Industry Report: Construction Industry

What Really Drives Construction Growth And Where the Cracks Still Are

Here, at EquityEdge Research, we deep dive into complex Articles and Reports and make it easier for you by presenting everything, RIGHT HERE!!

Please Fill the form Below if you are interested in our Services and would like a Free Sample of our Equity Research Report covering a Small/Micro-cap Company.

Check out our Previous Industry Report:

What do you mean by the Construction Industry?

Global Construction Industry.

Indian Construction Industry.

Industry Segmentation.

Import/Export Dynamics.

Key Trends/Growth Drivers:

Industry Risk and Future Challenges.

Major Players in India.

Conclusion.

1. What do you mean by the Construction Industry?

The construction industry is a fundamental pillar of economic development, encompassing the activities involved in the planning, design, construction, renovation, and maintenance of physical structures and infrastructure. It covers a wide range of projects, including residential housing, commercial buildings, industrial facilities, and large-scale infrastructure such as roads, bridges, airports, railways, and public utilities. The industry brings together multiple stakeholders—architects, engineers, contractors, suppliers, and skilled and unskilled labour to transform raw materials into durable assets that support economic activity and improve quality of life. By generating large-scale employment, stimulating demand for materials such as cement, steel, and machinery, and enabling urbanization and industrial expansion, the construction industry plays a critical role in sustaining long-term economic growth and national development.

Sources- World Bank, International Labour Organization (ILO), OECD, United Nations Statistics Division (UNSD), McKinsey Global Institute, Investopedia

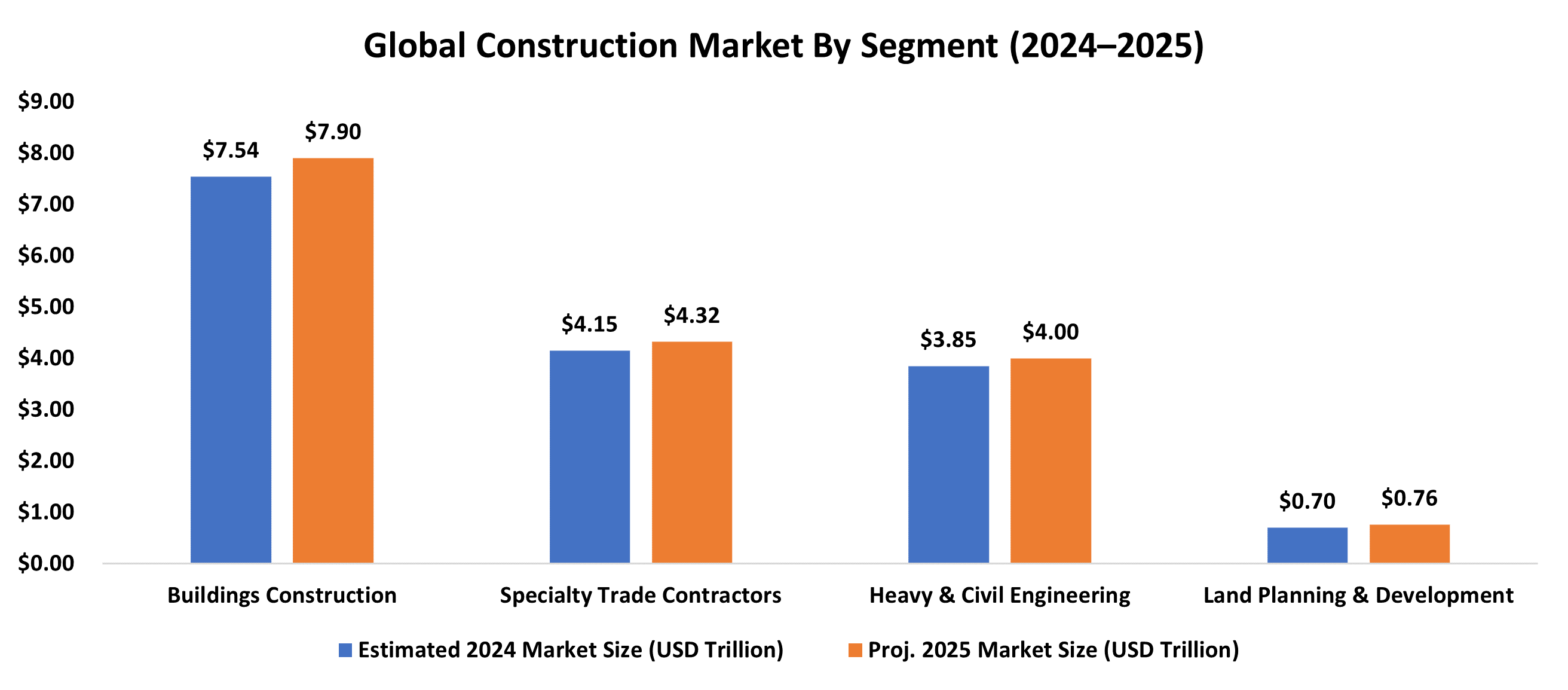

2. Global Construction Industry:

2.1 Market Size and Growth

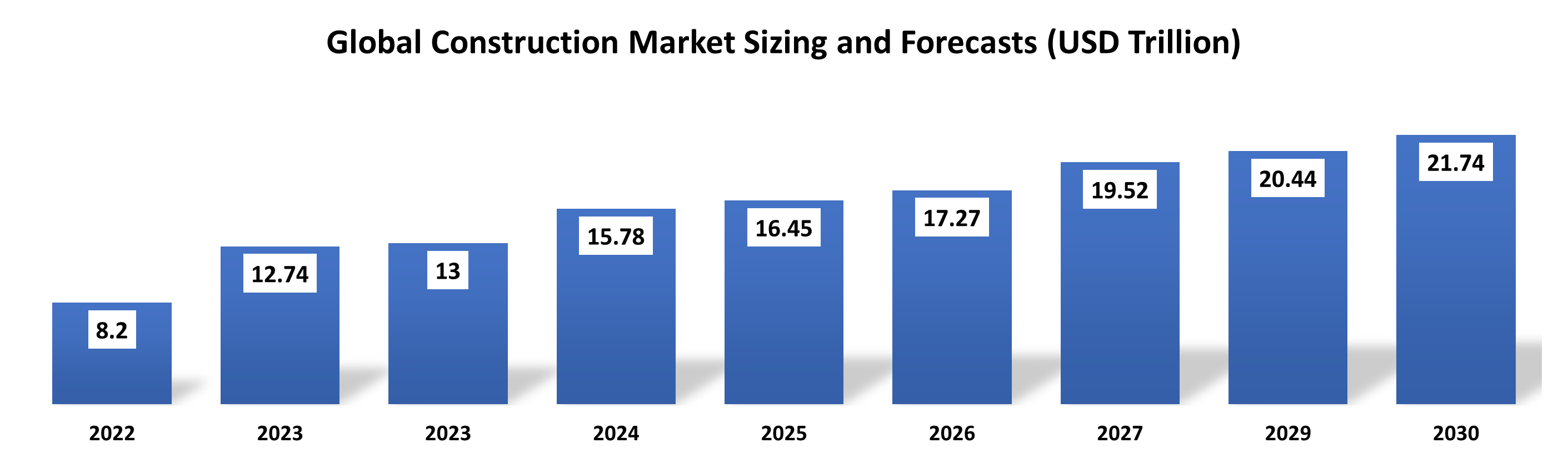

The global construction market is currently valued between 15.78 trillion USD and 16.04 trillion USD as of 2024. The sector is expected to expand to approximately 16.45 trillion USD in 2025, representing a compound annual growth rate (CAGR) of 4.3% in the near term.

Looking further ahead, industry forecasts suggest the market will reach a valuation of 21.74 trillion USD by 2030, supported by a projected growth acceleration of 5.9% during the late 2020s.

Total spending in the industry accounts for roughly 13% of global economic production, with the 2023 gross annual output having reached 13 trillion USD.

2.2 Key Segments

Building construction remains the most significant segment of the market, accounting for approximately 46.43% of the total, or 7.45 trillion USD, in 2024.

Infrastructure construction is another vital pillar, estimated at 3.82 trillion USD for 2025, where transportation projects serve as a primary anchor with a 36.78% share of that specific segment.

The residential sector continues to be a massive driver of activity, valued at 5.29 trillion USD in 2023, though it currently faces sensitivity to fluctuating interest rates.

Additionally, an industrial “supercycle” is emerging in the form of data center construction, with a global project pipeline that reached 157.8 billion USD by late 2025.

2.3 Regional Highlights

The Asia-Pacific region maintains its position as the dominant global power in construction, claiming a 46.54% share of total revenue in 2024, largely driven by the rapid urbanization occurring in China and India.

North America represents the second-largest market, with United States construction spending surpassing 2 trillion USD in 2024 as it transitions toward high-tech industrial assets and energy infrastructure.

Meanwhile, the Middle East and Africa is recognized as the fastest-growing regional market with a projected CAGR of 7.56% through 2030, a trend heavily influenced by large-scale infrastructure developments and the ongoing Belt and Road Initiative.

2.4 Technology Drivers

Digital transformation is rapidly becoming the standard for the industry, with Building Information Modeling (BIM) adoption exceeding 70% in advanced economies such as Germany.

The expansion of smart city infrastructure is another major trend, with the global market for such IoT-enabled projects expected to reach 1.7 trillion USD by 2025.

Other emerging technologies are also seeing significant growth, including Digital Twins, which are projected to expand at a 30% CAGR, and modular construction, which offers a 6.5% CAGR as firms seek faster and more efficient project delivery methods.

2.5 Key Challenges

The primary existential threat to the industry is a persistent and worsening shortage of skilled labor; the sector faced a global shortfall of roughly 500,000 workers in 2024, with nearly 75% of firms reporting recruitment difficulties.

This crisis is intensified by an aging workforce, as an estimated 53% of current skilled tradespeople are expected to reach retirement age by 2036.

Furthermore, macroeconomic pressures such as rising material costs which have consistently increased at rates of 1% to 3% above general inflation and new tariffs that pushed effective rates for construction goods to a 40-year high in 2025, continue to compress margins for contractors.

2.6 Major Industry Participants

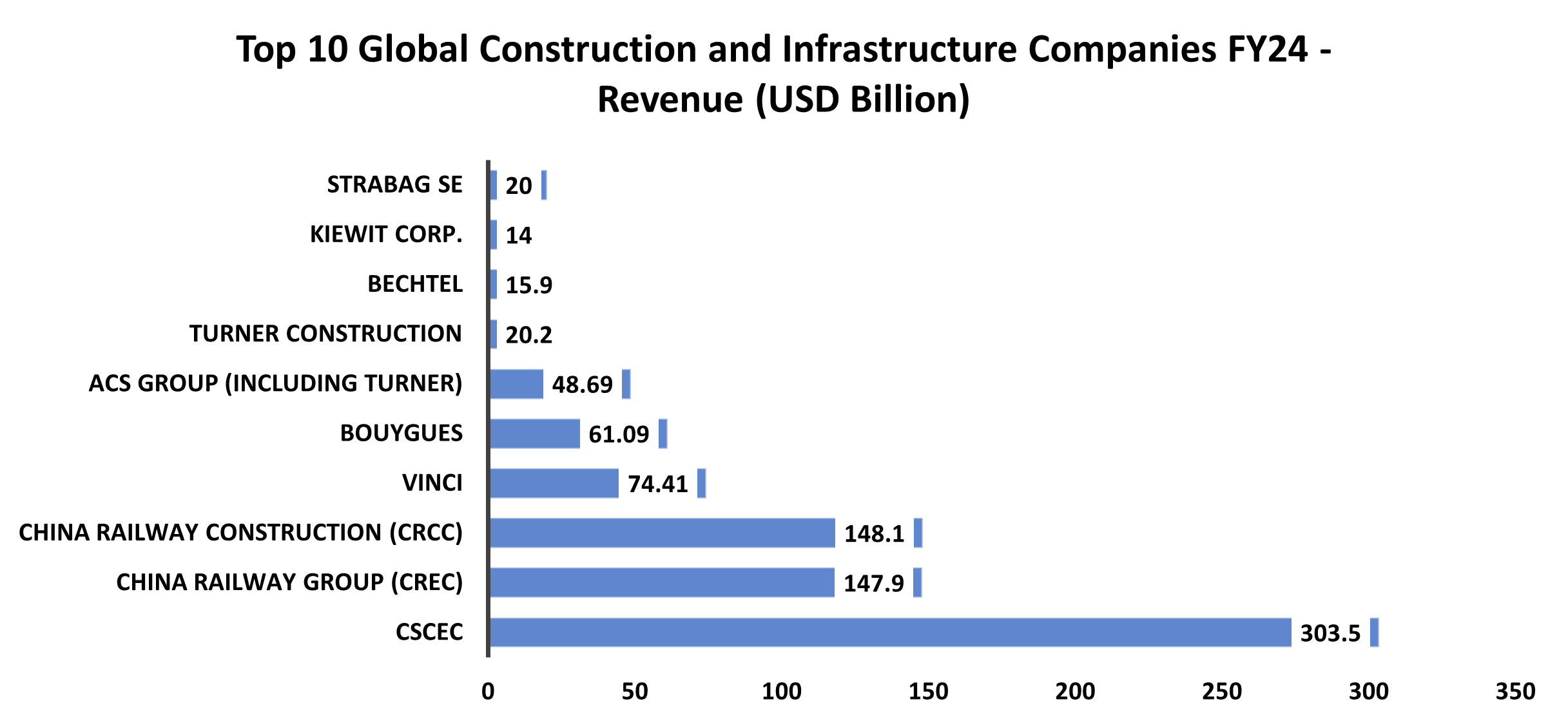

The competitive landscape is led by massive Chinese state-owned enterprises, with the China State Construction Engineering Corporation (CSCEC) remaining the world’s largest construction company, reporting a revenue of 303.50 billion USD in 2024.

Other major Chinese players include the China Railway Group (CREC) and China Railway Construction Corporation (CRCC), which generated revenues of approximately 158.62 billion USD and 148.10 billion USD respectively.

In Europe, the market is dominated by firms like France’s VINCI, which reported 74.41 billion USD in revenue, and Bouygues, while the United States market is led by Turner Construction with 20.2 billion USD in 2024 sales.

Sources: McKinsey & Company , Statista , Mordor Intelligence , World Population Review, CompaniesMarketCap , CSCEC Official Report , VINCI Official Report , GlobeNewswire, Bouygues Full-Year Results, ACS Group Press Release , Construction Dive , Turner Construction.

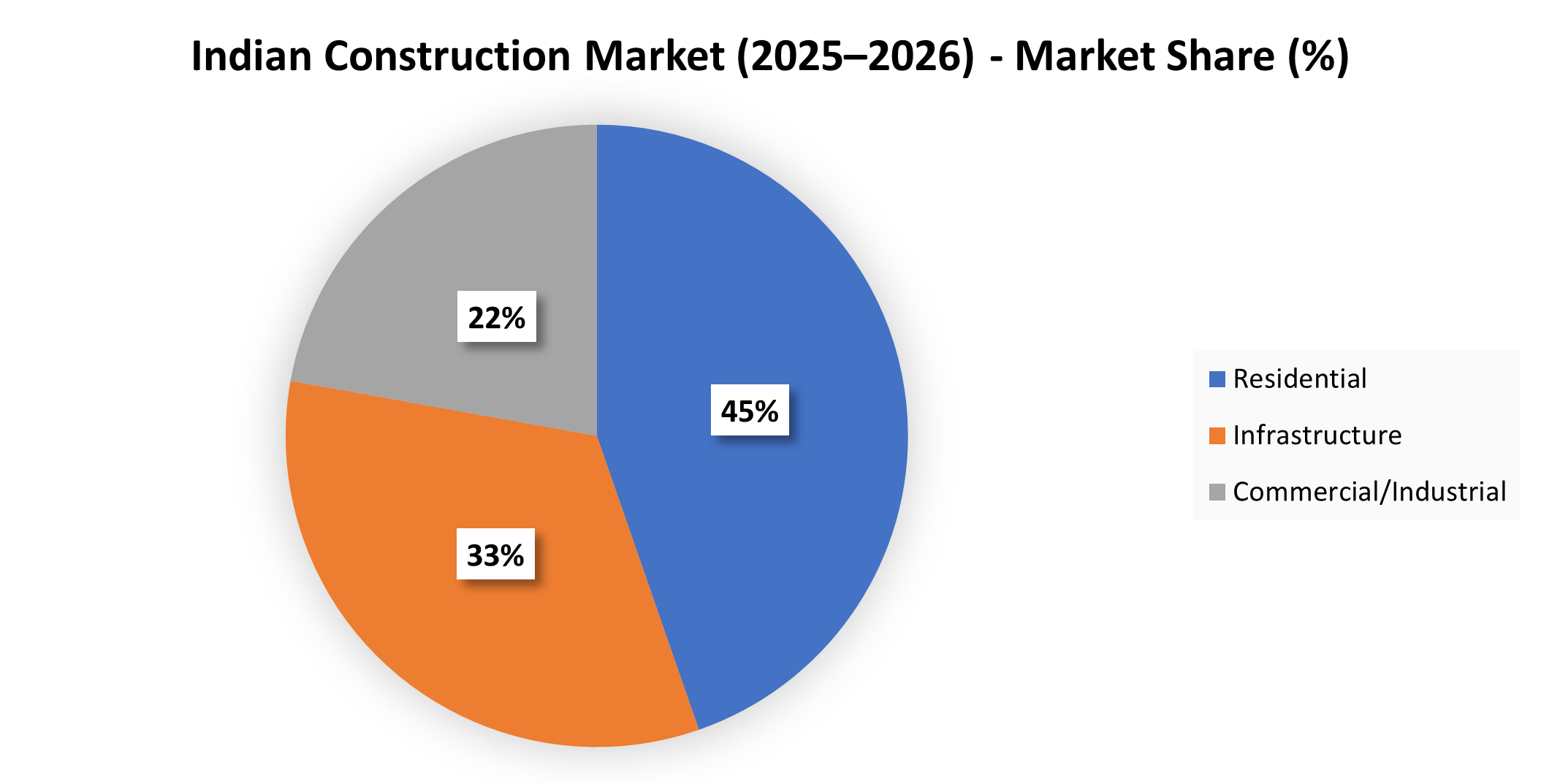

3. Indian Construction Industry:

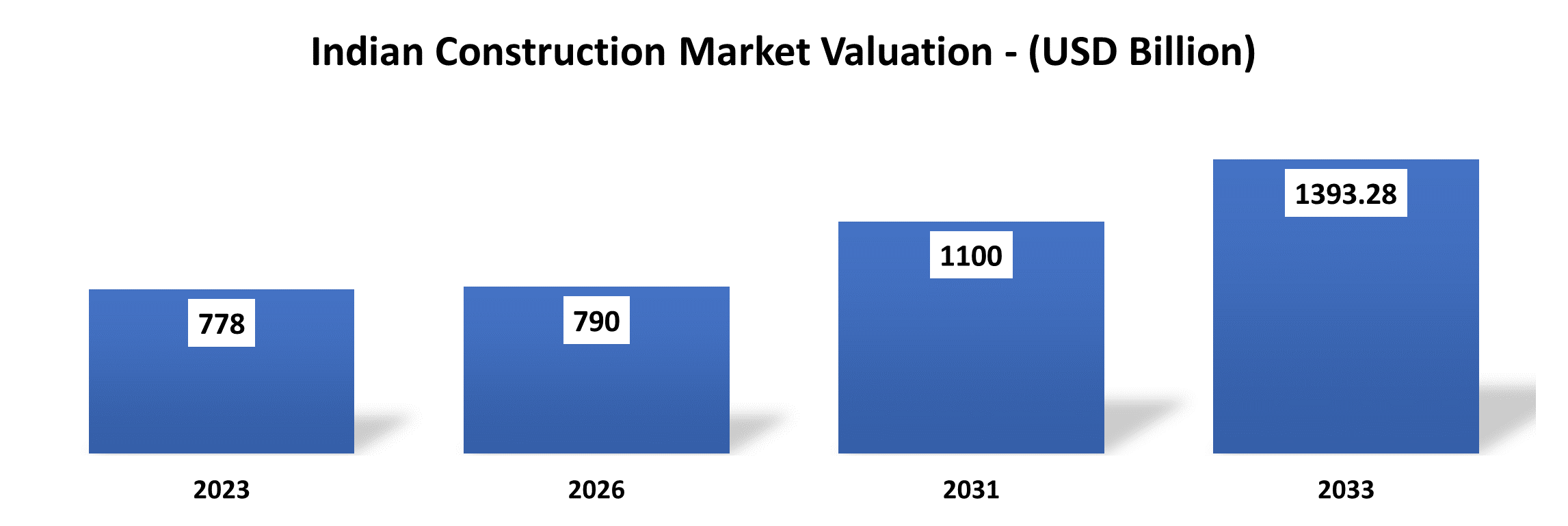

3.1 Market Size and Growth:

The Indian construction market is valued at approximately US$ 790 billion in 2026, following a consistent growth momentum that achieved a 14.2% CAGR between 2020 and 2024.

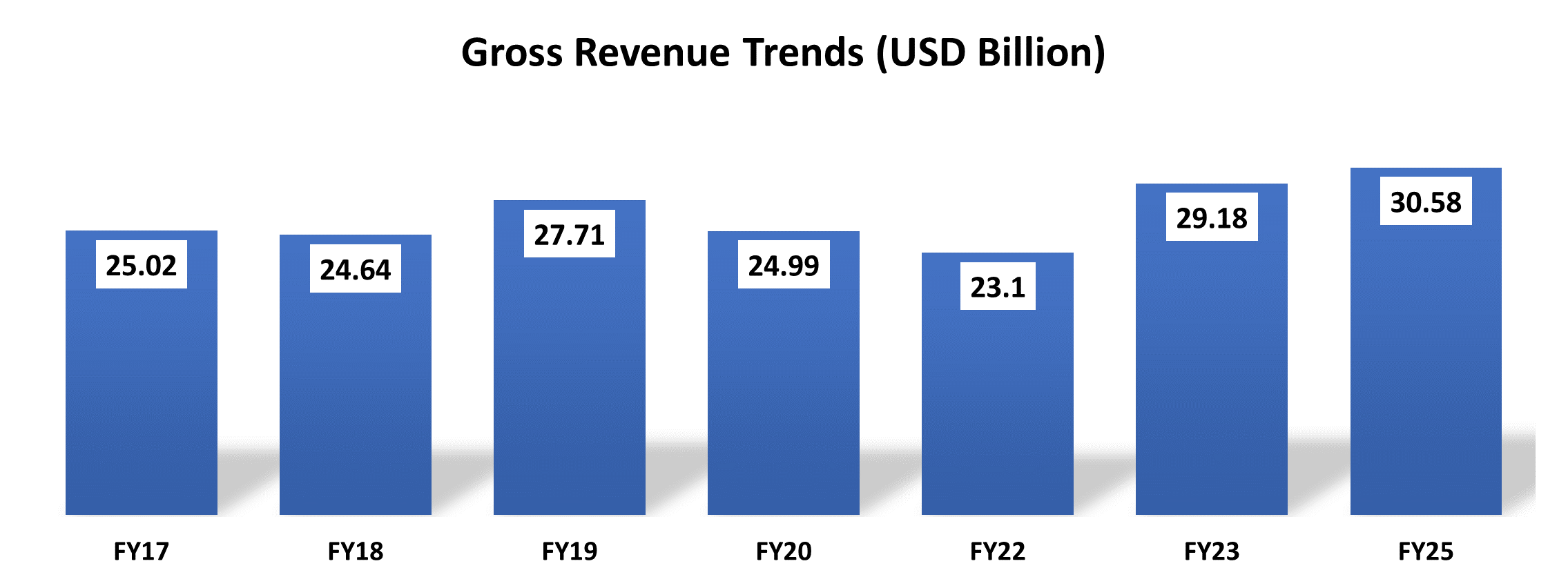

Gross revenue trends for the infrastructure sector specifically highlight a significant recovery from US$ 23.10 billion in FY22 to US$ 30.58 billion in FY25.

The industry contributes roughly 8% to the national GDP and recorded a real Gross Value Added (GVA) growth rate of 9.4% in the 2024-25 fiscal year.

Looking forward, the broader ecosystem is projected to reach a valuation of US$ 1,100 billion by 2031 as it remains the primary engine for India’s transition toward a US$ 26,000 billion economy by 2047.

3.2 Key Segments:

The industry is bifurcated into high-impact segments led by residential construction, which commanded a 44.68% market share in 2025, with apartments and condominiums accounting for 75% of total residential activity.

Growth in infrastructure-related activities during FY24 was exceptionally strong, with National Highway construction leading at 20.00%, followed by electricity generation at 6.22% and cargo at major ports at 4.55%.

Road construction pace significantly accelerated to 34 kms per day in FY24, and while it adjusted to 29 kms per day in FY25, the government has set a long-term target of 100 kms per day by 2047.

The commercial segment continues to be driven by office space demand, which holds a 60.90% revenue share, alongside a projected 20% CAGR for the data center industry through 2028.

3.3 Regional Highlights:

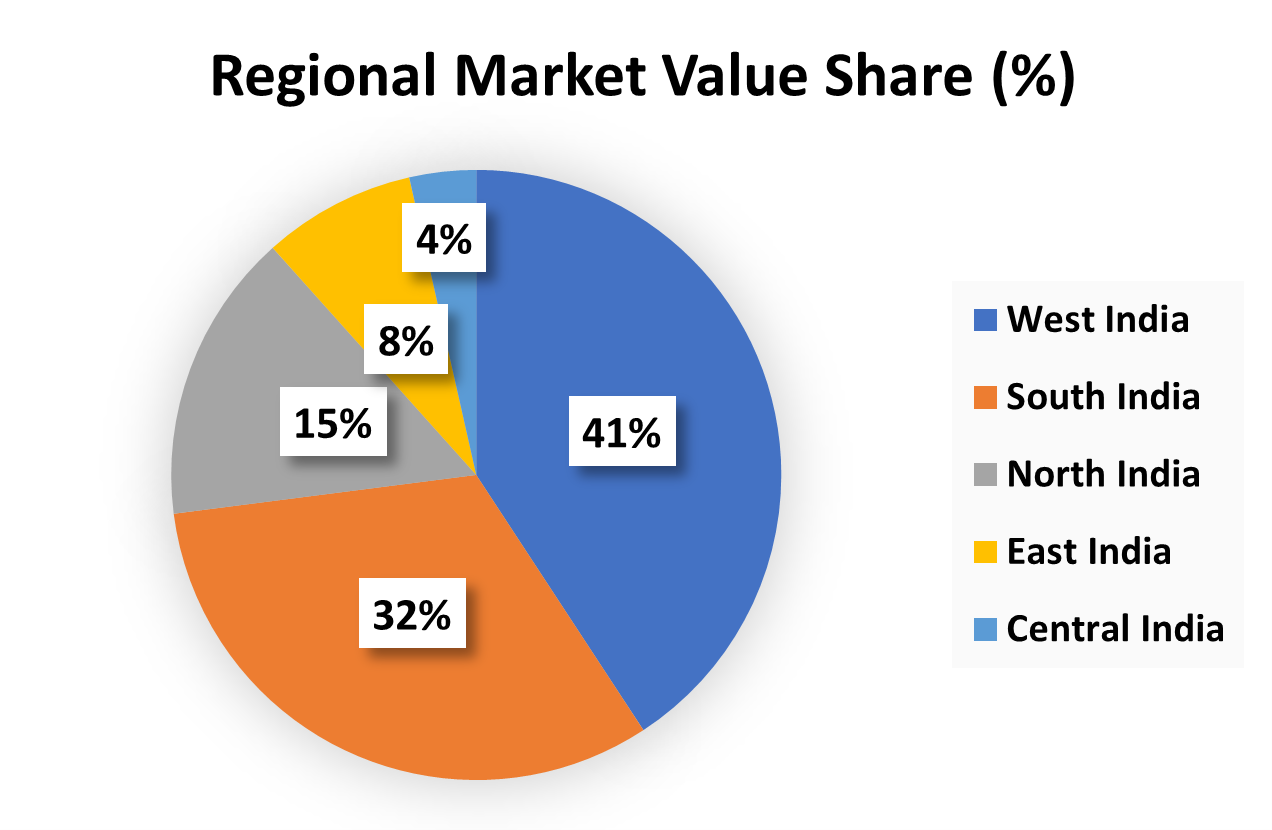

West India remains the dominant geographical contributor, accounting for 40.77% of the total construction market value in 2025 due to intensive industrial activity in Maharashtra and Gujarat.

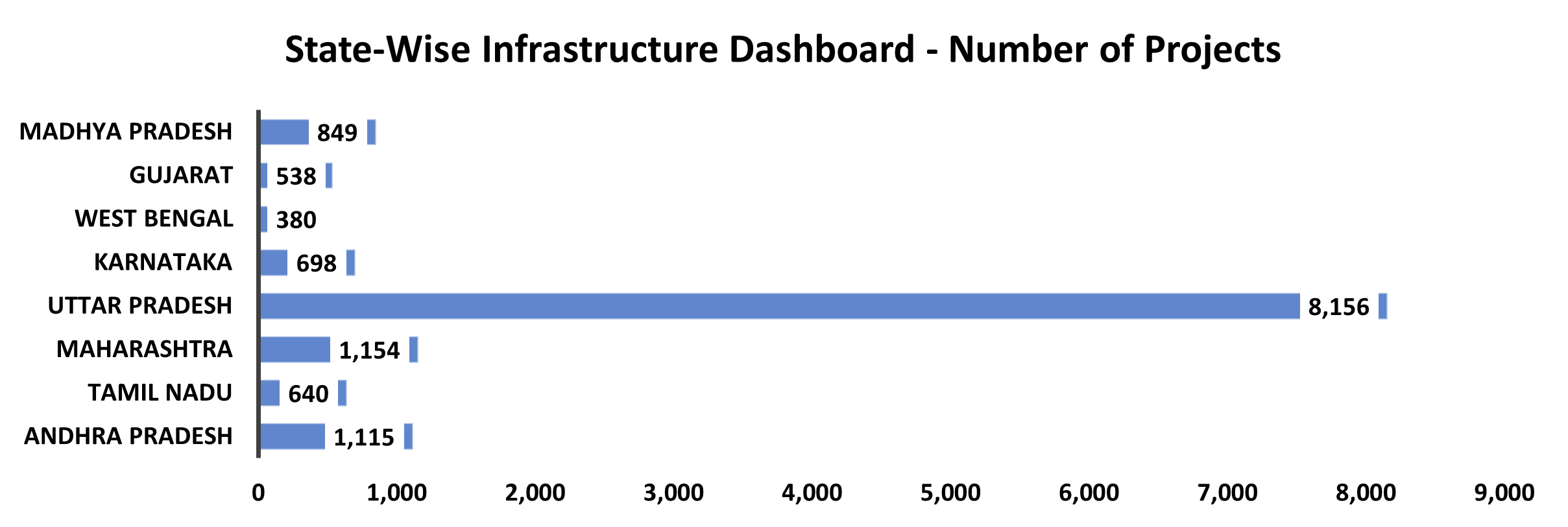

Significant capital outlays are also concentrated in South India, where Andhra Pradesh and Tamil Nadu lead with estimated outlays under the National Infrastructure Pipeline of US$ 186.81 billion and US$ 101.30 billion respectively.

While Maharashtra follows with a US$ 92.40 billion project pipeline, East India has been identified as the fastest-growing region with a projected growth rate of 7.24% through 2031.

3.4 Technology Drivers:

The sector is undergoing a digital transformation supported by approximately US$ 10 billion in construction technology investments expected by the end of 2025.

Key technological drivers include the widespread adoption of Building Information Modeling (BIM) and real-time IoT monitoring for complex projects such as high-speed rail and metro expansions.

Modern Methods of Construction (MMC), including prefabrication and modular techniques, are growing at a CAGR of 7.25% as developers seek to mitigate labor shortages and compress project delivery timelines by up to 20%.

Sources: IBEF Infrastructure Industry Infographic 2025, Mordor Intelligence , Research and Markets , Invest India , MoSPI Flash Report August 2025 , CRISIL , ICRA , World Bank , and Annual Reports of L&T, MEIL, NCC, and Reliance Infrastructure.

4. Industry Segmentation:

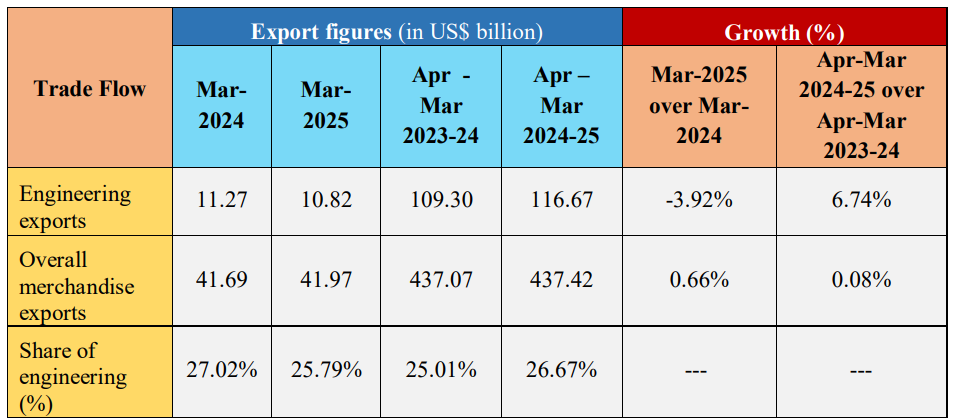

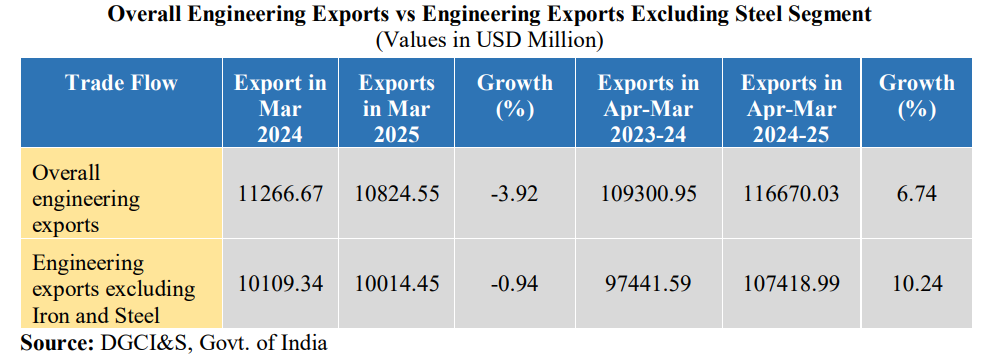

5. Import/Export Dynamics:

5.1 Exports:

Engineering goods (including construction machinery, fabricated structures, and related products) reached a record USD 116.7 billion in FY25, up 6.74% YoY.

Engineering exports now account for 26.7% of India’s merchandise exports.

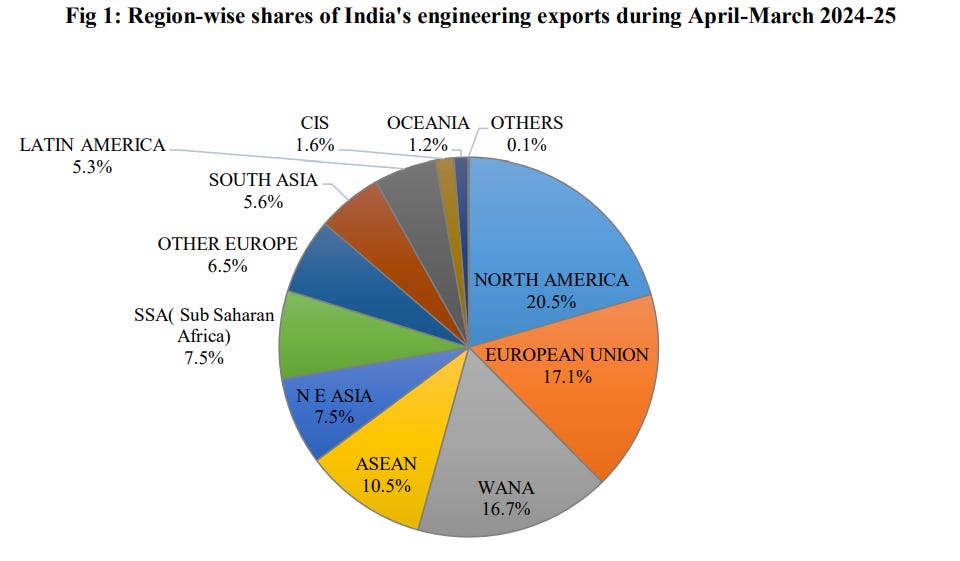

Top export destinations: USA (20.5%), EU (17.1%), West Asia & North Africa (16.7%); significant growth in France, Nepal, and the UK.

Region-wise engineering exports in April-May 2024-25 vis-à-vis April-March 2023-24.

Key exported products: Iron and steel, non-ferrous metals (copper, aluminum), construction machinery, office equipment, and fabricated structures.

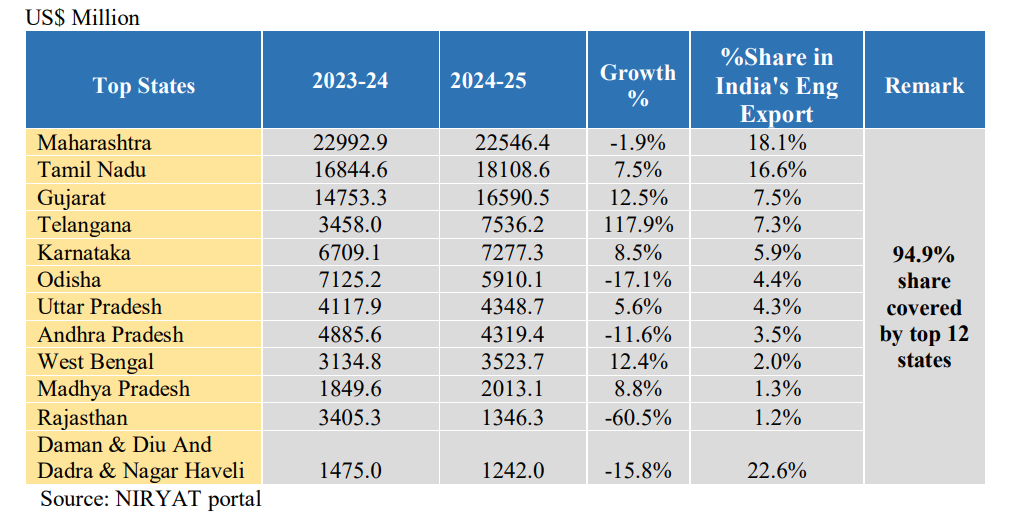

Top state-wise engineering export performance – April-May 2024-25.

5.2 Imports:

India imports construction machinery, advanced equipment, and specialized materials from China, Germany, the USA, Japan, and South Korea.

The trade balance in engineering goods remains positive, with exports outpacing imports in recent years.

India’s engineering imports

6. Key Trends/Growth Drivers:

6.1 Infrastructure Spending and Urbanization as Structural Demand Drivers:

One of the strongest growth drivers for the construction industry is increasing global infrastructure spending, which is being prioritized by governments to support economic expansion and connectivity.

The global construction market reached an estimated $16.45 trillion in 2025, up from $13.57 trillion in 2020, and is projected to grow to $20.44 trillion by 2029, reflecting sustained investment momentum across public works and utilities projects.

Asia-Pacific alone accounted for approximately $5.7 trillion in construction value in 2024 and is expected to expand further by 2030. Emerging economies, particularly China, the United States, and India, are projected to contribute nearly 60% of total global construction value through this decade, highlighting how urbanization and national infrastructure plans are central growth drivers.

6.2 Shift Toward Organized and Large-Scale Real Estate Development:

Residential and commercial real estate continues to be a major lever of construction growth. With rising disposable incomes and migration toward urban centers, demand is shifting from basic housing units to organized, large-scale developments such as integrated townships, office complexes, and logistics hubs.

Residential construction remains the largest segment of construction activity globally, representing over 40% of total output, with urbanization trends - more than 55% of the world’s population living in cities as of 2022 - projected to reach around 80% by 2050, dramatically increasing the need for housing and related urban infrastructure.

6.3 Technology-Led Efficiency and Productivity Improvements:

Technological adoption - including Building Information Modeling (BIM), modular construction, and digital project management tools is reshaping execution efficiency and cost structures in the industry.

Digital technologies correlate with productivity gains of around 15% or more, while the global prefabricated building market is expected to grow at roughly 6.6% CAGR through 2030. BIM adoption rates are especially high among larger firms (more than 70% in some regions) and integrated digital platforms are increasingly seen as essential for reducing delays and overruns in major projects

6.4 Sustainability Standards and Regulatory Compliance Driving Industry Consolidation:

Sustainability is no longer a peripheral trend but a core growth driver affecting materials, processes, and project financing. The global green building market is projected to reach over $227 billion by 2026, reflecting rising demand for energy-efficient and environmentally compliant construction.

Regulatory focus on emissions and resource use, combined with incentives for green infrastructure, is encouraging larger construction firms to adopt sustainable practices early, gaining competitive advantage and access to institutional contracts.

Sources- dojobusiness, globalgrowthinsights, McKinsey Global Institute, World Economic Forum (Future of Construction), Oxford Economics / Global Construction Perspectives, Deloitte Global Construction Outlook

7. Industry Risks and Future Challenges:

7.1 Project Delays & Cost Overruns:

Project execution delays remain a structural issue due to land acquisition hurdles, regulatory approvals, and funding gaps.

As of 2024–25, ~45% of large central infrastructure projects monitored by MoSPI faced time overruns.

Aggregate cost overruns exceed ₹5.1 lakh crore, translating to ~20% escalation over original project costs.

Average delay period stands at 30–36 months, impacting cash flows and IRRs for EPC players.

Impact: Margin erosion stretched working capital cycles, and elevated balance-sheet risk.

7.2 Skilled Labour Shortage & Productivity Issues:

Despite a large workforce, the industry faces an acute shortage of skilled manpower.

India’s construction workforce is estimated at ~70 million, but less than 10% is formally skilled.

Wage inflation for skilled workers has risen 12–15% annually in urban infrastructure projects.

Impact: Lower productivity, execution inefficiencies, quality risks, and higher project costs.

7.3 Financing Constraints & Liquidity Stress:

Construction companies—especially mid-sized EPC players—continue to face funding challenges.

Delayed payments from government bodies often stretch receivable cycles beyond 180–240 days.

Banks remain cautious due to legacy NPAs in infrastructure lending, increasing dependence on high-cost debt.

Impact: Higher leverage, interest cost pressure, and limited bidding capacity for new projects.

7.4 Raw Material Price Volatility:

Input costs are highly cyclical and difficult to hedge in fixed-price contracts.

Steel prices show volatility of 15–20% YoY.

Cement prices fluctuate 8–12% YoY, particularly during peak construction cycles.

Impact: Compressed margins, conservative bidding, and contract renegotiation risks.

7.5 Regulatory & Land Acquisition Challenges:

Multi-layered approval processes and state-level policy variations remain key execution bottlenecks.

Environmental clearances, utility shifting, and right-of-way issues frequently delay project start dates by 6–18 months.

Impact: Delayed revenue recognition and uncertainty in project timelines.

7.6 Environmental, Climate & Safety Risks:

Increasing climate volatility and stricter ESG norms are emerging as material risks.

Extreme weather events disrupt project timelines and raise insurance and compliance costs.

Green construction norms require additional capex and planning capabilities.

Impact: Higher compliance costs and execution uncertainty, particularly for legacy contractors.

(Sources: Ministry of Statistics & Programme Implementation, RBI & Reuters, Equipment Rentals India – Industry Risk & Policy Analysis, Financial Express & LiveMint – Construction Sector Challenges, Academic & Industry Studies on BIM and Digital Adoption in Construction)

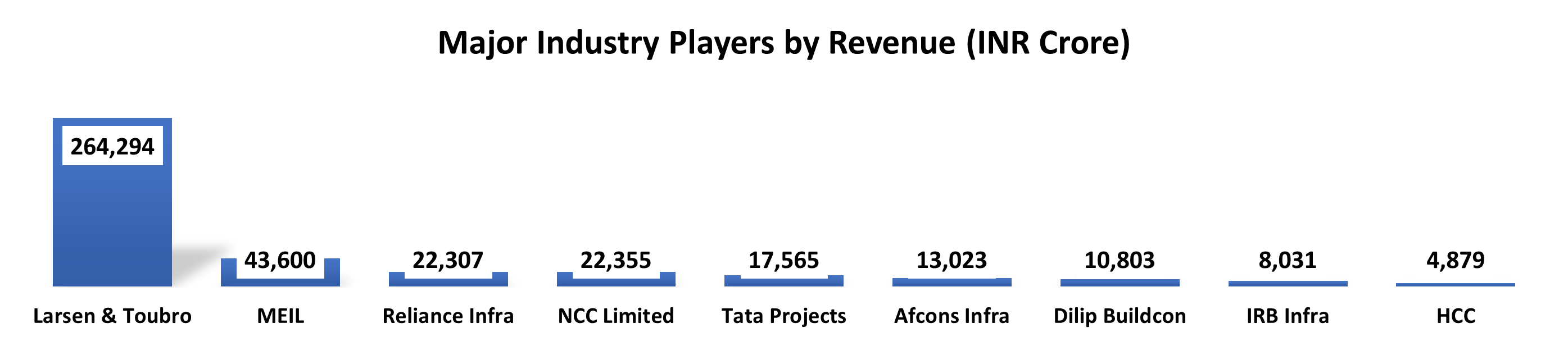

8. Major Players in India:

8.1 Larsen & Toubro (L&T)

Larsen & Toubro is India’s largest and most diversified construction and engineering company, with leadership across EPC projects in transportation, power, water, hydrocarbons, heavy engineering, defence, and urban infrastructure. The company has a strong presence in both domestic and international markets, backed by advanced project execution capabilities and a robust order book. L&T benefits significantly from India’s infrastructure push and remains the industry benchmark in scale, technology, and execution.

8.2 MEIL (Megha Engineering & Infrastructures Ltd.)

MEIL is a fast-growing infrastructure company with a strong presence in irrigation projects, water supply, power generation, oil & gas pipelines, and urban infrastructure. The company has gained prominence through large government contracts, especially in irrigation and water management. MEIL’s aggressive bidding strategy and execution strength have enabled it to emerge as one of the top revenue-generating construction firms in India.

8.3 Reliance Infrastructure

Reliance Infrastructure operates primarily in transport infrastructure, power projects, metro rail, and defence-related construction. Historically known for large-scale EPC projects, the company has shifted focus toward asset monetisation, defence manufacturing, and selective infrastructure development. While financial stress has reduced its market presence compared to peers, it remains a recognizable name in India’s construction ecosystem.

8.4 NCC Limited

NCC Limited is a well-established EPC player with operations spanning buildings, transportation, water & environment, irrigation, electrical projects, and mining. The company has a diversified order book and strong exposure to state and central government infrastructure projects. NCC’s execution track record, especially in irrigation and urban infrastructure, positions it as a mid-to-large cap construction company with steady growth prospects.

8.5 Tata Projects

Tata Projects is part of the Tata Group and focuses on industrial construction, urban infrastructure, transportation, power transmission, and water projects. Known for high governance standards and quality execution, the company is increasingly participating in complex and technology-intensive projects such as data centres, metro systems, and smart infrastructure. Tata Projects benefits from strong parentage and long-term relationships with both public and private clients.

8.6 Afcons Infrastructure

Afcons Infrastructure is a subsidiary of the Shapoorji Pallonji Group and is one of India’s leading heavy civil engineering and marine construction companies. The company specializes in metros, bridges, tunnels, ports, offshore structures, and hydro projects, with a strong international footprint across Asia, Africa, and the Middle East. Afcons is known for executing technically complex projects and has consistently maintained a healthy order pipeline.

8.7 Dilip Buildcon

Dilip Buildcon is a prominent road and highway construction company, with strong exposure to EPC and HAM (Hybrid Annuity Model) projects. The company also operates in mining, irrigation, and urban infrastructure. Dilip Buildcon benefited significantly from India’s highway expansion phase, though high leverage and working capital intensity remain key concerns.

8.8 IRB Infrastructure Developers

IRB Infrastructure is one of India’s largest BOT and HAM-based road developers, with a portfolio of toll roads, highways, and expressways. The company combines project development with construction capabilities, generating long-term annuity and toll revenues. IRB’s asset monetisation strategy and focus on road infrastructure align well with the government’s transport infrastructure agenda.

8.9 HCC (Hindustan Construction Company)

HCC is a legacy infrastructure company with expertise in hydro power, tunnels, dams, metro rail, and nuclear infrastructure. Despite facing financial and execution challenges in recent years, HCC remains technically strong and is involved in several complex civil engineering projects. Ongoing restructuring and asset monetisation efforts are aimed at stabilising operations.

9. Conclusion:

The Indian construction industry stands at a pivotal juncture, supported by strong structural drivers such as sustained government capital expenditure, large-scale infrastructure programs, rapid urbanisation, and rising private sector participation. Initiatives including the National Infrastructure Pipeline (NIP), Bharatmala, PM Gati Shakti, Smart Cities Mission, and renewable energy expansion continue to provide long-term visibility for project awards across roads, railways, urban infrastructure, power, and water segments.

However, the sector remains execution-intensive and capital-heavy, with persistent challenges such as project delays, cost overruns, skilled labour shortages, regulatory complexities, and input cost volatility. These factors create significant divergence in performance between large, well-capitalised EPC players and mid-sized or leveraged contractors, making balance-sheet strength, execution capability, and working-capital discipline key differentiators.

Over the medium to long term, industry consolidation is likely to accelerate, favouring companies with strong order books, technological adoption, asset-light strategies, and access to diversified funding sources. Increased focus on digital project management, sustainability, and asset monetisation is expected to improve execution efficiency and return profiles. Overall, while risks remain inherent, the Indian construction industry offers sustained growth potential, with selective opportunities for structurally strong players aligned with India’s infrastructure-led development trajectory.

THANK YOU FOR READING!!

Researched By- Ayush, Naresh, and Mayank.

Hope you liked our work. Please Subscribe so that we can reach out to more People like you!

We are Proud to Announce Our New Launch of the Premium services where we Deep-dive into the Business and back you up with Robust Research.

We Provide services for different Level of Investors. You can Email us directly to start your journey!