1. Fundamentals of a Data Centre

1.1 What is a Data Centre?

A data centre is a physical facility used to house critical applications and data. It consists of networked computing and storage resources like routers, switches, firewalls, storage systems, servers, and application-delivery controllers.

Modern data centres have evolved from on-premises servers to multi-cloud environments, enabling connectivity across multiple locations, including the edge, private, and public clouds. Cloud-hosted applications rely on data centre resources from cloud providers.

1.2 Who uses Data Centres?

Data centres support industries like cloud computing, AI, finance, telecommunications, e-commerce, and digital content. They provide computational power for businesses and governments to operate efficiently.

1.3 Who owns and operates data centres?

Ownership varies based on business models and investment strategies, including:

Cloud service providers (AWS, Google Cloud, Azure).

Telecom companies (Reliance Jio, Airtel).

Hyperscale operators (Meta, Microsoft).

Colocation providers (Equinix, Digital Realty).

Financial institutions & Real Estate Investors.

1.4 Primary Uses of a Data Centre

Data Storage & Management

Securely stores and manages structured & unstructured data.

Ensures quick retrieval, backup, and recovery.

Example: Cloud storage (Google Drive, AWS S3) & enterprise databases.

Computing Power & Processing

Provides high-performance computing for AI, big data, and simulations.

Scalable computing on demand.

Example: AI model training & machine learning workloads.

Application Hosting & IT Services

Hosts business-critical applications (ERP, CRM, SaaS platforms).

Ensures low latency, security, and 24/7 availability.

Example: Cloud-based apps (Salesforce, Zoom, Shopify).

Security & Compliance Management

Implements cybersecurity protocols, encryption, and access control.

Ensures compliance with GDPR, HIPAA, and data localisation laws.

Example: Government and financial organisations use data centres for secure operations.

2. What’s Happening Around the Globe?

Data Centers & AI: Powering the Future

AI-driven growth is expected to push the global data centre market to 10-20% annual growth over the next decade.

Data center GPU servers consume 3-4x more power than traditional CPU servers, leading to an annual demand surge of 30-40% in key regions.

Constraints in power supply, labour, and materials may slow down expansion in some markets.

Data center rents are rising due to high demand and limited supply, benefiting incumbents.

Electricity Demand Surge from AI & Data Centers

Electricity demand in US & Europe has remained flat for 20 years but is expected to grow at 2-3% annually, driven by data centres.

Data centres could contribute ~20% of incremental electricity demand globally.

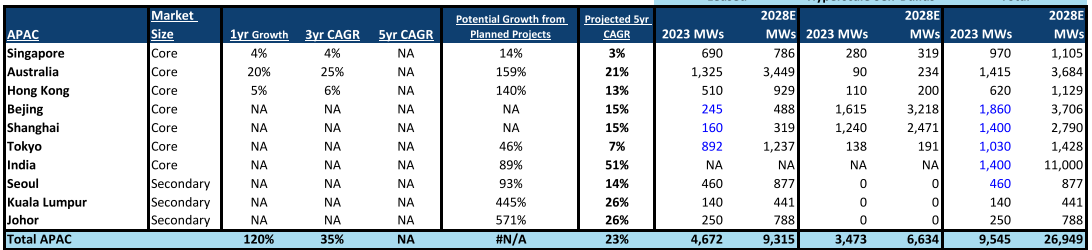

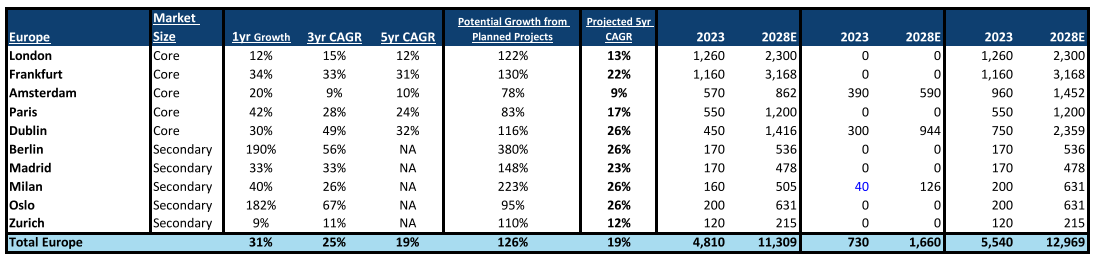

Europe’s fastest-growing data centre markets: Germany, Ireland, Spain, and Norway.

US markets are expanding beyond Northern Virginia to non-traditional regions like the Southeast.

Growth will benefit power plants, renewable developers, and grid utilities.

Global Data Center Market Analysis

Colocation data centre demand has grown 10-20% annually for 15+ years, but in the last two years, demand surged beyond 30%.

Vacancy rates have dropped from 10% to just 1-3%, highlighting supply shortages.

Major constraints: Power availability, land, labour, and construction materials.

Power demand context:

10 years ago: 15% of data center growth required 250 MW in the US.

Today: The same 15% growth requires 2 GW, with actual growth doubling that.

Trailing 4-quarter leasing volume:

US: ~4.5 GW

Europe: ~1 GW

Rising rents: Since late 2021, wholesale data centre rents (e.g., DLR) have surged 80%, reversing the 2013-2020 decline.

Even if growth moderates to 10-20%, many new GWs of power will be required annually.

Future Market Outlook

Data Center Growth Projections by Region

Data Center Growth by Market

Growth will continue, but expansion will shift to markets with available power capacity.

Long-term power demand growth is inevitable as AI and cloud services scale.

Market modelling suggests 10-15% CAGR in power usage, requiring continuous investment in energy infrastructure and grid capacity.

3. Introduction to Indian DATA CENTRE Industry

Current Market Snapshot

India’s colocation (colo) DC capacity in 2024: 1.35 GW (up 38% YoY).

Estimated requirement by 2030: 5 GW (to reach 50% of China’s density).

Planned & under-construction capacity by 2028: 3.3 GW, making the 5 GW target realistic

India’s Competitive Advantage in the DC Market

Lower Cost Per MW: Capex per MW in India is INR 465 million (~USD 5.5 million/MW), significantly lower than developed markets.

Strategic Location: Positioned between the Middle East & Southeast Asia, India can serve as a regional data hub.

Improving Connectivity: Increased subsea cable landings enhance global data flow and attract foreign investments.

Cost-Effective Operations: Lower power, real estate, and manpower costs compared to the West.

AI's Role in India's DC Growth: DeepSeek AI & IndiaAI Mission: A Game Changer

DeepSeek’s AI models are more power-efficient than traditional AI workloads.

IndiaAI Mission plans to procure 18,000+ compute chips (like NVIDIA H200), accelerating AI-driven DC demand.

Lower rack density (6-12KW/rack) in Indian DCs can be repurposed for AI workloads, making existing and new capacity AI-ready.

4. Regulatory Push & Market Evolution

The Reserve Bank of India (RBI) data localisation mandate was a key turning point for India’s data centre (DC) market. This policy, which required payment-related data to be stored within India, laid the foundation for accelerated investments in the sector.

The turning point came in 2021 when a temporary ban on HDFC-Mastercard’s new card issuance due to data centre outages highlighted the critical need for robust data infrastructure. Since then, India’s DC capacity has been growing at a staggering 50%+ CAGR, with its share of global demand expected to rise from <1% to ~6% by 2030.

5. Key Players

Players With Sizeable Online Capacities And Established Presence In The Market

Netmagic (part of NTT): NTT's business in India is growing at 40% CAGR over the last 3 years.

Nxtra by Airtel: Will invest INR 50 Bn to build 6 new hyperscale DCs and expand its capacity by 2x to 400+ MW.

ST Telemedia Global Data Centres: Intends to increase the share of renewable energy to 70%. Have invested in renewable plants owned by Q2 Power and Avaada.

CtrlS: To invest US$ 2 Bn over the next 6 years to expand into Asia and Middle East, intending to add 350 MW of AI and cloud-ready DCs.

Sify: Kotak DC Fund invested INR 16,000 Mn in Sify Infinit Spaces (Sify's DC arm) to expand DC capacity.

Yotta: Partnered with Vi Business (Vodafone Idea's enterprise arm) to enhance the data center and cloud services portfolio.

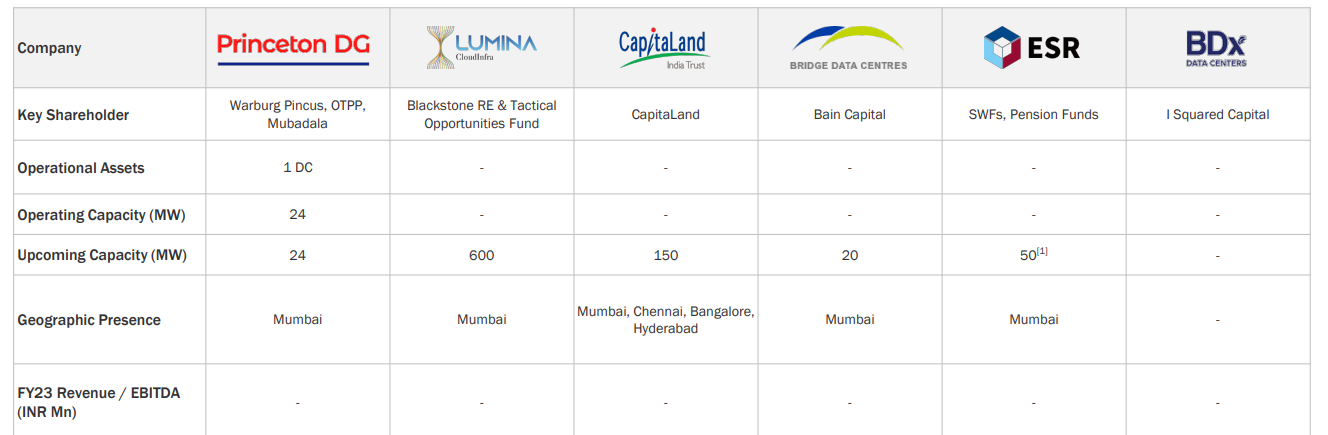

Data Center Platforms Started By Financial Investors

Princeton DG: Signed a 25 years agreement with Tata Power to meet the power needs of its 48 MW Mumbai DC.

Lumina Data Centres: By 2030, Blackstone plans to set up data centers in five Indian cities with a total capacity of 600 MW.

CapitaLand: 1st phase of the Mumbai DC will deliver 30.5 MW and will be Ready-for-Service by mid-2025.

Bridge Data Centres: The first asset is under construction and will deliver 8 MW by 2024 and 20 MW at full build-out.

ESR: Have launched ESR DC Fund 1 for development of its data centre business.

BDx Data Centers: Pan-Asian DC platform set-up by I Squared; actively looking for potential land parcels to enter Indian Market.

Global Players Strategically Making Their Presence In India With Different Ventures

Colt Data Centre Services: Planning to invest ~US $1.3 Bn for developing ~270 MW total DC capacity in Mumbai and Chennai over the next 3-5 years.

Digital Connexion: Reliance invested US $45 Mn to become a 33% shareholder along with Digital Realty and Brookfield Infrastructure in this JV.

ACx Data Centres: Aims to deliver DC Capacity of 1 GW by 2030. Planning to invest ~US $5 Bn over the next 5 years.

Equinix: Acquired a 6-acre land parcel in Chennai to expand its footprint in India.

Everyonr: The 1st DC under the JV is getting constructed in Mumbai; will deliver 12 MW of IT load in the first phase.

Digital Edge: Will invest around US $170 Mn in setting up the Navi Mumbai DC with a capacity of 15 MW for the first phase of the project of overall size 300 MW.

Domestic Indian Players Continue To Serve Their Share Of The Market

Web Werks: Signed MoUs/Agreements to invest in data centers in Chennai, Telangana, and Bangalore.

ESDS: Amongst the preferred managed DC and cloud service providers for SMBs.

Pi: Planning to expand operations to Hyderabad with an investment of INR 200 Cr over a period of next 2 years.

NxtGen: Targeted to invest INR 13 Bn to develop more assets.

L&T Cloudfiniti: Upcoming facilities in Mumbai and Chennai.

Techno Electric & Engineering Co. Ltd.: Plans to develop 250 MW of hyper density data centers in India over the next 5 years.

6. India’s Data Centre Capacity to Grow 12x by FY30E

Currently, India’s DC capacity is ~1-1.5 GW, far behind Europe’s 10 GW. However, with a larger internet user base (India: 898M vs. Europe: 400M), India’s DC capacity is expected to reach 17 GW by FY30E, accounting for 15% of incremental power demand.

Major Players Expanding in India

Global Data Centre Giants: NTT, AWS, Colt DCS

Indian Conglomerates: Reliance, Adani

Key Occupiers: Amazon, Netflix, banks, fintech firms

Investment Momentum: USD 27 billion announced in the last 36-48 months

Power Sector to Benefit: Siemens & ABB India Leading the Charge

Siemens: 40-45% exposure to India’s DC capex.

ABB India: 20-25% exposure, benefiting from rising power demand.

L&T, Voltas, Bluestar: 15% exposure each to India’s DC boom.

Cummins: 10% of its power generation revenues in FY24 came from data centre-related sales.

By FY30E, India will not only have a 12x larger DC footprint, but it will also emerge as a key global data centre hub.

Installed DC Capacity In India (MW)

7. Data Centre Capex Breakdown: USD 4-5 Million per MW

Typical DC projects in India are 20-25 MW in capacity, with capex distributed as follows:

Power-Related Costs: 30% (Largest component)

Automation, HVAC, EPC (Engineering, Procurement, Construction): 15% each

Power Backup: 10% (Primarily imported, as 2,000+ KVA gensets lack local manufacturing)

Technology Hardware & Software: Provided by occupants (not included in capex costs)

Data center capex split

8. What is Driving Data Centre Market Growth in India?

India’s data centre (DC) market is expanding rapidly, driven by digital transformation, rising internet penetration, policy initiatives, increasing data consumption, and AI adoption. The surge in data traffic from industries like finance, telecom, e-commerce, and cloud computing, coupled with the rollout of 5G, is accelerating demand for secure and scalable data storage and processing facilities.

A comparison of India’s DC growth drivers with global markets

9. Key Growth Drivers

AI & High-Performance Computing (HPC)

AI-driven applications and HPC workloads are increasing demand for high-power density DCs with advanced cooling systems.

Generative AI alone could add ~USD 400 billion to India’s GDP by 2029-30, creating an unprecedented need for AI-ready data centres.

Regulatory & Policy Support

The Digital Personal Data Protection Act (DPDPA) 2023 strengthens data privacy and compliance, boosting cross-border trade and data localisation.

Government initiatives like the Draft Data Centre Policy, 2020, and IndiaAI Mission aim to create a favourable environment for DC investments.

International Investments & Infrastructure Status

India’s DC market has attracted USD 60 billion in investments from 2019-2024, with global tech giants expanding their presence.

By 2027, investment commitments are expected to surpass USD 100 billion, driven by real estate developers, private equity funds, and hyperscalers.

Growing Digital Penetration & 5G Deployment

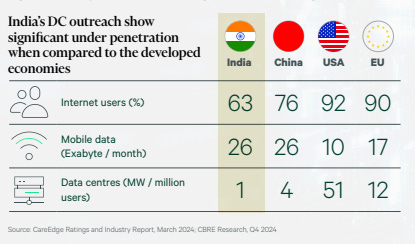

Internet penetration in India is growing rapidly, but DC capacity per million users remains lower than developed economies.

As mobile data usage continues to rise, India’s DC capacity is projected to reach ~1,600 MW by the end of 2024, up from 1,255 MW in 9M 2024.

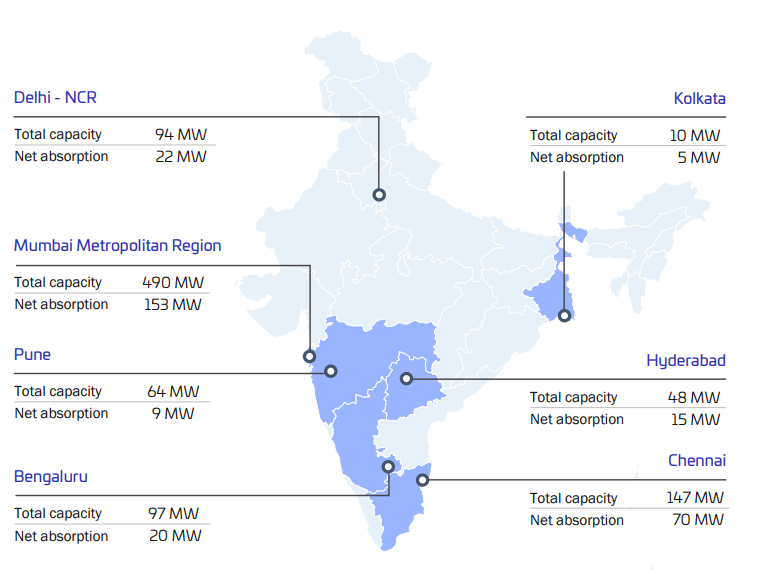

10. India’s Established Data Centre Markets: Mumbai & Chennai Leading the Race

Mumbai & Chennai: The Front-Runners

Both cities have emerged as dominant data centre hubs due to their strong digital infrastructure, connectivity, and power reliability.

1. Mumbai – India’s Data Centre Capital

Mumbai accounts for 48% of India’s total DC capacity, making it the country’s largest and most preferred DC destination.

Why is Mumbai the #1 DC Hub?

Submarine Cable Landing Stations – Ensuring best-in-class global latencies for seamless international connectivity.

Robust Infrastructure – Reliable power supply, road networks, and extensive fiber optic connectivity.

Strong Demand Base – A financial & telecom hub, Mumbai houses major BFSI institutions, hyperscalers, and cloud providers.

Minimal Natural Threats – Unlike coastal cities prone to cyclones, Mumbai faces no major climate risks, enhancing business continuity.

Mumbai’s Future Growth Potential

Over the next five years, ~35% of India’s additional DC capacity is expected to come from Mumbai.

New hyperscale investments and colocation expansions are set to further solidify Mumbai’s leadership in the DC space.

2. Chennai – India’s Fastest-Growing DC Market

Chennai is rapidly becoming a preferred alternative to Mumbai due to its similar infrastructure advantages.

Why is Chennai Emerging as a DC Hotspot?

Submarine Cable Connectivity – Chennai has a dense wet cable ecosystem, ensuring low-latency global connectivity similar to Mumbai.

Growing Hyperscaler & Enterprise Demand – Fueled by APAC-focused tech firms, BFSI players, and cloud providers.

Massive Capacity Expansion – ~25% of India’s incremental DC capacity is expected to come from Chennai.

MIST Cable System – The upcoming MIST submarine cable will enhance Chennai’s connectivity with APAC markets, further boosting demand.

Other Growing DC Markets in India

Delhi & Noida – The only major DC hubs in North India, catering to regional enterprise demand.

~15% of India’s incremental capacity is expected to come from Delhi.

Noida is witnessing substantial new DC developments.

Kolkata – An emerging DC hub in East India, but growth is still at an early stage.

Diversified Occupier Base Driving Demand

Technology firms, financial services, and government bodies are leading the demand for colocation data centres. Key occupiers include:

Technology companies & hyperscalers (AWS, Microsoft, Google)

BFSI & fintech firms (HDFC Bank, Paytm, NPCI)

OTT platforms & social media giants (Netflix, Meta, YouTube)

Public sector undertakings shifting to third-party colocation DCs due to increasing digitisation.

Data Centre Occupancy Levels (9M 2024)

Mumbai – 63%

Chennai – 76%

Bengaluru – 78%

Delhi-NCR – 75-80%

With continued expansion and new entrants, occupancy levels are expected to rise further in 2025.

Current Installed Capacity Of ~ 1 GW Of Which ~ 30% Is Taken Up By BFSI And Tech Industry

11. Investment Hotspots: Maharashtra & Tamil Nadu Leading the Charge

India’s cumulative DC investments (2019 - 2027 E)

Major DC investment deals in 2024

State-wise spread of DC investments (2019 - 2024)

India’s top DC investment destinations include Maharashtra, Tamil Nadu, Telangana, Uttar Pradesh, and West Bengal.

Between 2019 and 2024, India attracted ~USD 60 billion in DC investments.

By 2027, the cumulative investment commitment is projected to exceed USD 100 billion.

12. DATA CENTRE Industry Segmentation

12.1 Segmentation by Infrastructure Type

a. IT Infrastructure

Servers: The backbone of data centers, handling data processing and storage. Growing demand for high-performance servers is driven by AI, cloud computing, and big data.

Storage Systems: Includes solid-state drives (SSDs), storage area networks (SANs), and cloud storage solutions, offering faster and more reliable data retrieval.

Networking Equipment: Comprises routers, switches, and firewalls that manage data flow within and outside the data center. Software-defined networking (SDN) is improving efficiency.

b. Power Infrastructure

Uninterruptible Power Supply (UPS): Provides emergency power to ensure uninterrupted operation. Modern UPS systems focus on energy efficiency and scalability.

Generators: Serve as backup power sources during outages. Many data centers are adopting eco-friendly generators.

Power Distribution Units (PDUs): Distribute electrical power to servers and networking equipment. Intelligent PDUs offer remote monitoring for better energy management.

c. Cooling Infrastructure

Cooling Towers and Air Conditioning Units: Traditional heat dissipation methods, though energy-intensive.

Liquid Cooling Systems: Emerging as a more efficient alternative, using liquid-based solutions to absorb and dissipate heat.

d. Security Infrastructure

Physical Security: Includes biometric access controls, surveillance cameras, and on-site security personnel.

Cybersecurity Solutions: Firewalls, intrusion detection systems, and encryption protocols to protect against cyber threats.

12.2 Segmentation by Size & Scale

a. Hyperscale Data Centers

Large-scale data centers operated by companies like Amazon Web Services (AWS), Microsoft Azure, and Google Cloud.

These facilities house thousands of servers and support cloud services, AI applications, and big data analytics.

b. Colocation Data Centers: Shared facilities where multiple businesses rent space for their servers and IT infrastructure.

Advantages:

Lower capital investment compared to building an in-house data center.

Redundant power supply & cooling systems, reducing downtime risks.

c. Enterprise Data Centers: Privately owned and operated by a single organization to support its internal IT operations.

Benefits:

High security & data privacy, preferred by financial institutions and governments.

Custom-built for specific business needs like banking transactions or healthcare data storage.

d. Edge Data Centers: Smaller facilities located close to users to reduce latency and improve service performance.

Used in:

5G networks: Low-latency connectivity for real-time applications.

Autonomous vehicles: Instant data processing for navigation and safety.

Smart cities & IoT: Supports sensors and connected devices.

12.3 Segmentation by Deployment Model

On-Premises Data Centers: Owned and operated by organizations for internal use, offering full control over security and data management. Higher costs and maintenance compared to cloud alternatives.

Cloud Data Centers: Managed by third-party providers, offering services like Infrastructure as a Service (IaaS), Platform as a Service (PaaS), and Software as a Service (SaaS). Amazon plans to invest $13.2 billion in local cloud infrastructure over the next three years.

Hybrid Data Centers: A mix of on-premises and cloud environments, offering flexibility, scalability, and cost optimization

12.4 Segmentation by Tier Classification (Uptime Institute Standard)

Tier I: Basic infrastructure with 99.671% uptime.

Tier II: Redundant capacity components, offering 99.741% uptime.

Tier III: Concurrently maintainable with redundant components and multiple distribution paths, ensuring 99.982% uptime.

Tier IV: Fully fault-tolerant with 99.995% uptime, designed for mission-critical applications.

13. Key Risks and Challenges

While the Indian data center industry is experiencing rapid growth, it also faces several challenges and risks that could impact its expansion. Below are the major concerns:

1. High Capital & Operating Costs

Setting up hyperscale data centers requires massive investment in land, infrastructure, and technology.

Energy costs account for nearly 40% of a data center’s total operating expenses, making it difficult for smaller players to compete.

Real estate prices in Mumbai, Delhi, and Chennai are rising, increasing the cost of expansion.

2. Power Supply & Energy Constraints

Data centers are extremely power-intensive. India’s energy demand for data centers is expected to grow 10x by 2030.

Frequent power shortages & grid instability in certain regions pose risks to uptime.

Limited access to renewable energy in some areas makes sustainability efforts challenging.

3. Regulatory & Compliance Uncertainty

Data localization laws require businesses to store sensitive data within India, increasing compliance costs.

The Digital Personal Data Protection (DPDP) Act, 2023 mandates strict data security, but frequent changes in regulations create uncertainty.

Complex tax structures & approvals slow down data center expansion.

4. Cybersecurity Threats & Data Breaches

Cyberattacks in India surged by 24% in 2023, targeting financial, healthcare, and government data centers.

Ransomware attacks, DDoS attacks, and cloud security breaches are major concerns.

Lack of skilled cybersecurity professionals makes it difficult to implement robust security measures.

5. Skilled Workforce Shortage

India needs 2 million cloud computing & data center professionals by 2030, but there’s a major skill gap.

Specialized skills in AI, cloud security, and data center management are in short supply.

6. Land Acquisition & Infrastructure Challenges

Securing land for data centers in key locations (Mumbai, Chennai, Hyderabad) is expensive and slow due to regulatory hurdles.

Poor infrastructure in Tier 2 & Tier 3 cities (road connectivity, power supply, fiber networks) limits expansion.

7. Environmental Concerns & Sustainability Issues

Data centers generate massive carbon footprints, with power consumption expected to surpass 5GW by 2028.

Water usage for cooling systems is also a growing environmental concern.

Government regulations on energy efficiency & emissions are becoming stricter.

8. Competition from Global Cloud Giants

AWS, Google Cloud, and Microsoft Azure dominate the market, making it difficult for smaller Indian players to compete.

Foreign players invest billions in India, creating pricing pressure for domestic data center operators.

CONCLUSION:

As the digital landscape expands at an unprecedented pace, data centers stand as the silent workhorses of our hyper-connected world.

Powering AI, cloud computing, and vast data ecosystems, they are the backbone of everything from streaming services to financial transactions. Yet, as demand soars, so do the challenges.

Energy efficiency, sustainability, and security are no longer optional—they are the defining factors shaping the industry’s future. The pressure to reduce carbon footprints has sparked innovations in liquid cooling, renewable energy integration, and AI-driven optimizations.

Meanwhile, the rise of edge computing is shifting the paradigm, bringing processing power closer to users and reducing latency like never before.

But with every leap forward comes new questions. Can data centers scale at the rate digital transformation demands without compromising efficiency? How will quantum computing and next-gen infrastructure reshape storage and processing capabilities?

And perhaps most intriguingly—what happens when the world’s data outgrows even the most advanced systems?

The industry is at a crossroads, balancing innovation with sustainability, speed with security. The next evolution isn’t just about expansion—it’s about redefining what’s possible.