challenges.

3.3 Regional Highlights

E-waste generation in India is highly concentrated in urban industrial hubs. West India currently holds the largest market share, led by states like Maharashtra and Gujarat, which serve as major processing and collection centers.

Mumbai consistently ranks as the top e-waste-generating city in the country, followed by Delhi, Bengaluru, Chennai, and Kolkata. While the western and southern regions host the most developed recycling infrastructure, North India is expected to see the highest growth rate in the coming years as regional collection networks expand.

Interestingly, although 65 cities generate more than 60% of the nation’s e-waste, rural digital adoption is beginning to shift the geographical spread of discarded electronics.

3.4 Technology Drivers

Advancements in recovery technology are transforming the industry from basic dismantling to sophisticated material science. Leading formal recyclers are adopting automated shredding, optical sorting, and zero-discharge effluent systems to improve recovery rates and environmental safety.

There is an increasing shift toward hydrometallurgical and pyrometallurgical processes for high-purity metal extraction. Furthermore, the rise of “urban mining” has turned e-waste into a strategic resource for reclaiming rare earth elements.

Digital tracking systems and blockchain are also being explored to enhance the transparency of the Extended Producer Responsibility (EPR) certificates, ensuring that waste is traceable from the consumer to the final disposal site.

Source: Astute Analytica, IMARC Group, Company reports.

4. Industry Segmentation:

Note on Data Discrepancy: Please note that there is a difference between the total market values in “India E-waste Management Market Size Chart” and “Estimated India E-Waste Recycling Market Forecast By Material (Total Size) provided earlier. These variations arise because the data is sourced from two different reports which employ distinct research methodologies, definitions of “management” vs. “recycling,” and varied forecasting models.

5. Key Trends/Growth Drivers:

Rapid growth in global electronic consumption

Global e-waste generation exceeded 60 million metric tonnes annually, according to the Global E-waste Statistics Partnership. Rising sales of smartphones, laptops, TVs, and appliances are accelerating waste generation. For example, over 1.2 billion smartphones are shipped globally each year, creating a massive future recycling stream.Shortening product replacement cycles

Consumers are replacing devices more frequently. Smartphones that previously had a lifecycle of 4–5 years are now often replaced within 2–3 years, significantly increasing electronic waste volumes and recycling demand.High value recovery from precious metals

E-waste contains valuable recoverable materials. According to industry estimates, 1 tonne of mobile phones can contain more gold than 1 tonne of gold ore mined traditionally. Companies like Umicore generate significant revenue through precious metal recovery from electronic scrap.Government regulations and Extended Producer Responsibility (EPR)

India implemented E-Waste Management Rules requiring manufacturers to collect and recycle a fixed percentage of products sold. Similar regulations in the European Union are forcing companies to strengthen recycling systems, boosting formal e-waste processing capacity.Growth in formal recycling infrastructure

Companies like Attero process large volumes of lithium-ion batteries and e-waste in India. Attero claims recovery rates of up to 95–98% for certain metals, showing how advanced recycling technologies are improving industry economics.Rising demand for critical minerals and rare earth recovery

E-waste recycling is increasingly important for securing materials used in EVs and electronics, such as lithium, cobalt, and nickel. With EV demand surging globally, battery recycling has become a strategic priority for countries like China and United States.Corporate sustainability and circular economy initiatives

Companies like Apple use recycled rare earth materials and aluminum in products and operate recycling robots like “Daisy” that can dismantle 200 iPhones per hour, highlighting how sustainability goals are driving recycling investments.Increase in lithium-ion battery waste

The rise in EV adoption is expected to create a major battery recycling market. By 2030, millions of EV batteries globally are expected to reach end-of-life, creating significant demand for specialized recycling and material recovery facilities.Digitalization and smart waste tracking systems

Governments and recyclers are increasingly using digital tracking systems to monitor e-waste movement and compliance. For example, India introduced online EPR certificate trading mechanisms to formalize recycling processes and improve transparency.Growing environmental and health awareness

Improper disposal of e-waste releases toxic substances like lead and mercury into soil and water. Organizations such as the World Health Organization have highlighted health risks from informal recycling practices, increasing pressure for environmentally safe disposal systems.

Sources: United Nations Environment Programme; World Health Organization; Global E-waste Statistics Partnership; Central Pollution Control Board; International Telecommunication Union.

6. Industry Risks and Future Challenges:

6.1 Dominance of Informal Recycling Sector:

One of the biggest risks in India’s e-waste industry is the overwhelming dependence on the informal sector.

Informal recyclers account for ~62% of e-waste processing capacity in India

In several states, over 90–95% of e-waste is handled through unorganized scrap channels

India’s formal recycling rate remains only ~10%, significantly below the global average of ~22%

Informal processing methods such as:

Open burning

Acid extraction

Unsafe dismantling

create severe environmental and health risks while reducing feedstock availability for organized recyclers.

6.2 Rapid Increase in E-Waste Generation:

India’s digital economy and rising electronics consumption are accelerating e-waste generation rapidly.

Key growth drivers include:

Smartphone replacement cycles

Consumer electronics demand

EV battery adoption

Renewable energy waste (solar panels, batteries)

India generated nearly 3.8 MMT of e-waste in FY2024, nearly doubling over the past decade.

Additionally:

Global e-waste generation is expected to reach 82 million tonnes by 2030

Recycling growth globally remains much slower than waste generation

This rapid growth creates pressure on collection systems, recycling infrastructure, and compliance mechanisms.

6.3 Weak Collection Infrastructure:

India has inadequate formal collection infrastructure for e-waste.

India currently has only ~2,808 authorized collection centres for its large population

Accessibility gaps encourage consumers to sell devices to informal scrap dealers

Challenges include:

Poor reverse logistics

Low consumer awareness

Limited collection points in Tier-2 and Tier-3 cities

This restricts organized recycling growth.

6.4 Regulatory & Compliance Challenges:

India introduced the E‑Waste Management Rules 2022 to strengthen Extended Producer Responsibility (EPR).

However, challenges remain:

Weak enforcement mechanisms

Fraudulent recycling certificates

Lack of traceability

Low producer compliance

Recent policy changes regarding mandatory recycler payments have also increased compliance costs for electronics manufacturers. Several global electronics firms challenged the policy due to significantly higher recycling expenses.

This creates uncertainty for recyclers and electronics producers.

6.5 Technology & Recycling Efficiency Constraints:

Advanced recycling technologies such as:

Hydrometallurgy

AI-based sorting

Lithium-ion battery recovery

remain underdeveloped in India.

Key issues include:

High technology costs

Low recovery efficiency

Limited domestic processing capability for rare earth metals and lithium

Although India’s annual formal recycling capacity reached ~4.2 MMT in 2024, technological capability remains concentrated among a few large players.

6.6 Low Consumer Awareness & Participation:

Consumer participation in formal recycling channels remains limited.

Challenges include:

Lack of awareness regarding authorized recyclers

Preference for resale in informal markets

Low incentives for responsible disposal

This reduces formal collection rates and weakens circular economy development.

7. Major Players in India:

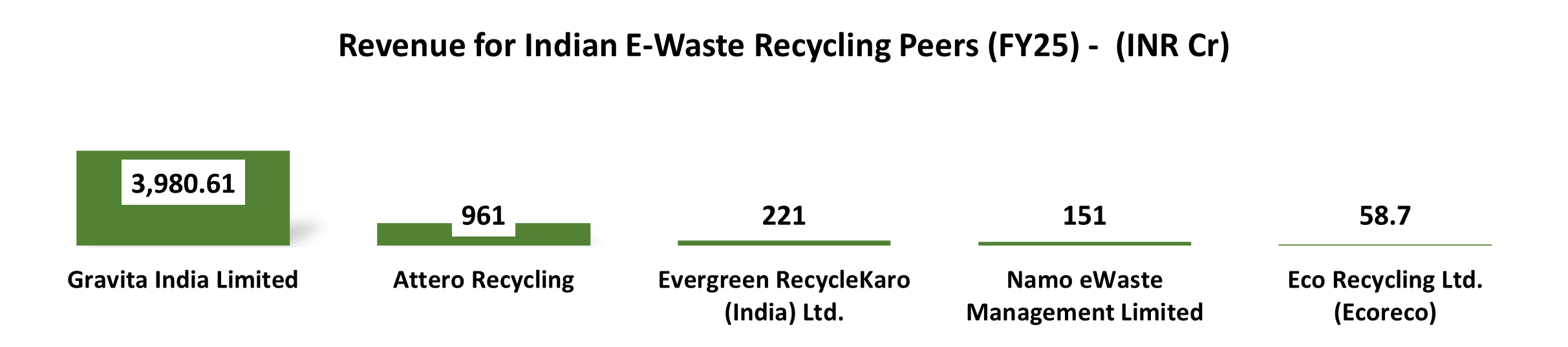

7.1 Gravita India Ltd.:

Gravita India Ltd. is one of India’s leading recycling and resource recovery companies with operations across lead recycling, aluminum recycling, plastic recycling, and e-waste processing. The company operates in more than 70 countries and has developed an integrated recycling ecosystem focused on circular economy solutions. With FY25 revenue of ~₹3,981 crore, Gravita is among the largest organized recycling companies in India. The company is expanding aggressively in lithium-ion battery recycling, electronic scrap recovery, and precious metal extraction, positioning itself to benefit from rising e-waste generation and EV adoption. Gravita also benefits from strong export capabilities and diversified recycling operations.

7.2 Attero Recycling Pvt. Ltd.:

Attero Recycling Pvt. Ltd. is one of India’s largest and most technologically advanced e-waste and lithium-ion battery recycling companies. The company specializes in recovering gold, silver, copper, cobalt, nickel, and lithium from electronic waste and used batteries. With estimated FY25 revenue of ~₹961 crore, Attero has emerged as a major player in India’s circular economy ecosystem. The company operates one of the world’s most advanced urban mining facilities and holds multiple patents in metal extraction technologies. Attero is also expanding into EV battery recycling, which is expected to become a major growth segment over the next decade.

7.3 Evergreen RecycleKaro (India) Ltd.:

Evergreen RecycleKaro (India) Ltd. operates in the recycling and processing of electronic waste, lithium-ion batteries, and industrial scrap materials. The company focuses on environmentally sustainable disposal and recovery solutions for electronic and electrical equipment. With FY25 revenue of ~₹221 crore, the company is gradually expanding its recycling infrastructure and collection network. Evergreen RecycleKaro benefits from rising regulatory focus on formal recycling and increasing awareness regarding safe disposal of electronic waste.

7.4 Namo eWaste Management Ltd.:

Namo eWaste Management Ltd. is an organized e-waste recycling company engaged in the collection, dismantling, refurbishing, and recycling of electronic waste materials. The company provides recycling solutions for computers, servers, telecom equipment, consumer electronics, and industrial electrical waste. With FY25 revenue of ~₹151 crore, Namo eWaste is positioned as a growing player in India’s formal recycling market. The company benefits from increasing Extended Producer Responsibility (EPR) compliance requirements and growing demand for environmentally compliant recycling services.

7.5 Eco Recycling Ltd. (Ecoreco):

Eco Recycling Ltd. is one of India’s oldest organized e-waste recycling companies and a pioneer in formal electronic waste management. The company offers services including asset destruction, e-waste recycling, data destruction, and IT asset disposition (ITAD) solutions. With FY25 revenue of ~₹58.7 crore, Ecoreco operates authorized recycling facilities and serves corporate, government, and institutional clients. The company benefits from increasing corporate focus on secure data destruction, sustainability reporting, and environmental compliance.

8. Conclusion:

The Indian e-waste management industry is emerging as a high-growth segment within the circular economy ecosystem, driven by rapid digitalization, rising electronics consumption, increasing EV adoption, and stricter environmental regulations. As the 3rd largest e-waste generator globally, India presents significant long-term opportunities for organized recycling and resource recovery companies.

India’s e-waste generation is projected to increase from ~6.2 million metric tonnes in 2024 to nearly 14 million metric tonnes by 2030, creating substantial demand for formal recycling infrastructure, metal recovery, battery recycling, and sustainable waste management solutions. Government initiatives such as the E‑Waste Management Rules 2022 and Extended Producer Responsibility (EPR) framework are expected to accelerate industry formalization and improve compliance standards.

However, the industry continues to face major challenges including the dominance of the informal sector, weak collection infrastructure, low consumer awareness, technology limitations, and regulatory enforcement gaps. Additionally, rapidly increasing battery and solar waste will require significant investment in advanced recycling technologies and processing infrastructure.

Leading organized players such as Gravita India Ltd., Attero Recycling Pvt. Ltd., Evergreen RecycleKaro (India) Ltd., Namo eWaste Management Ltd., and Eco Recycling Ltd. are expected to benefit from increasing formalization, higher recycling demand, and rising focus on critical metal recovery and sustainable disposal practices.

Overall, with growing environmental awareness, policy support, and increasing demand for resource recovery, the Indian e-waste management industry is expected to witness strong long-term structural growth, making it an important sector supporting sustainability, urban mining, and circular economy development in India.

THANK YOU FOR READING!!

Hope you liked our work. Please Subscribe so that we can reach out to more People like you!

We are Proud to Announce Our New Launch of the Premium services where we Deep-dive into the Business and back you up with Robust Research.

We Provide services for different Level of Investors. You can Email us directly to start your journey!