Here, at EquityEdge Research, we deep dive into complex Articles and Reports and make it easier for you by presenting everything, RIGHT HERE!!

Please Fill the form Below if you are interested in our Services and would like a Free Sample of our Equity Research Report covering a Small/Micro-cap Company.

What Will We Discuss Today?

Global Defence Electronics Industry Overview.

Indian Defence Electronics Industry Overview.

Export & Import Dynamics.

Industry Segmentation.

Key Trends/ Growth Drivers.

Risks & Challenges.

Major Players in India.

Conclusion/Outlook.

1. Global Pharmaceutical Industry Overview:

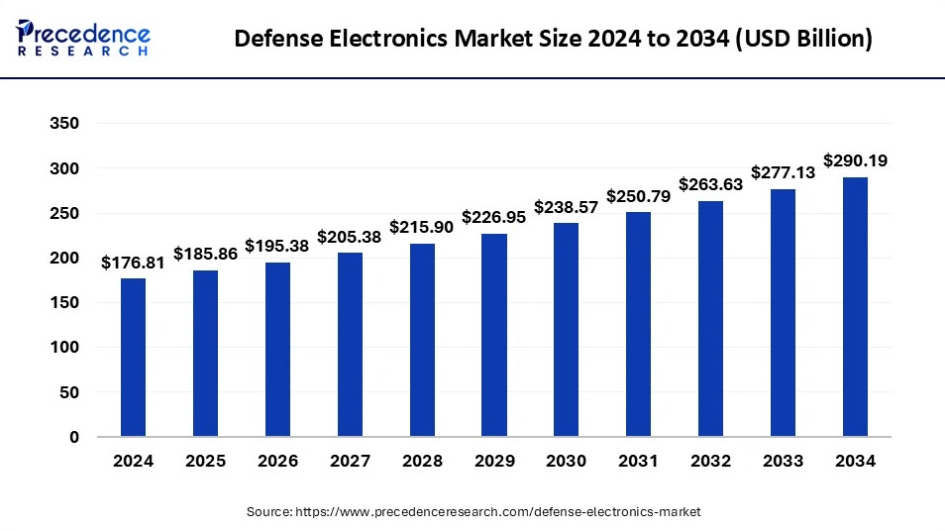

The global defense electronics market is large and growing rapidly. In 2024, estimates place its value between $175–230 billion. Forecasts suggest an annual growth rate of around 5–6%, which would bring the market to $250–300 billion by the early 2030s. A specific projection puts it at approximately $290.2 billion by 2034, up from $176.8 billion in 2024, indicating a ~5.1% CAGR.

This growth is driven by increasing defense budgets, rapid digitization across military forces, and the demand for advanced technologies such as IoT, AI, next-gen sensors, and communications equipment. For 2025, one analysis expects the market to hit around $185.9 billion. Another forecast suggests the market could reach $305 billion by 2029.

1.1 Major Regional Markets & Leading Countries

Asia-Pacific: This region currently dominates the market. Over half the world’s population and many rapid-developing militaries are in Asia . China’s steady defense-spending increases and tech investments make it a top market, while India’s expanding budgets and “Make in India” initiatives are also driving demand. Japan and South Korea likewise invest heavily in advanced electronics. As a result, Asia-Pacific held the largest regional share of defense electronics in 2024.

North America: The United States is the single largest national market. U.S. defense spending is at record highs (FY2025 DoD request ~$849.8 B), much of which flows into electronics (air defense radars, communications, UAVs, etc.). North America leads in electronic warfare and sensor systems; one report notes North America led the EW segment in 2024. Canada’s growing defense programs and close industry ties to the U.S. also boost the North American market.

Europe & CIS: Key NATO countries (UK, France, Germany, Italy, etc.) maintain advanced defense electronics industries. Europe as a whole is a major but slower-growing market. For example, French firm Safran is expanding globally (announced its first overseas defense-electronics site in India in 2024). Israel (Elbit, Rafael) is a leader in EW and UAVs. Russia remains a significant market (especially for domestic firms) but faces export controls and sanctions. Other significant spenders include Turkey (Aselsan), Eastern European buyers (NATO upgrades), and a rising interest from Gulf states in sensors and networks.

Leading Countries: The top defense spenders – notably the U.S., China, India, Russia, Japan, and major European powers – lead in defense electronics procurement. For instance, ongoing programs in the U.S., China, and India for new fighters, ships and missile defenses all require cutting-edge electronics. Sweden, South Korea, and others also make key contributions through domestic firms (e.g. Saab, Samsung/Hanwha).

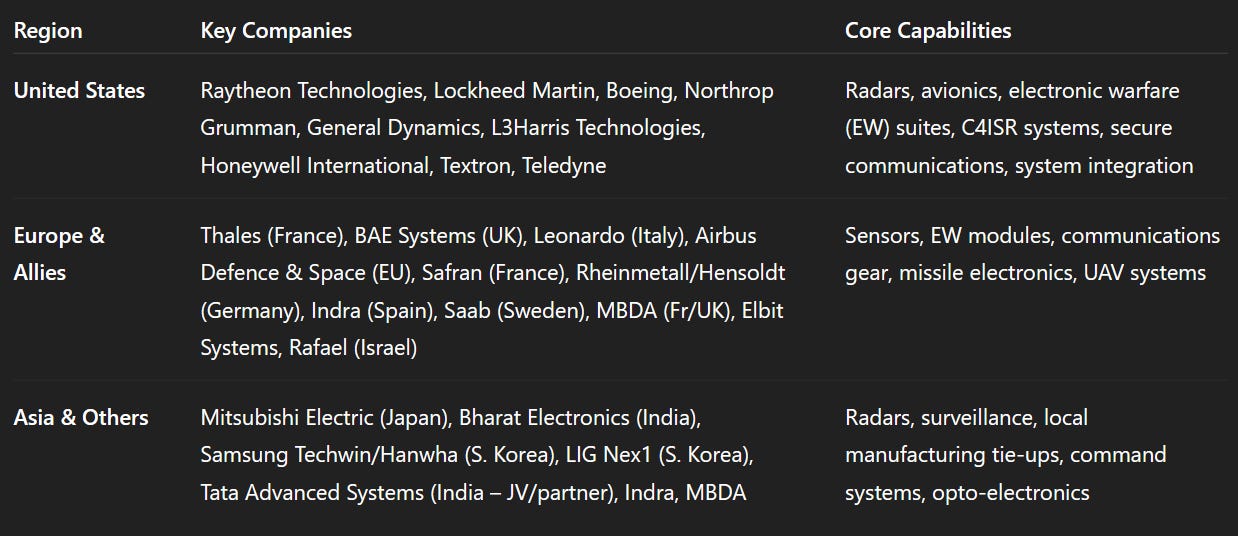

1.2 Prominent Companies & Contractors:

1.3 Key Technologies & Innovations:

Defense electronics encompass a broad range of high-tech systems. Recent innovations include:

Advanced Radars and Sensors: Active Electronically Scanned Array (AESA) radars and next-generation sensor suites (electro-optical/infrared imaging, signal intelligence) are central. Use of gallium nitride (GaN) devices and miniaturized multi-function antennas is growing. For example, both military and naval radars are moving to GaN for higher power and efficiency.

Electronic Warfare (EW): Modern EW systems (jammers, anti-jam receivers, signals intelligence) are rapidly evolving. The EW electronics market alone was about $18.5 B in 2024 and is projected to reach $34.1 B by 2031 (≈9.4% CAGR). Notably, “cognitive” EW using AI/ML to autonomously detect and counter threats is emerging.

C4ISR & Communications: Secure, high-bandwidth communication and networking equipment (satellite links, software-defined radios, data links, and integrated command-control systems) are vital. Efforts to harden links against jamming/spoofing and to implement anti-tamper security (e.g. quantum encryption R&D) are underway. Battlefield Internet-of-Things and satellite communications (military-5G convergence) are key trends.

Artificial Intelligence & Autonomy: AI and machine learning are being embedded throughout defense electronics. Applications include autonomous UAV/drone swarms, predictive maintenance, real-time sensor fusion, and automated decision aids. Recent reports highlight deployment of AI-enabled drones for autonomous target tracking and AI that enhances network resilience against jamming. The industry is increasingly developing edge-compute platforms and rugged processors to run these AI workloads in the field.

Cybersecurity: Electronic systems now integrate advanced cybersecurity features by design (encrypted communications, secure boot, intrusion detection). Defense agencies are adopting stricter standards to secure everything from radars to vehicles. At the same time, cyber defense is driving dual-use demand – military systems often require the same high-level cybersecurity hardening found in critical infrastructure.

Miniaturization & Integration: There is a constant push to reduce size/weight/power (SWaP) of components. This enables more electronics on smaller platforms (e.g. miniaturized radars on UAVs or satellites). Integration of multiple functions (e.g. combined radar-communications apertures) and use of commercial semiconductor advances (3D packaging, advanced FPGAs, etc.) are notable trends.

1.4 Dual-Use Technologies & Civilian Applications:

Many defense electronics technologies have civilian counterparts or applications:

Navigation and GPS: The U.S. GPS system is a classic example. Once restricted to the military, GPS was opened to civilian use (policy changes through the 1980s–2000s). Today GPS underpins navigation in cars, phones, aviation, and countless consumer/industrial devices, demonstrating how military navigation tech spurred a global civilian industry.

Satcom & Comms: Military satellite and secure radio technologies have civilian spin-offs (e.g. satellite broadband, aeronautical/automotive connectivity). Conversely, commercial 5G and software-defined radio tech are being adapted for military use in advanced radios and networks.

Imaging & Sensors: High-end sensors developed for defense (night-vision, infrared cameras, LIDAR, radar altimeters) find civilian uses in aerospace, automotive (e.g. collision-avoidance radar, driver-assist cameras), and law enforcement. Advances in signal processing (originally for EW or SIGINT) also benefit commercial wireless (e.g. spectrum monitoring, antenna technology).

Autonomous Platforms: UAV/drone technology is another area of overlap. Techniques for guidance, stabilization and remote piloting used in military drones are also applied in civilian drones (for agriculture, delivery, mapping). Likewise, CMOS camera and sensor chip improvements flow both ways.

Electronics and Computing: Defense’s need for rugged, reliable electronics drives industry innovations (e.g. rad-hard chips). At the same time, commercial semiconductor R&D (high-speed processors, GPUs, machine learning accelerators) often transfers into defense. For example, chip advances like GaN transistors are used in both 5G telecom equipment and military radar.

1.5 Major Drivers & Challenges:

Drivers (Growth Factors):

Geopolitical tensions and conflicts are the primary growth engine. SIPRI reports ~59 countries involved in wars (2022 vs 2019) and global military expenditure >$2.4 trillion in 2023. This intense security environment drives procurement of advanced electronics.

Additionally, adversaries increasingly rely on digital/AI systems, so militaries invest to maintain technological edge. Rising cyber threats push investment in cyber-resilient electronics. Large defense budgets (e.g. US FY2025 DoD ~$850 B) provide capital for major contracts. Likewise, modernization programs worldwide – upgrading aging fleets with new radars, sensors, C4ISR – directly increase demand.

Challenges:

High R&D and unit costs are a barrier, especially for cutting-edge components or for smaller nations. Stringent export controls (ITAR, Wassenaar, etc.) and shifting trade policies can limit international sales and collaboration (for example, Western restrictions on selling advanced chips or software to certain countries).

Complex compliance means long delays and added costs. Supply chain disruptions – notably shortages of specialized semiconductors and long lead times – are a serious concern. Defense electronics often rely on a few suppliers; global events (pandemics, trade disputes) can interrupt production.

Experts warn that the lengthy distances and geopolitical risks in the global electronics supply make domestic sourcing a strategic imperative. Finally, budget constraints and political shifts (e.g. competing social priorities or budget caps in some countries) can slow programs. The need for interoperability also poses difficulty; integrating new systems onto legacy platforms can be costly and time-consuming.

Source(all) :GM Insights, The Business Research Company, Precedence Research, Military Embedded Systems, TechSci Research, Deloitte, OD Impact, GlobalData, and Teledyne Technologies.

2. Indian Defence Electronics Industry Overview

2.1. Market Overview: Scaling New Frontiers:

India's defence industry is undergoing a structural transformation, with sustained government support, rising private participation, and a strong push for technological self-reliance. Defence electronics—one of the most strategic segments—is emerging as a high-growth vertical within this ecosystem.

Industry Size & Growth Trajectory

The Indian defence market was valued at USD 17.3 billion in 2024, and is expected to reach USD 29.8 billion by 2033, growing at a CAGR of 5.6% (2025–33).

Within this, the broader defence sector is projected to expand at a faster CAGR of 14% between FY24 and FY30, reflecting robust momentum across platforms, electronics, and systems integration.

Record-Breaking Domestic Production

In FY 2023–24, India achieved record defence production worth ₹1.27 lakh crore (~USD 15.34 billion).

This marks a 16.7% YoY increase, and an impressive 174% growth over FY15, driven by increasing indigenous capability and rising exports.

India's Global Defence Trade Status

Despite this growth, India remains the second-largest arms importer globally, with an 8.3% share in total global imports (2020–24).

However, this dependency is steadily reducing, thanks to initiatives like Make in India, Positive Indigenisation Lists, and expanded export outreach.

Sources: IMARC Group, PIB, TOI, The New Indian Express

2.2. Key Market Segments:

3. Import/Export Dynamics

India’s defence trade landscape is undergoing a pivotal transformation. While the country remains one of the world’s largest arms importers, a sharp rise in defence exports—coupled with aggressive indigenisation efforts—is steadily recalibrating the trade balance and strengthening strategic autonomy.

3.1. Export Performance: Scaling New Heights

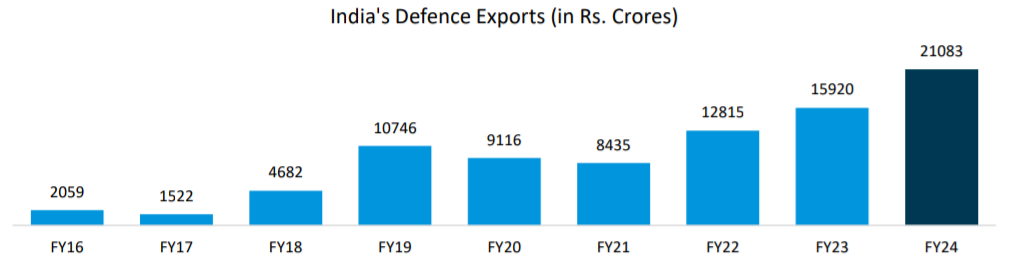

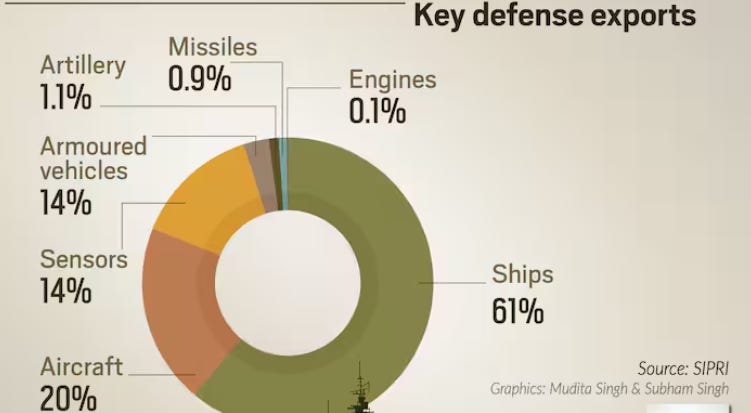

Record-Breaking FY25 Exports: India’s defence exports soared to an all-time high of ₹23,622 crore (~USD 2.76 billion) in FY 2024–25—marking a 12.04% year-on-year increase, and a staggering 34-fold surge from just ₹686 crore in FY 2013–14.

Key Export Contributors:

Private Sector: Contributed ₹15,233 crore (64.5% of total exports), highlighting the growing role of private players in India’s military-industrial complex.

Defence PSUs: Exported ₹8,389 crore (35.5%), with a strong 42.85% YoY growth, reflecting improved global competitiveness.

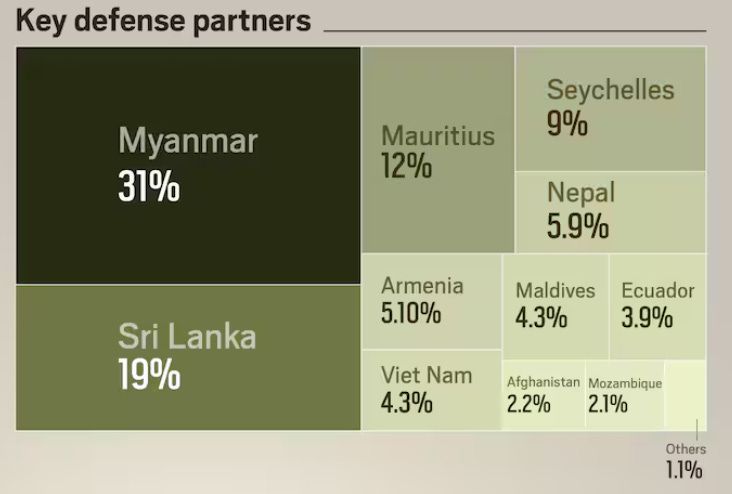

Export Reach: India now exports defence equipment to over 100 countries, signalling its emergence as a credible supplier in the global arms market.

Future Targets: The government aims to scale exports to ₹50,000 crore (~USD 6 billion) by 2028–29, driven by policy support, strategic diplomacy, and production-linked incentives.

Source: India Today Group

3.2. Import Patterns: Still Heavy, But Slowing

India’s Import Status: Despite progress, India remains the second-largest arms importer globally with an 8.3% share in total imports (2020–24). However, imports declined 9.3% compared to the 2015–19 period, thanks to rising domestic capabilities and procurement from indigenous sources.

Shifting Supplier Dynamics

Russia: Still India’s top supplier (36% share), but on a steep decline from 55% in 2015–19 and 72% in 2010–14, reflecting diversification and geopolitical shifts.

France: Emerged as the second-largest supplier, with a 489% surge in exports to India—led by Rafale fighter deliveries and future naval deals.

United States: A deepening partner, supplying key platforms like MQ-9B Sea Guardian drones, transport aircraft, and sensor systems.

Israel: Continues to be a critical provider of missile systems, radars, and electronic warfare equipment.

Major Systems Imported include:

Rafale-M fighter jets (France)

MQ-9B drones (USA)

Advanced radar systems

Submarines and EW platforms

3.3. Trade Balance: A Narrowing Deficit:

Though India still runs a sizeable defence trade deficit, the gap is gradually narrowing. Exports have risen 34x over the past decade, while imports have moderated by over 9%, suggesting that self-reliance is gaining real traction.

Strategic initiatives like Make in India, import restriction lists, iDEX, and the Defence Production and Export Promotion Policy (DPEPP) are key drivers. With consistent policy push and industry momentum, India is on track to achieve a more balanced and resilient defence trade position by 2030.

PIB, Business Standard, The New Indian Express, Economic Times and India Briefing

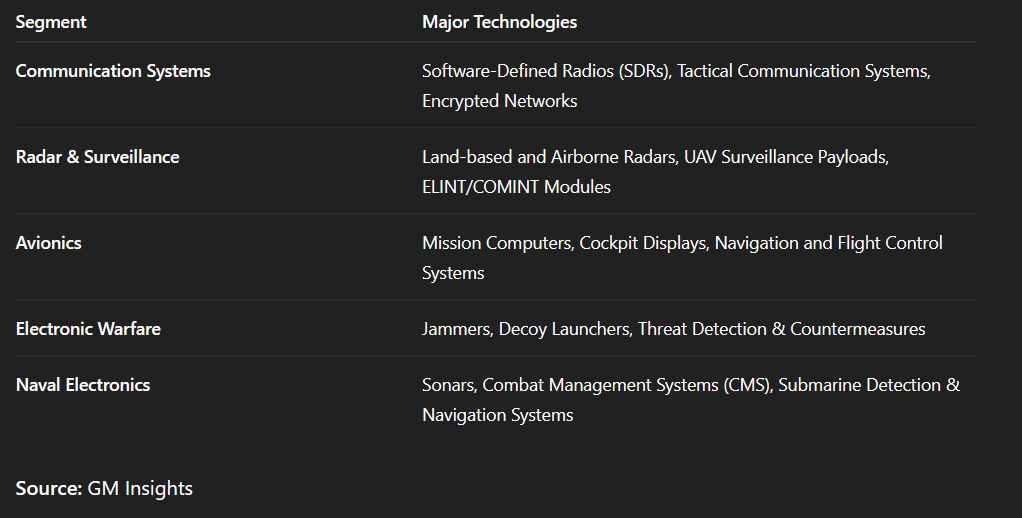

4. Industry Segmentation

4.1. By Application:

Electronic Warfare (EW): Includes jammers, electronic countermeasures (ECM), electronic support measures (ESM), anti-jam receivers, and signal intelligence systems.

C4ISR: Covers systems related to Command, Control, Communications, Computers, Intelligence, Surveillance, and Reconnaissance. These form the backbone of modern network-centric warfare.

Surveillance & Reconnaissance: Involves ground-based radars, airborne sensors (EO/IR), space-based surveillance, and maritime detection systems.

Navigation & Guidance: Involves inertial navigation systems (INS), GPS/GNSS modules, and electronics for guided munitions and missiles.

Fire Control & Weapon Electronics: Targeting and aiming systems, smart fuses, radar-guided artillery electronics, and ballistic computers.

Cybersecurity Systems: Embedded electronics for secure communications, intrusion detection, and encryption across devices and networks.

Simulation & Training: Includes radar/emission simulators, VR/AR-based electronic combat training platforms, and mission rehearsal systems.

4.2. By Product Type:

Radars & Sensors: AESA radars, infrared (IR) sensors, LiDAR systems, and GaN-based modules for high-performance radar applications.

Avionics Systems: Flight computers, mission systems, cockpit displays, HUDs, and navigation electronics used in military aircraft.

Communication Systems: Tactical radios, satellite communication (SATCOM) terminals, software-defined radios (SDRs), and secure data links.

Electronic Countermeasures (ECM): Airborne or ground-based systems to jam enemy radars and communications.

Power & Display Systems: Ruggedized displays, power converters, battery management units, and control interfaces for military platforms.

Embedded Electronics & Chips: Specialized processors, FPGAs, ASICs, and AI accelerators for rugged battlefield use.

4.3. By Platform:

Airborne: Electronics installed on fighter aircraft, UAVs, AEW&C platforms, and military helicopters.

Naval: Systems used in warships, submarines, UAV launchers, and naval radars or sensors.

Land: Electronics for armored vehicles, battlefield surveillance systems, and tactical command centers.

Space: Includes defense satellites (for ISR, communications, or GPS), ground-control electronics, and launch system payloads.

4.4. By End User:

Army: Ground-focused systems like artillery radar, battlefield communications, and vehicle-mounted EW.

Navy: Naval radar, sonar electronics, electronic countermeasures on ships, and underwater surveillance systems.

Air Force: Avionics, electronic warfare pods, airborne radar systems, and autonomous UAV control systems.

Joint/Strategic Commands: Integrated systems used across branches – e.g., C4ISR networks, missile defense systems, and space-based defense infrastructure.

5. Key Trends & Growth Drivers

India’s defence electronics ecosystem is riding a wave of innovation, propelled by cutting-edge technologies, startup participation, and government reforms aimed at self-reliance.

5.1. AI Integration in Defence Operations:

The Ministry of Defence launched 75 AI-based defence solutions in July 2022, spanning areas such as logistics, data analytics, battlefield surveillance, and weapons systems. These developments have started to redefine the capabilities of platforms like fighter jets, where AI-enabled avionics and software-centric upgrades now serve as strategic differentiators.

5.2 Rise of Autonomous and Unmanned Systems:

India is accelerating development of autonomous systems for real-time intelligence and battlefield surveillance. The Indian Army has inducted 75 AI-powered drones, and the indigenous Drishti-10 MALE UAVs reflect growing ISR capabilities. The procurement of American MQ-9B Sea Guardians signals India's intent to blend indigenous development with best-in-class foreign systems.

5.3 Transition to Software-Defined Technologies:

A major shift is underway from rigid, hardware-dominated systems to flexible, software-defined architectures. These systems allow for modular upgrades, AI integration, and real-time battlefield data processing, placing India in sync with global defence modernization trends centered on speed, adaptability, and information dominance.

5.4 Atmanirbhar Bharat & Local Procurement Push:

India’s self-reliance mission has significantly restructured defence procurement. In FY24, 75% of the capital acquisition budget was earmarked for Indian vendors—up from 63% in FY22. This consistent rise in local sourcing highlights the government’s clear policy direction towards strengthening the domestic defence industrial base.

5.5 Production-Linked Incentive (PLI) Scheme for Components:

In March 2025, the government rolled out a ₹22,919 crore PLI scheme focused on passive electronic components such as resistors, inductors, and capacitors. The scheme is projected to bring in ₹59,350 crore in new investments and generate production worth ₹4.56 lakh crore over six years, directly benefiting the defence electronics supply chain.

5.6 Positive Indigenisation Lists and SRIJAN:

To curb dependency on imports, India has now banned over 5,600 defence items from being sourced abroad. Under the SRIJAN initiative, more than 14,000 components have already been indigenised, while 3,000 items feature on the Positive Indigenisation Lists. These policies are compelling both public and private players to scale local manufacturing and design capabilities.

5.7 iDEX: Catalysing Defence Innovation:

Since its launch in 2018, the iDEX (Innovations for Defence Excellence) initiative has become a cornerstone of India’s military innovation ecosystem. As of February 2025, it has attracted 619 startups and MSMEs, addressed 549 defence challenges, and led to 430 contracts. With a ₹449.62 crore allocation for FY26 and new focus areas like quantum technologies and semiconductors through the ADITI scheme, iDEX continues to foster next-generation defence technologies.

Sources: Defence Production Dashboard (DDOP), Strafasia, IDI, Business Standard, ModernIntelligence, PIB

6. Key Risks & Challenges

6.1 Persistent Technology Gaps & Import Dependence:

Despite progress, India still relies on imports for 60–70% of advanced components, including AESA radars, jet engines, and semiconductors—all critical for building next-gen platforms. This dependence continues to undermine India’s vision of true defence self-reliance.

6.2 Cumbersome Procurement and Execution Bottlenecks:

Big-ticket projects like the Tejas fighter and Rafale MMRCA deals face long delays due to slow procurement cycles and bureaucratic decision-making. While reforms exist, on-ground execution remains patchy, impacting force readiness and technology absorption.

6.3 Underwhelming R&D Investment:

India invests just 0.7% of GDP in R&D, with DRDO receiving only 3.9% of the defence budget. In contrast, countries like the US (3.5%) and China (2.4%) prioritize defence R&D, leading to superior innovation pipelines and indigenous tech development.

6.4 Limited Private Sector Participation:

The private sector contributes only 21% to total defence production, hindered by high entry barriers, lack of access to critical IP, and uncertain policy continuity. This stifles innovation and keeps India’s defence electronics ecosystem from scaling effectively.

6.5 Modernisation Delays & Obsolete Platforms:

Legacy platforms like MiG-21s remain in service, reflecting sluggish modernisation. Only 27% of the FY26 defence budget is allocated for capital acquisition, slowing the transition to network-centric warfare. The absence of integrated theatre commands further hampers tech-enabled joint operations.

7. Major Indian Players:

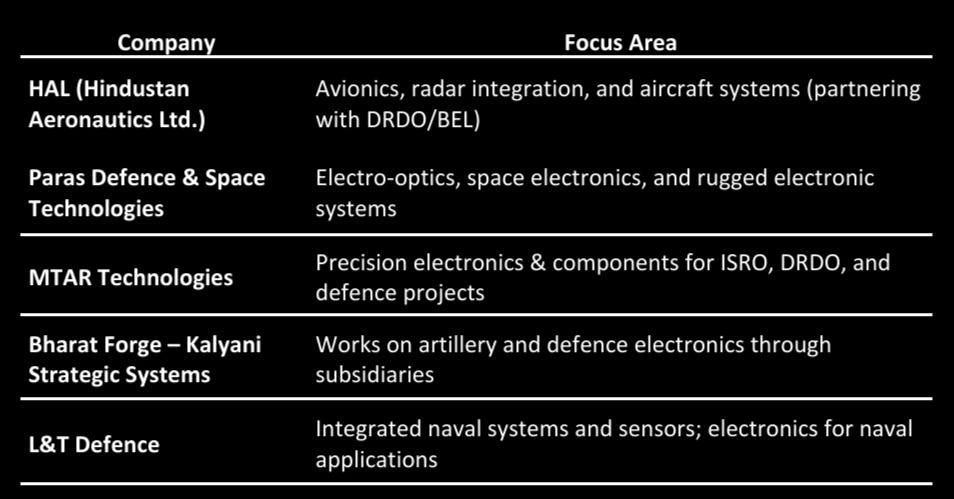

7.1. Bharat Electronics Limited (BEL)

Bharat Electronics Limited is the largest defence electronics company in India and a leading Public Sector Undertaking under the Ministry of Defence. Established in 1954, BEL has played a central role in India’s indigenous defence capability, particularly in the design and manufacturing of advanced electronic products and systems. Its extensive portfolio includes radars, electronic warfare systems, military communication systems, night vision devices, naval and airborne avionics, missile electronics, sonar systems, and more. BEL is known for its strong R&D foundation and collaboration with the Defence Research and Development Organisation (DRDO), as well as for fulfilling major orders for the Indian Armed Forces. It has also expanded its footprint globally by exporting defence electronics to over 40 countries.

7.2. Hindustan Aeronautics Limited (HAL)

Hindustan Aeronautics Limited (HAL) is a state-owned aerospace and defence company headquartered in Bengaluru, operating under the Ministry of Defence, Government of India. Established in 1940, HAL is one of Asia's largest aerospace firms and plays a critical role in the design, development, manufacturing, and maintenance of aircraft, helicopters, avionics, and aero engines. The company is known for its indigenous platforms such as the Light Combat Aircraft (Tejas), Dhruv Advanced Light Helicopter, and Light Combat Helicopter (LCH), and also handles licensed production of major aircraft like the Sukhoi Su-30 MKI. HAL’s Electronics Division develops mission-critical avionics and systems integration for various military platforms, making it a vital player in India’s defence electronics ecosystem.

7.3. Data Patterns (India) Ltd.

Data Patterns is a high-end defence and aerospace electronics company based in Chennai, and one of the few private firms in India offering vertically integrated capabilities from design through to production. The company focuses on mission-critical electronics systems and subsystems for defence applications, including radar signal processing, electronic warfare, communication systems, avionics, and fire control systems. Known for its strong in-house R&D capabilities, Data Patterns supplies products to DRDO, BEL, HAL, BrahMos, ISRO, and several foreign OEMs. Its systems are deployed across land, sea, air, and space platforms. The company has gained prominence as a key private-sector contributor to the Atmanirbhar Bharat defence initiatives.

7.4. Astra Microwave Products Ltd.

Astra Microwave Products, based in Hyderabad, is a specialist in RF and microwave-based systems, components, and subsystems. The company’s offerings are crucial for radar, electronic warfare, satellite communication, and missile applications. Astra designs and manufactures components such as power amplifiers, radar front-ends, signal generators, T/R modules, and antenna systems, making it a key supplier for DRDO labs and other government and private entities like BEL and ISRO. Astra Microwave’s expertise in high-frequency systems has enabled it to participate in a wide range of indigenous defence programs, including radar and missile development projects.

7.5. Tata Advanced Systems Limited (TASL)

Tata Advanced Systems is the defence and aerospace arm of the Tata Group and represents one of the most diversified private-sector players in the industry. TASL is involved in a broad range of defence electronics activities, including sensors, avionics, communications, UAV electronics, and system integration. The company collaborates with global defence majors such as Lockheed Martin, Boeing, and Airbus, bringing global-grade technology and quality standards into Indian production. TASL contributes to several key Indian defence programs, including airborne surveillance systems, missile systems, and radar subsystems, and plays a key role in integrating electronic payloads for platforms ranging from drones to missiles.

8. Future Trends & 2030 Outlook:

Steady Growth to 2030: Analysts expect the market to continue expanding at roughly 5–6% per year through 2030. For example, one forecast projects ~USD 182.6 B in 2024 growing to ~USD 240.8 B by 2030 (CAGR ~4.8%) Another projects ~$290–305 B by the early 2030s. Continued military spending (e.g. recent US and allied budget hikes) underpin this.

Artificial Intelligence & Autonomy: AI/ML will become even more integral. By 2030, expect autonomous unmanned systems (drone swarms, robotic ground and naval vehicles) to be common on the battlefield, with onboard AI for tasks like real-time target recognition and adaptive mission planning. AI-driven cyber-defense (real-time threat detection) and cognitive EW systems (self-learning jammers) will grow.

C4ISR and Networks: The move to joint, network-centric operations will intensify. Technologies like 5G/6G military networks, edge computing nodes, and resilient mesh communications will be fielded. Satellite constellations (LEO/HEO) for surveillance and communications will provide global connectivity for defense.

Electronic Warfare and Spectrum Control: With increasingly contested electromagnetic domains, EW and cyber-electronic warfare capabilities will be a focus. Expect advances in quantum sensing and low-probability-of-intercept radars. Militaries will also invest in counter-satellite (ASAT) and anti-drone electronic systems.

Next-Gen Hardware: Look for new platforms to adopt emerging hardware: e.g. photonic RF components, neuromorphic processors, and even nascent quantum communication links for ultimate secure comms. Continued miniaturization will allow embedding powerful electronics in missiles, munitions, and soldier gear. Hypersonic vehicles (boost-glide missiles) will drive development of extreme-condition electronics.

Resilience and Cyber: Given the cyber threat landscape, future systems will prioritize resilience. Hardened, redundant architectures (including blockchain-like supply tracking) and robust encryption will be standard. Governments may enforce domestic sourcing for key components (e.g. secure chips) to mitigate supply risks.

Regional Shifts: Asia-Pacific will likely increase its share of the market, as China’s and other Asian countries’ modernization accelerate. Collaborative programs (e.g. among NATO or AUKUS partners) and alliances may shape large procurement projects. “Make in” initiatives (India, SE Asia) suggest more local production of defense electronics by 2030.3

THANKYOU FOR READING!!

Hope you liked our work, Please Subscribe so that we can reach out to more People like you!

We are Proud to Announce Our New Launch of the Premium services where we Deep-dive into the Business and back you up with Robust Research.

We Provide services for different Level of Investors. You can Email us directly to start your journey!

If you like the hard work we put in, you can invest in us:

For our Non-Indian audience: You can donate to us through PayPal. Click here.

For our Indian audience, UPI QRs are given below:

Great article.. v insightful.

Wrote something purely on BEL, India defence electronics has an interesting journey ahead no doubt.

https://open.substack.com/pub/earningsunwrapped/p/firing-on-all-fronts-indias-defence?utm_source=share&utm_medium=android&r=rer2b