Hello, our gentle readers.

Welcome to the very first edition of Industry Pulse.

As the name suggests, this series is dedicated to understanding the pulse of an industry, the developments that may seem like ordinary news headlines today but often become the forces shaping tomorrow’s competitive landscape.

Every industry has its own story unfolding in real time. A company announces a new factory. A competitor cuts prices. A regulation changes. A merger is announced. Demand shifts. Technology disrupts old business models. Individually, these may look like isolated events. Together, they reveal where an industry is heading.

That’s exactly what Industry Pulse aims to do.

In every edition, we’ll go beyond simply reporting the news. We’ll connect the dots, explain why each development matters, identify who stands to gain or lose, and explore the second- and third-order effects that are often overlooked. More importantly, we’ll ask the questions that investors should be thinking about before the market fully prices in these changes.

Whether you’re an investor, a business enthusiast, a student of economics, or simply curious about how industries evolve, we hope this series helps you see businesses not as individual companies, but as participants in an ever-changing competitive ecosystem.

This series is also something we want to build with you.

Your feedback, suggestions, criticisms, and ideas will play an important role in shaping future editions. If there’s an industry you’d like us to cover, a format you think would work better, or an angle you believe deserves more attention, please don’t hesitate to let us know. The conversations in the comments are just as valuable as the articles themselves.

Our goal isn’t simply to publish another industry update.

Our goal is to create a place where every edition helps us and all of you become better observers of businesses, sharper thinkers, and more informed investors.

So, let’s begin by taking the pulse of the industry.

The Big Picture

Artificial Intelligence is entering a new phase.

For the past few years, the conversation revolved around building smarter models making AI answer questions faster, write better code, or generate more realistic images. That race is far from over, but the industry’s center of gravity has shifted.

Today, the bigger question is no longer how intelligent AI can become, but how much real work it can perform and who owns the infrastructure that makes it possible.

Two powerful forces are now unfolding simultaneously.

The first is the rise of Agentic AI autonomous digital agents capable of planning, reasoning, and executing tasks with minimal human intervention. Businesses are beginning to deploy AI not merely as an assistant, but as a digital workforce embedded across operations.

The second is an unprecedented global infrastructure race. Every autonomous agent needs enormous computing power, pushing governments, hyperscalers, semiconductor companies, and data-center operators into a multi-trillion-dollar investment cycle spanning GPUs, chips, energy, cloud infrastructure, and connectivity.

These are not separate stories. They are two sides of the same equation.

One creates the demand for intelligence. The other builds the factories that manufacture it.

India sits at the center of both trends. Its IT services industry is rethinking a decades-old headcount-driven business model as enterprises embrace autonomous agents, while the country simultaneously attracts billions of dollars in investments for AI data centers, sovereign compute, and digital infrastructure.

This edition of Industry Pulse examines these twin developments not simply as technology news, but as signals of a deeper structural shift. Because the companies that dominate the AI economy tomorrow may not necessarily be the ones building the smartest models, but the ones deploying the most capable agents and controlling the infrastructure that keeps them running.

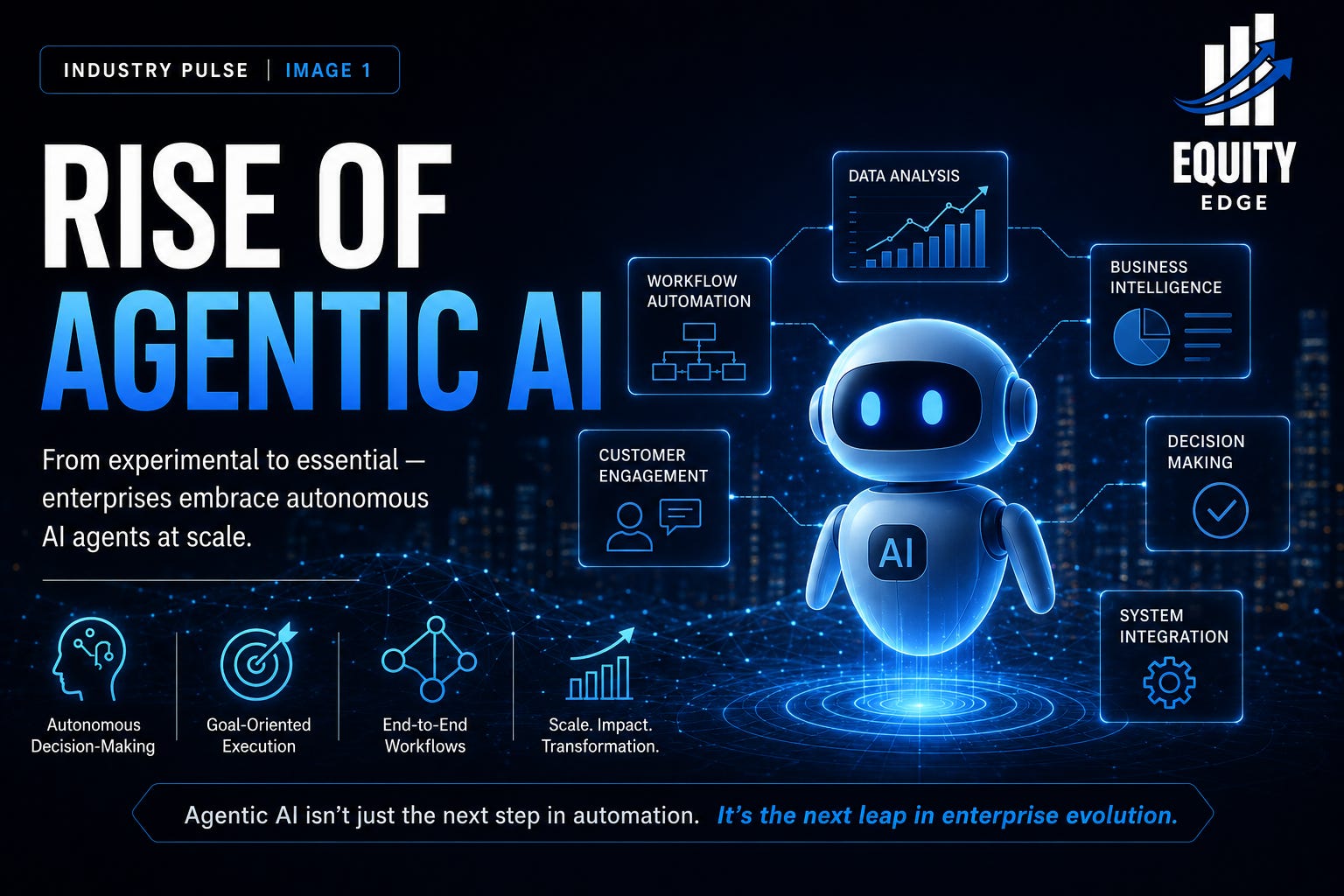

1. Rise of Agentic AI:

The Indian technology and enterprise landscape has officially moved past the experimental generative AI phase, entering full-scale production with Agentic AI. Rather than relying on simple, reactive chat interfaces that require constant human prompting, companies are rapidly transitioning to autonomous digital agents.

These specialized frameworks integrate an internal reasoning layer to independently plan, leverage enterprise APIs, and execute multi-step workflows across business infrastructure without needing a human operator behind every single action.

This operational shift is driven by three uniquely Indian market dynamics:

The Service-to-Product Scale: For decades, the Indian IT sector scaled linearly based on headcount and labor arbitrage. Agentic AI is breaking this historical link, forcing a hard pivot toward non-linear growth models driven by digital coworkers working alongside human engineers.

The Vernacular Frontier: Unlike Western markets relying on English-dominated models, Indian organizations face a deeply fragmented linguistic landscape. The rise of agentic networks locally is defined by the deployment of multilingual, voice-enabled agents capable of navigating dozens of regional Indian languages.

GCC Value Inversion: India’s network of over 1,600 Global Capability Centers (GCCs) is transforming. Historically viewed as back-office operational cost centers, these hubs are evolving into the primary global engine for agent orchestration, building the core autonomous systems used by their global parent organizations.

Recent Major News Related to the Advancement of Agentic AI

1. India-Specific News

Massive Agentic Scale Across Indian IT Majors: Microsoft announced that leading IT giants Infosys, TCS, and Wipro have collectively scaled their Microsoft 365 Copilot and custom agentic frameworks to over 300,000 employees. This rollout marks one of the largest and fastest transitions from tool-level AI to an enterprise-wide agentic operating model globally.

Wipro Reports Quantifiable Savings via Agent Deployment: Wipro revealed that its active deployment of over 29,000 employee-created custom AI agents and 60 enterprise-grade agentic platforms has saved more than 250,000 full-time equivalent (FTE) days per quarter. Notably, its internal appraisal agent reduced performance review workloads by nearly 70% by tracking evidence-based goals automatically.

Infosys Topaz Achieves Deep Engagement: Infosys expanded Copilot and agentic access to 115,000 seats across delivery, engineering, and corporate functions under its Infosys Topaz ecosystem, documenting a massive 91% monthly active usage rate as these tools evolve into core workflow components.

TCS Records Substantial Efficiency Gains: TCS integrated custom agentic intelligence across more than 100,000 associates, reporting that 86% actively use AI in daily work to secure 20% to 25% productivity improvements in research and content production, alongside a 25% to 35% reduction in selective technical work-cycle times.

Rise of Indian Full-Stack Agent Builders: Homegrown platforms are scaling rapidly to close the enterprise integration gap. Startups like Onetab.ai launched an Enterprise AI Agentic Solutions suite capable of connecting with over 150 legacy business tools, allowing Indian firms across healthcare and banking to cut operational costs by roughly 40% and save up to 80% on manual task execution.

Multilingual Vernacular Agents Scale Across Public Infrastructure: Conversational agent providers like CoRover and Yellow.ai have scaled autonomous, voice-enabled agents across Indian Railways (IRCTC), national airports, and state government portals, supporting over 135 regional languages to facilitate transactions and customer support for millions of non-English speaking citizens.

2. Global-Specific News

Global Enterprise Software Pivot to Agents: Enterprise software giants have fundamentally shifted from utility software to autonomous platforms. Salesforce launched its massive Agentforce initiative, while ServiceNow deployed its Autonomous Workforce platform, signaling a market transition from traditional SaaS “systems of record” to autonomous “systems of decisions.”

Developer Ecosystem Standardizes on Open Protocols: The global developer community has broadly adopted Anthropic’s Model Context Protocol (MCP) alongside specialized Agent Client Protocols, allowing engineers to build safer, desktop-level computer execution sandboxes for autonomous software agents.

Inference Costs Plunge Globally: A sustained 95% drop in frontier model token inference costs over the past few years has reshaped tech economics. It is now financially viable for enterprises to let multiple background agents run continuous, iterative loop conversations to solve a single problem.

Market Penetration Surges: Gartner updates indicate that 40% of enterprise applications will embed task-specific AI agents by the end of 2026, up from under 5% a year earlier, highlighting the steepest adoption curve of any emerging technology tracked..

Why Does It Matter

The rapid adoption of agentic frameworks completely resets the unit economics of the software and IT services sectors, shifting the paradigm from productivity amplification to task delegation.

For decades, the global software industry operated as a “system of record” that still required human labor to prompt the tool, process the information, and transfer it manually. Agentic AI turns software into a “system of decisions,” meaning companies are deploying an independent digital workforce rather than just buying software utilities to help employees work a bit faster.

For the $300 billion Indian IT sector, this transformation challenges its historical foundations. For decades, the industry scaled linearly based on head-count and labor arbitrage, more project revenue strictly required hiring more engineers. Agentic AI breaks this linear link, forcing a hard shift toward non-linear growth models driven by digital coworkers.

Financially, this shift is accelerated by two distinct metrics.

First, a dramatic 95% drop in global LLM inference costs has made running continuous, iterative agent reasoning loops highly cost-effective for large organizations.

Second, internal business metrics have proven massive financial viability: early production data shows that delegating routine operational tasks to autonomous agents reduces manual workflow cycles by up to 80% and slashes operational costs by roughly 40%.

The focus of corporate leadership is moving away from basic model performance metrics like context windows or speed, landing entirely on real-time business outcomes.

Who Is Doing What

The Indian agentic landscape has quickly organized into specialized execution layers, moving beyond traditional software maintenance into high-value autonomous systems:

Zepto (Quick-Commerce Automation):

Leading in real-time operational agent deployment, Zepto built an in-house multi-agent framework called Zap to handle complex customer support loops.

When an issue occurs, Zap automatically coordinates specialized verification agents: one authenticates order context, another leverages computer vision to analyze uploaded product photos for fraud or spoilage, and a final policy engine issues instant resolution.

This custom infrastructure has slashed average support resolution times by 75%, shifting human operators entirely to edge-case oversight.

Amazon India (Context-Driven Commerce):

Implementing agentic memory frameworks across emerging markets, Amazon has shifted its local consumer engine away from generic purchase histories.

Its new agents maintain adaptive context models (tracking localized budget preferences or regional family shopping habits).

They utilize localized natural language processing to let users query their own inferred profiles directly via features like Quick Summary and the Rufus shopping assistant layer.

Sarvam AI (Sovereign Full-Stack Agent Frameworks):

Operating as a cornerstone of domestic developer infrastructure, Sarvam AI has scaled open, highly optimized enterprise engines like Samvaad and Arya.

Instead of forcing companies to route data through generic foreign APIs, Sarvam partners directly with major Indian financial and insurance institutions to build production-ready, air-gapped agent networks running on sovereign compute infrastructure.

Bolna AI & Homegrown Startups (Vernacular Voice Automation):

Dominating the high-volume voice call stack, startups like Bolna AI have deployed multilingual, conversational voice agents across thousands of inbound and outbound customer calls every minute.

These localized voice agents are specifically trained to handle complex accents and mixed dialects (such as “Hinglish”) across over ten regional Indian languages, completely automating e-commerce cart abandonment checks, cash-on-delivery (COD) confirmations, and rapid applicant screening.

Second-Order Effects

The rapid migration toward non-deterministic background agents is triggering structural changes across the domestic market landscape:

1. The Disruption of Time-and-Material Pricing

As autonomous software agents take over heavy operational workloads like code testing, system compliance, data analytics, and L1 helpdesk support, the traditional IT billing architecture is eroding. The time-and-material contract structure, which bills clients directly for human hours logged, is giving way to strict, value-based or outcome-based pricing models. Companies are no longer being paid for the size of the team they provide, but for the specific speed, accuracy, and operational outcomes their agent networks deliver.

2. The Acceleration of the “Frontier Firm” GCC

India’s network of over 1,600 Global Capability Centers (GCCs) is experiencing a severe value inversion. Historically utilized as back-office execution centers for Western parent corporations, these GCCs are capitalizing on their vast pools of technical talent to become the absolute core engineering engine for global agent roadmaps. The architecture, security guardrails, and data pipelines powering global enterprise agent networks are increasingly being built and managed directly out of India.

3. Radical Restructuring of Corporate L&D and Hiring

Because entry-level cognitive tasks are easily automated by agentic loops, the traditional hiring and training pipeline for Indian tech graduates is changing completely. According to recent enterprise insights, an overwhelming 92% of technology executives state that future job competitiveness depends heavily on agent lifecycle management and human-agent collaboration. Corporate Learning and Development (L&D) budgets are moving away from teaching basic language syntax, focusing instead on advanced context engineering, multi-agent orchestration, and strict governance oversight.

Key Question

As corporate software evolves into a decentralized network of autonomous digital workers, the ultimate operational challenge shifts from enabling capability to maintaining predictable governance:

As hundreds of non-deterministic background agents begin independently executing transactions, querying financial ledgers, and altering customer records across Indian corporate systems, how will organizations build an “operating system for AI” that successfully enforces deterministic compliance guardrails, API security controls, and real-time auditability without choking the very autonomy that makes them valuable?

Sources: Microsoft Asia Newsroom, TechGig IT Case Studies, AI HR Daily, The Economic Times Tech, Zepto Data Science Logs, AWS Machine Learning Bulletins, Sarvam AI Engineering Logs, Bolna AI Developer Stack, Onetab.ai Whitepapers, EY India AI Survey, NASSCOM Tech Tracker, and Gartner Forecasting.

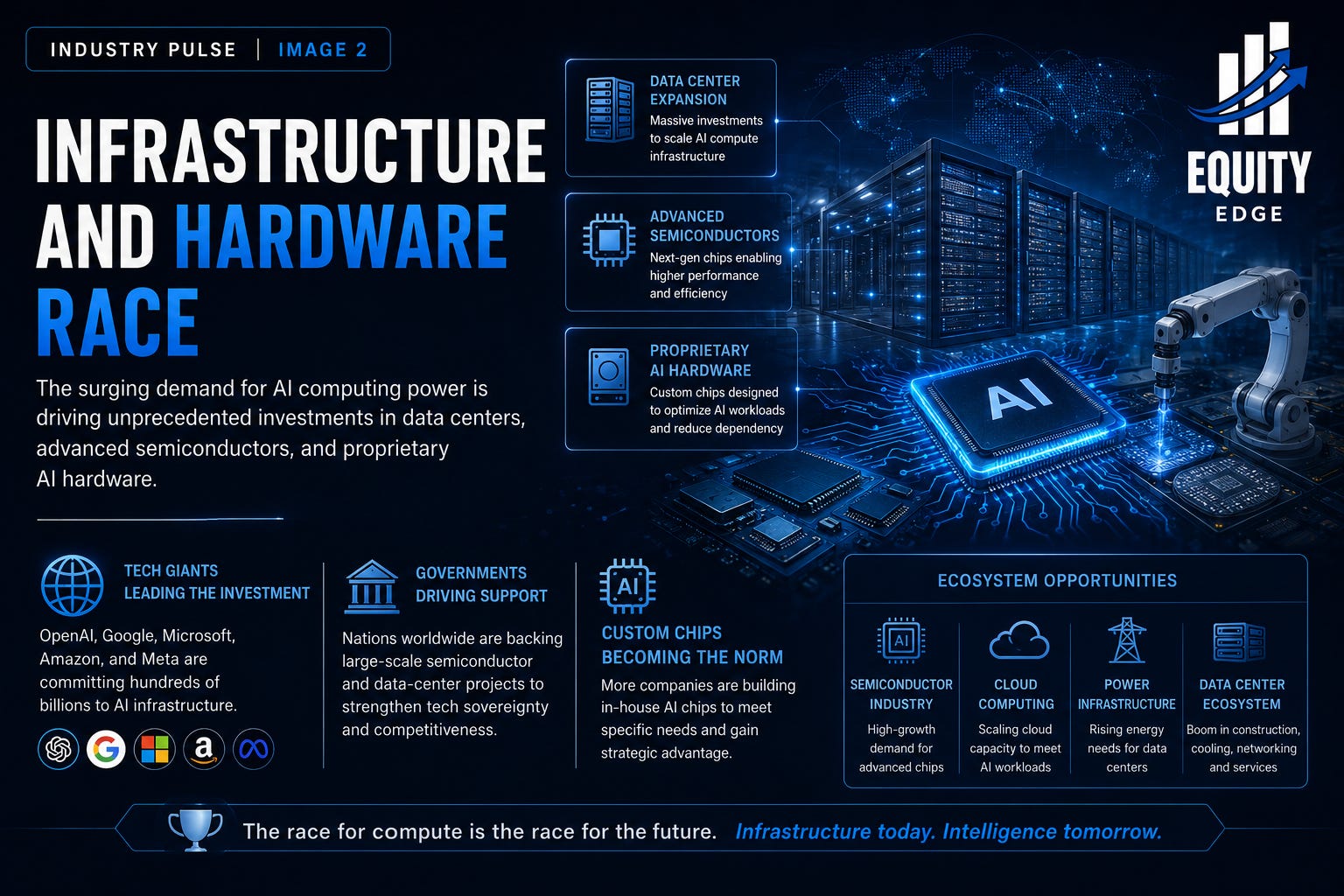

2. Infrastructure and Hardware Race:

The surging demand for AI computing power is driving unprecedented investments in data centers, advanced semiconductors, and proprietary AI hardware.

Technology giants such as OpenAI, Google, Microsoft, Amazon, and Meta are collectively committing hundreds of billions of dollars to expand AI infrastructure, while governments worldwide are supporting large-scale semiconductor and data-center projects to strengthen technological competitiveness.

At the same time, companies are increasingly developing custom AI chips to reduce reliance on third-party suppliers and optimize performance for AI workloads.

This global race for computing capacity is reshaping the technology landscape and creating significant opportunities across the semiconductor, cloud computing, power infrastructure, and data-center ecosystems.

Recent Major News related to advancement of Infrastructure and Hardware:

1. India Specific News:

India Targets $200 Billion in AI Data Center Investments: The Government of India announced its ambition to attract up to $200 billion in AI data center investments as part of its strategy to position India as a global AI hub. The initiative is backed by tax incentives, data-center policies, and public AI computing infrastructure. Major global technology companies have already announced investments, including Google ($15 billion), Microsoft ($17.5 billion), and Amazon ($35 billion by 2030).

Reliance and Adani Announce Over $210 Billion AI Infrastructure Plans: India’s two largest conglomerates announced combined investments of approximately $210 billion in AI infrastructure.

Reliance Industries: ~$110 billion

Adani Group: ~$100 billion

The investments include hyperscale AI data centers, renewable-powered computing campuses, cloud infrastructure, and AI services. Reliance’s Jamnagar AI campus alone is expected to add more than 120 MW of data-center capacity in its initial phase

IndiaAI Mission Expands National GPU Compute Infrastructure: At the India AI Impact Summit 2026, the government announced plans to expand the IndiaAI Compute Portal by adding over 20,000 GPUs to the existing pool of 38,000 GPUs. The initiative aims to provide affordable computing resources for startups, researchers, and enterprises while supporting the development of sovereign Indian AI models.

India Emerges as a Global AI Data Center Destination: Global cloud providers accelerated their India expansion during the year.

Key announced investments include:

Microsoft: $17.5 billion.

Google: $15 billion.

Amazon: $35 billion (by 2030).

India’s cloud data-center capacity has reached approximately 1,280 MW and is projected to grow 4–5 times by 2030, driven by AI workloads and cloud adoption.

Microsoft-Led Undersea Cable Strengthens India’s AI Connectivity: Microsoft, Lightstorm, Tata Communications, and other partners announced the I-2SEA submarine cable connecting India, Malaysia, and Singapore. The 3,600-km cable is designed to support the rapid expansion of AI and cloud infrastructure by providing higher international bandwidth and improved connectivity for hyperscale data centers.

2. Global Specific News:

Stargate: The Largest AI Infrastructure Project Ever Announced: OpenAI, SoftBank, Oracle, and partners launched the Stargate Project, with plans to invest up to $500 billion in AI infrastructure over four years. The initiative aims to build massive AI data centers and computing capacity across the United States, making it one of the largest technology infrastructure projects in history.

Big Tech’s AI Capital Expenditure Surge: Microsoft, Amazon, Alphabet, Meta, and Oracle collectively committed hundreds of billions of dollars toward AI infrastructure. Industry estimates suggest aggregate AI-related capital expenditure is approaching $700 billion, while major hyperscalers continue expanding data centers, networking infrastructure, and GPU clusters.

Nvidia’s Blackwell AI Chip Boom: Demand for Nvidia’s Blackwell GPUs surged as cloud providers and AI companies raced to secure computing power. Nvidia’s data-center business reached record levels, with the company reporting massive growth driven by AI infrastructure spending and long-term demand for advanced AI accelerators.

AI’s Growing Demand for Power and Semiconductor Capacity: The rapid expansion of AI data centers has triggered unprecedented demand for electricity, memory chips, and power infrastructure. Companies such as Micron reported billions of dollars in long-term customer commitments, while infrastructure investors committed tens of billions to energy projects designed specifically for AI workloads.

(Sources: intuitionlabs.ai, futurumgroup.com, ciodive.com, reuters.com.)

Why Does It Matter?

AI infrastructure has become the foundational layer of the AI economy. As AI models become larger and autonomous AI agents execute increasingly complex, multi-step workflows, computing power is emerging as a key competitive advantage rather than just a technological resource.

Organizations with access to scalable compute, advanced semiconductors, and high-performance data centers will be better positioned to develop, deploy, and commercialize next-generation AI applications.

The infrastructure race also extends beyond technology companies. It is reshaping industries such as semiconductors, cloud computing, energy, telecommunications, and industrial real estate by creating sustained demand for GPUs, networking equipment, power systems, cooling technologies, and digital infrastructure. Consequently, AI infrastructure is evolving into a critical enabler of innovation, productivity, and economic growth.

At a strategic level, control over AI infrastructure is increasingly linked to technological leadership, digital sovereignty, and national competitiveness. Countries and enterprises that establish robust AI compute ecosystems are likely to accelerate AI adoption, attract high-value investments, strengthen domestic innovation, and secure long-term advantages in the global digital economy.

Who Is Doing What?

The AI infrastructure race is being driven by governments, hyperscale cloud providers, semiconductor manufacturers, and digital infrastructure companies, each investing aggressively to secure control over the computing backbone of the AI economy.

Government Initiatives (Building National AI Compute)

Governments are increasingly treating AI infrastructure as strategic national infrastructure, similar to energy and telecommunications. India aims to attract up to US$200 billion in AI data center investments while expanding the IndiaAI Compute Portal by adding over 20,000 GPUs to its existing 38,000-GPU pool, enabling affordable access to AI compute for startups, researchers, and enterprises developing sovereign AI models.

Globally, the United States is supporting large-scale AI infrastructure through initiatives such as the US$500 billion Stargate Project, while countries including South Korea, the UAE, and Singapore are accelerating investments in semiconductor manufacturing, AI data centers, and digital infrastructure to strengthen technological competitiveness.

Microsoft, Amazon, Google & OpenAI (Building Hyperscale AI Infrastructure)

Global hyperscalers are investing hundreds of billions of dollars to expand AI computing capacity through hyperscale data centers, cloud platforms, proprietary AI chips, and high-performance networking.

Microsoft has announced approximately US$17.5 billion in investments in India while rapidly expanding AI-enabled cloud infrastructure globally.

Amazon plans to invest US$35 billion in India by 2030 and has committed an additional US$1 billion to accelerate enterprise deployment of agentic AI.

Google has announced approximately US$15 billion in investments to strengthen India’s AI and cloud ecosystem while continuing to develop its custom TPU chips.

OpenAI, together with SoftBank and Oracle, is leading the Stargate Project, a US$500 billion initiative to build one of the world’s largest AI computing ecosystems across the United States.

These investments are creating the large-scale computing capacity required to train and deploy next-generation foundation models.

Nvidia, AMD, TSMC & Memory Manufacturers (Powering the AI Compute Stack)

Semiconductor companies are rapidly expanding production to meet unprecedented demand for AI accelerators, memory, and advanced chip packaging.

Nvidia continues to dominate the AI accelerator market through its Blackwell GPU platform, with record growth in its Data Center business driven by hyperscale AI deployments.

AMD is expanding its Instinct AI accelerator portfolio to compete in enterprise AI workloads, while Micron and SK Hynix are significantly increasing production of High-Bandwidth Memory (HBM)—a critical component required for modern AI servers.

Meanwhile, TSMC is investing tens of billions of dollars in advanced semiconductor fabrication and packaging technologies to support growing demand from customers including Nvidia, AMD, Apple, and Broadcom.

Reliance, Adani & Infrastructure Providers (Building the Physical Backbone)

Infrastructure companies are building the physical foundation required to support AI at scale, including data centers, power generation, cooling systems, and high-speed connectivity.

In India, Reliance Industries and Adani Group have announced combined AI infrastructure investments of approximately US$210 billion. Reliance’s proposed AI campus at Jamnagar is expected to deliver over 120 MW of initial data center capacity, supported by renewable energy and cloud infrastructure.

Globally, companies such as Equinix and Digital Realty continue expanding hyperscale data center capacity, while Bloom Energy and Brookfield have partnered on US$25 billion worth of power infrastructure projects dedicated to AI data centers. At the same time, international connectivity is being strengthened through projects such as the I-2SEA submarine cable, led by Microsoft and its partners, enabling faster cross-border movement of AI data.

Second-Order Effects

The global AI infrastructure race is expected to reshape multiple industries well beyond semiconductors and cloud computing. As computing power becomes a strategic resource, its impact will extend across energy, real estate, telecommunications, and enterprise technology.

1. AI Compute Becomes the New Strategic Commodity:

Just as oil fueled the industrial economy and cloud computing powered the digital economy, AI compute is emerging as the defining strategic resource of the AI era. Governments and enterprises are investing hundreds of billions of dollars in GPUs, custom AI chips, and hyperscale data centers to secure long-term computing capacity. This shift is expected to intensify competition for semiconductor manufacturing, advanced packaging, and High-Bandwidth Memory (HBM), creating sustained demand across the global semiconductor ecosystem.

2. Data Centers Evolve into Critical National Infrastructure:

The rapid deployment of AI models is transforming data centers from traditional IT facilities into large-scale digital utilities. AI workloads require significantly higher rack densities, advanced liquid-cooling systems, reliable fiber connectivity, and uninterrupted power supply, driving increased investments in industrial real estate, construction, cooling technologies, and digital infrastructure. As a result, hyperscale AI campuses are expected to become a major asset class over the next decade.

3. Power Infrastructure Emerges as the Next Bottleneck:

Unlike conventional cloud workloads, AI data centers consume substantially more electricity due to continuous GPU utilization and high-performance computing requirements. This is accelerating investments in power generation, renewable energy, battery storage, transmission infrastructure, and grid modernization. Access to reliable and low-cost electricity is increasingly becoming a key factor in determining where future AI data centers will be built.

4. High-Speed Connectivity Becomes Mission-Critical:

As AI models process and exchange massive volumes of data across regions, demand for low-latency digital connectivity is increasing rapidly. This is driving investments in high-capacity fiber networks, AI-optimized networking equipment, edge computing infrastructure, and submarine cable systems such as the India–Southeast Asia connectivity corridor. Telecommunications infrastructure is therefore evolving from a support service into a strategic enabler of AI deployment.

5. Faster AI Adoption Across Enterprises:

Greater availability of AI computing infrastructure is expected to reduce inference costs and improve access to advanced AI models, enabling wider adoption across banking, healthcare, manufacturing, retail, logistics, and public services. As infrastructure constraints ease, enterprises are likely to accelerate investments in AI-powered software, autonomous agents, cybersecurity platforms, and cloud-native applications, expanding the addressable market for enterprise AI solutions.

Key Question:

The defining question is no longer whether AI adoption will continue, but which countries and companies will control the infrastructure powering the AI economy.

Will AI compute become concentrated among a handful of global hyperscalers, or will governments and domestic enterprises succeed in building sovereign AI infrastructure?

At the same time, can electricity generation, semiconductor manufacturing, and data-center capacity expand quickly enough to meet surging AI demand without creating supply bottlenecks?

The answers to these questions will determine the next generation of winners across semiconductors, cloud computing, energy, telecommunications, and digital infrastructure.