On February 12, 2026, the National Statistical Office (NSO), under the Ministry of Statistics and Programme Implementation (MoSPI), quietly did something that matters enormously for India’s economic conversation: it launched a revised Consumer Price Index (CPI) series with a new base year of 2024.

This may sound like statistical housekeeping. It is not.

It is an attempt to update the mirror through which India looks at inflation.

For over a decade, we were measuring today’s price changes using a 2012 consumption template. But India in 2026 is not India in 2012. Back then, VCR players still had a statistical afterlife. Today, households pay for OTT subscriptions, data plans, e-commerce deliveries, and rural house rent. The economy has urbanised, digitised, and professionalised. The CPI had to catch up.

This reset anchors the index in the Household Consumption Expenditure Survey (HCES) 2023–24, which captures how Indians actually spend today not how they used to.

Let’s unpack what changed, and more importantly, why it matters.

The Base Year Shift: Updating the Economic Photograph

The base year has moved from 2012 to 2024.

That means the weights assigned to different items now reflect current consumption patterns. Think of CPI as a weighted basket. If households are spending more on transport, housing, and health and relatively less on food then the inflation index must reflect that.

Without this update, policymakers would be reacting to a distorted picture.

And in a country growing at 7.3% to 7.5% real GDP in recent years, with per capita income nearly doubling since 2012, distortion compounds quickly.

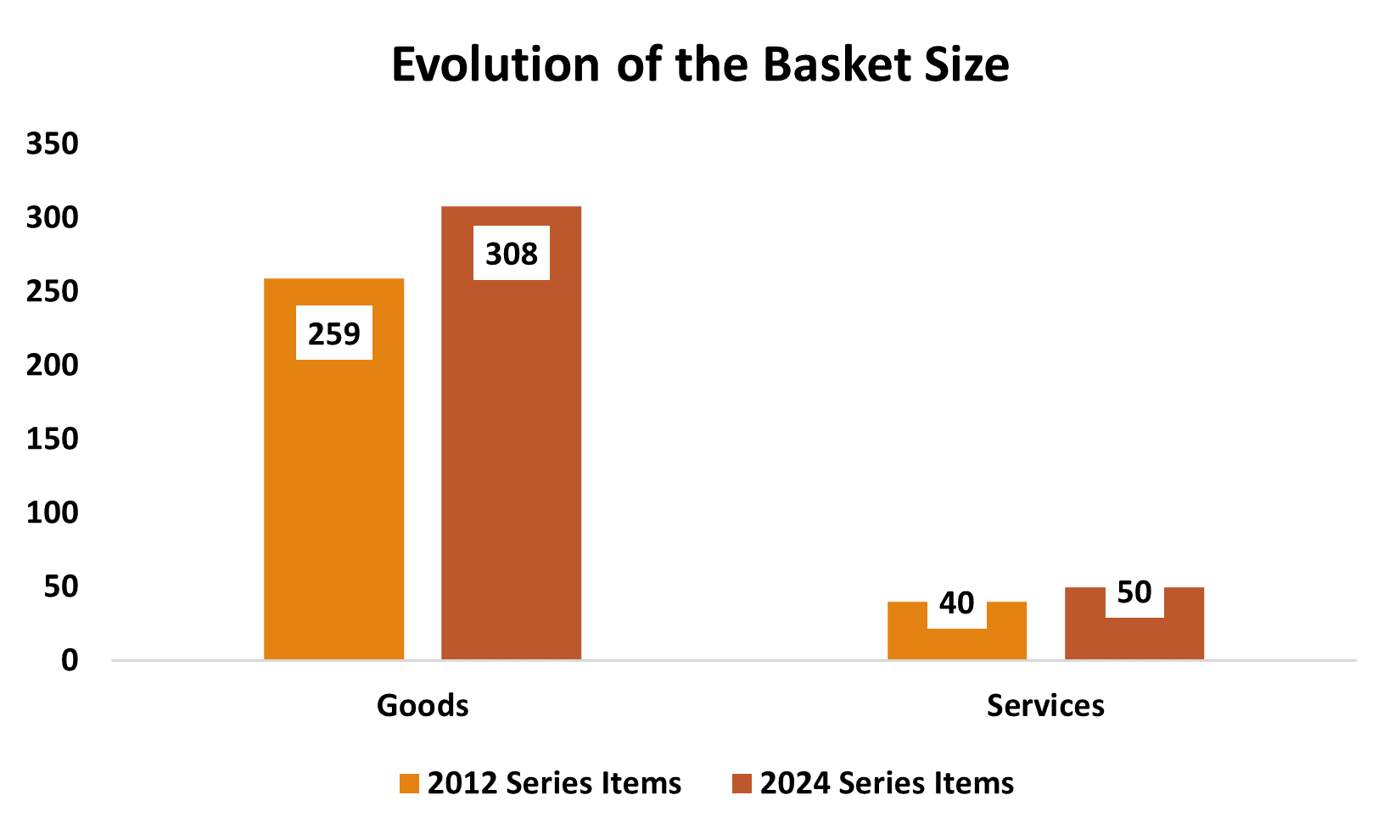

The Basket Gets Bigger And More Modern

The consumption basket has expanded from 299 to 358 items at the all-India level.

This matters because modern India is increasingly service-driven.

Obsolete items like VCR/VCD players and radios have been removed. In their place:

OTT streaming subscriptions.

Smartphones.

E-commerce pricing.

Rural house rent (included for the first time).

The inclusion of rural house rent is particularly important. It corrects a long-standing blind spot. Housing costs are real in rural India too, and now they are statistically acknowledged.

In short: the CPI basket now looks like your household budget, not your parents’.

The January 2026 Print: Signal vs Noise

The first reading under the new series showed January 2026 retail inflation at 2.75%, compared with 1.33% in December 2025 under the old 2012-based series.

Cue alarm? Not really.

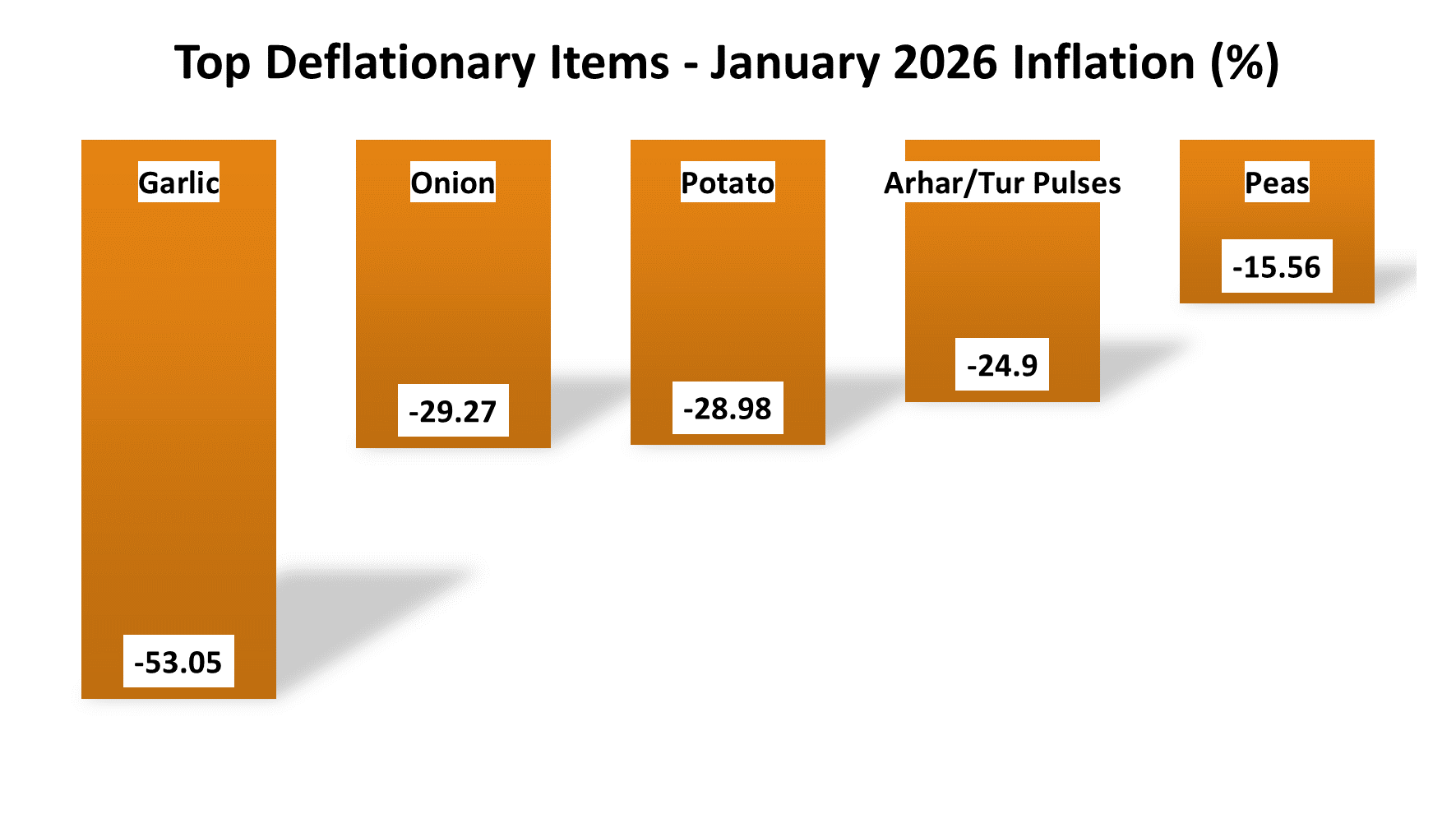

The NSO and experts have clarified: this is not a sudden inflation spike. It is a statistical reset. Several factors explain the difference.

1. Weight Recalibration

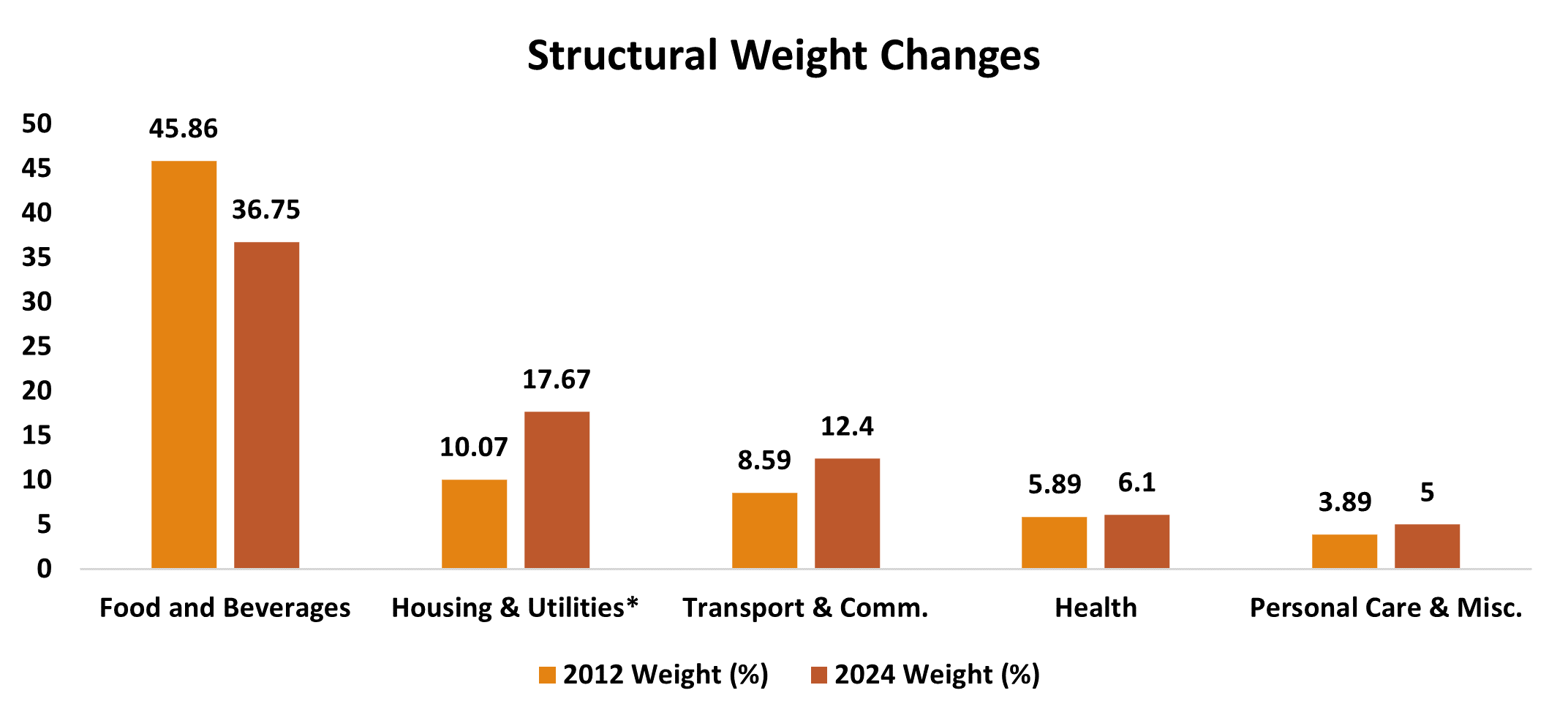

The most dramatic structural shift is in the weight of Food and Beverages:

2012 series: 45.86%.

2024 series: 36.75%.

Food remains the largest component but it no longer dominates the index the way it once did.

At the same time, core categories gained prominence:

Housing, Water, Electricity & Gas: 16.89% → 17.67%.

Transport: 6.39% → 8.80%.

Health: 5.9% → 6.1%.

Information & Communication: 2.2% → 3.6%.

Core CPI (excluding food and fuel) now carries a weight of 57.9%, up from 47.3% earlier.

This means headline inflation is structurally less sensitive to tomato and onion shocks. That is a major change for monetary policy.

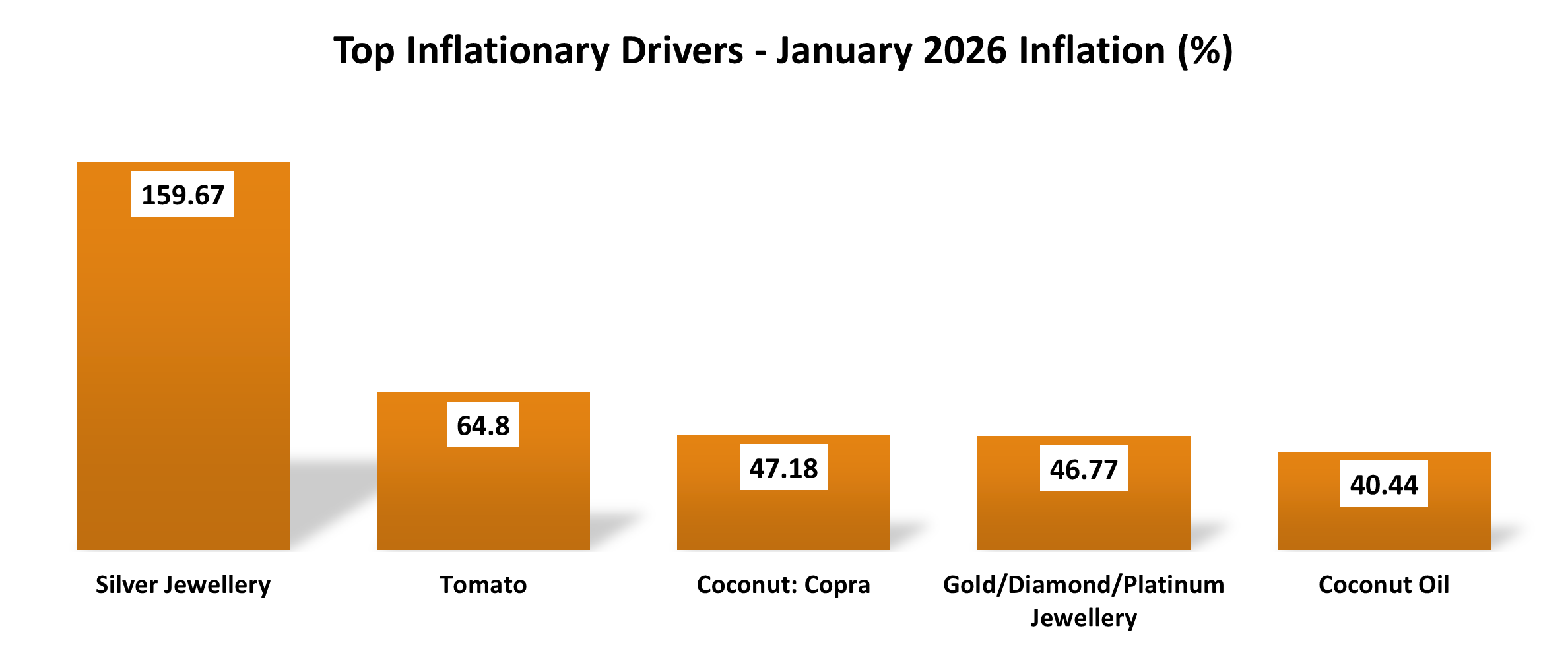

2. The “Bullion Effect”

A significant part of the January uptick came from a sharp surge in gold and silver jewellery prices.

Under the new weighting diagram, precious metals have a stronger impact. So when gold rallies, it shows up more clearly in inflation.

This is not price instability it is measurement visibility.

3. Methodological Improvements

The new series moves from manual pen-and-paper collection to a tablet-based system.

It also adopts a short-term, chain-based approach to measuring price changes.

Translation: fewer errors, less bias, better accuracy.

4. Reclassification Effects

Restaurant meals were moved out of the food group into a standalone service category called Restaurants and Accommodation Services (with a 3.3% weight).

This reclassification mathematically lowers the food weight while raising services.

Nothing changed in your plate. The spreadsheet changed.

The first headline under the new series January 2026 inflation at 2.75% triggered immediate commentary.

It was higher than December 2025’s 1.33% under the old series. It also exceeded market expectations of roughly 2.4%.

But much of this difference contains statistical noise rather than pure price acceleration.

Methodological Effects

Estimates suggest a marginal bias of 20–30 basis points under the new methodology. In months where food inflation is high, the new structure may actually print lower than the old series by a similar margin.

Measurement changes alter arithmetic outcomes. That is not manipulation it is recalibration.

Structural vs Cyclical Forces

Structurally, food weight fell from 45.86% to 36.75%. Core components (excluding food and fuel) rose to 57.9%.

Cyclically, January was heavily influenced by the bullion effect.

Silver jewellery inflation hit 159.67%. Gold and diamond jewellery rose 46.77%.

This surge in precious metals significantly influenced the headline number.

In other words, the inflation spike was less about vegetables and more about vaults.

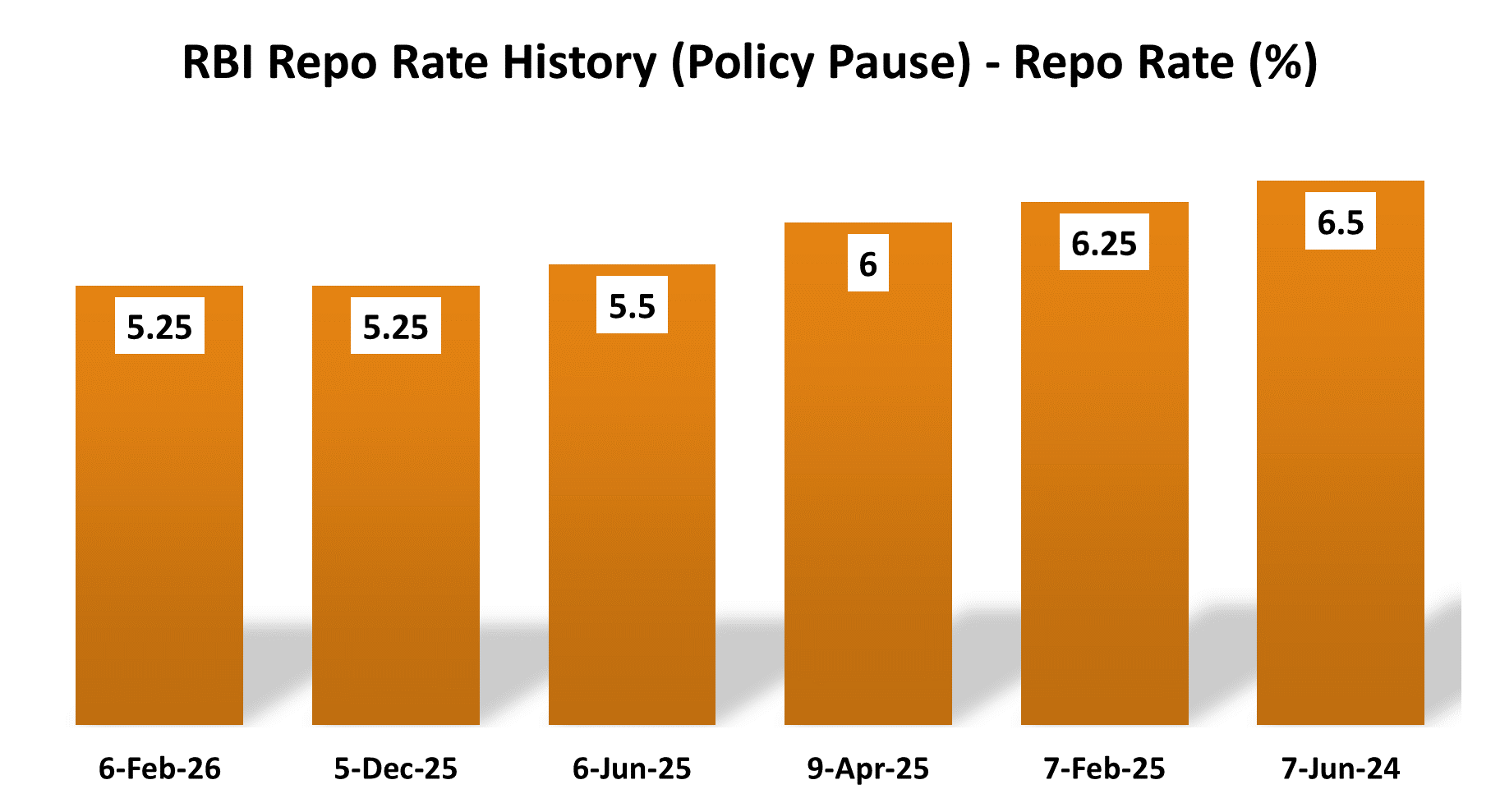

The RBI’s Policy Stance

At its February 6, 2026 meeting, the RBI maintained the repo rate at 5.25% and retained a neutral stance.

Governor Sanjay Malhotra described the approach as “pre-emptive and cautious.”

Markets interpret this as an extended pause. Analysts suggest that the rate-cut cycle may have ended, with policymakers waiting until April 2026 to integrate full-year FY27 projections under the new CPI structure.

The RBI is adapting not just to price movements, but to a new measurement regime.

That is prudent central banking.

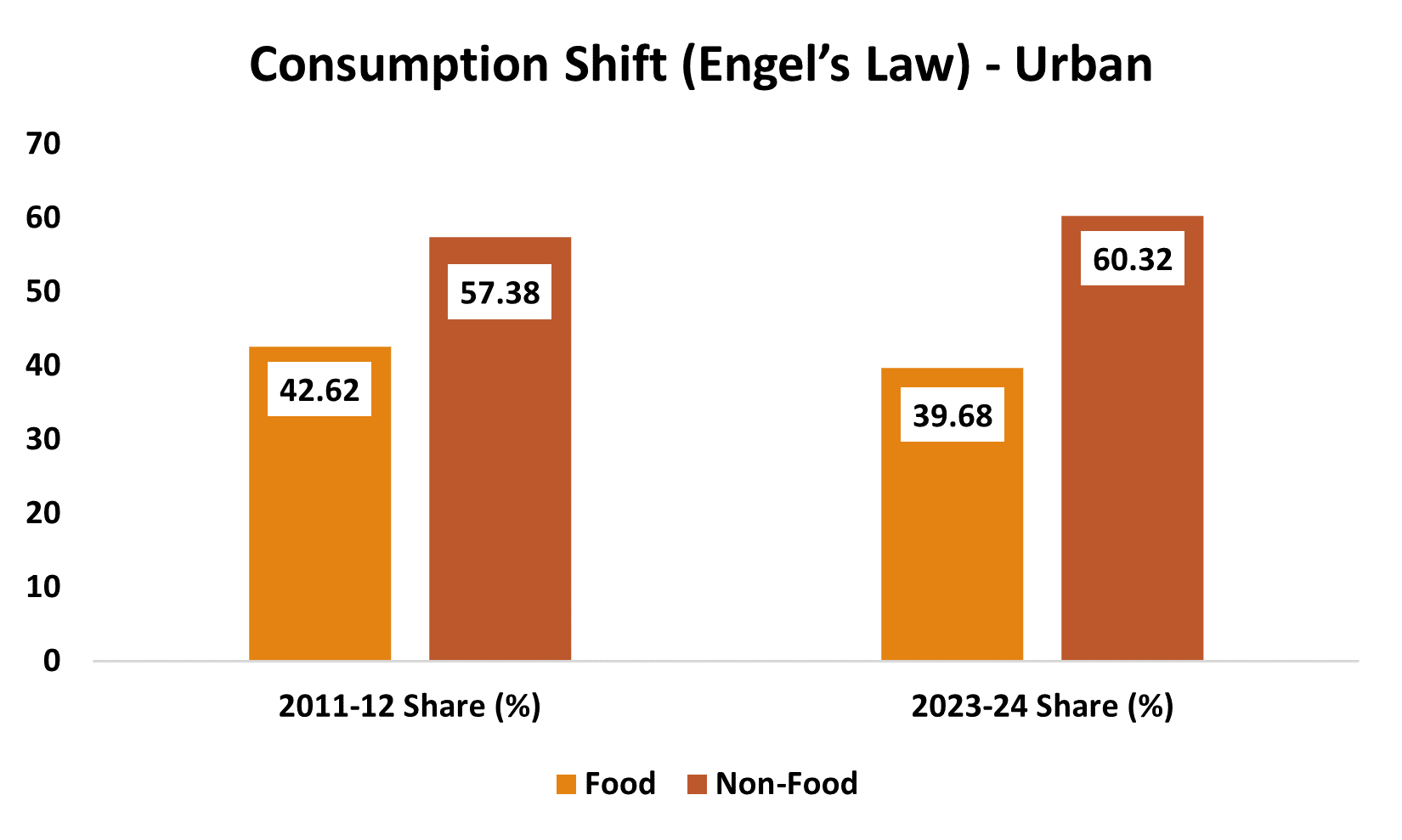

The Deeper Story: India’s Consumption Upgrade

The CPI revision is not just technical. It reflects something larger.

The HCES 2023–24 shows that household consumption has nearly doubled over the past decade. Rising incomes and improved living standards have changed spending patterns.

Within food itself, there is a shift:

From cereals and basic staples → toward dairy, fruits, vegetables, fish, and meat.

This is a move from “survival calories” to “nutritional calories.”

And outside food, spending on mobility, health, housing, communication, and services has expanded.

Economists call this Engel’s Law: as incomes rise, the share of income spent on food declines, even if absolute food spending increases.

That is precisely what India is experiencing.

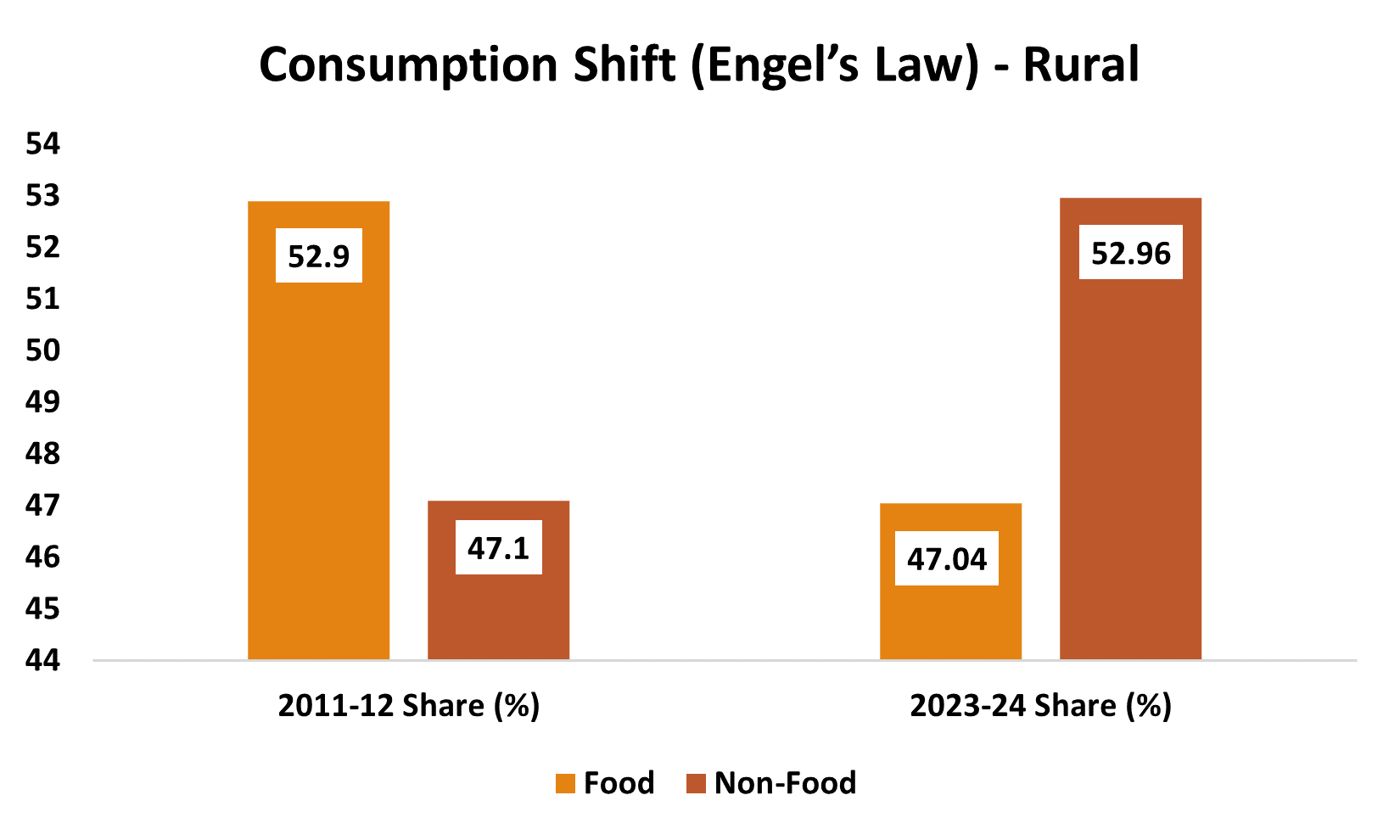

Rural vs Urban: The Divergence That Is Narrowing

The data shows an important shift in rural India.

Rural households are diversifying consumption faster than before.

They are spending more on non-food items, which indicates rising discretionary power.

The inclusion of rural house rent strengthens this narrative. Rural India is no longer statistically invisible in housing costs.

Meanwhile, services expansion including professional fees such as babysitters and domestic attendants reflects the growing formalisation and professionalisation of labour markets.

This is what middle-income transition looks like in numbers.

The Digital Turn: When CPI Meets the Smartphone

If the earlier revision was about acknowledging that India has grown richer, this next shift is about acknowledging that India has gone digital.

The 2024-based CPI does something quietly revolutionary: it begins to measure the Indian household as it actually exists in 2026 phone in hand, subscription auto-renewing, groceries delivered, rent transferred online.

The National Statistical Office (NSO) has expanded the basket not merely in size, but in character. It now captures digital goods and services that were previously invisible or underrepresented.

This is not cosmetic. This is structural.

What Enters the Digital Basket

Several “new-age” items are now formally part of the inflation calculus.

OTT Subscriptions

Platforms like Amazon Prime Video, Netflix, Jio Hotstar, SonyLiv, YouTube Premium, and Zee5 are now directly tracked through their service-provider websites.

This acknowledges that entertainment consumption has shifted decisively from cinema halls and cable TV toward streaming subscriptions. Inflation now includes binge watching.

Telecom Data

Data-heavy prepaid and postpaid plans are explicitly included. In a country where mobile data is the bloodstream of commerce, education, payments, and social life, excluding telecom pricing would have been anachronistic.

E-commerce Pricing

For the first time, prices from online platforms in 12 major towns (population above 25 lakhs) are treated as an additional market alongside physical shops.

This matters because the Indian consumer does not shop in just one marketplace anymore. She arbitrages across Amazon, Flipkart, and the neighbourhood kirana.

Digital Accessories & Goods

Smartphones, fitness trackers, wireless earphones, pen drives, external hard disks — these are no longer luxury outliers. They are mainstream consumption items.

In effect, CPI now tracks not just food, fuel, and fabric but firmware.

The Analog Exit

Modernisation also means subtraction.

The CPI basket has removed items that belong to another era:

VCR, VCD, DVD players and hiring charges.

Radios and tape recorders.

Audio/video cassettes.

Horse-cart fares (tonga).

Coir rope.

Second-hand clothing.

Cassette tapes.

The CPI is no longer a museum. It is a living document.

From Ghost Index to Living Document

If we are being honest, the old 2012-based CPI had become something of a ghost index.

It was still alive on paper, still guiding monetary policy, still cited in headlines but it was tracking a version of India that was fading. A basket dominated by food expenditure made sense for a lower-income economy. It made less sense for a country that had seen per capita income nearly double, urbanise rapidly, digitise at scale, and formalise consumption patterns.

Over the last decade, India changed. The CPI had not kept pace.

The 2024 rebasing is not cosmetic housekeeping. It is an overdue recalibration of the country’s inflation compass.

What Changed in the Real Economy

Several structural transformations since 2012 made the update inevitable.

The Smartphone Economy

The digital revolution was not incremental it was transformative. Smartphones became ubiquitous. Fitness trackers, wireless earphones, pen drives, external hard disks these are now everyday goods.

If inflation does not track the tools through which Indians work, communicate, and consume, it misses the point.

The Data Explosion

India became one of the world’s largest consumers of mobile data. Streaming platforms became mainstream entertainment.

The new CPI explicitly includes data-heavy telephone plans and OTT subscriptions like Netflix, Amazon Prime, and Disney+ Hotstar. That is not a niche adjustment; it is acknowledging that a significant part of household expenditure has moved online.

Urbanisation and Market Expansion

Urban India expanded rapidly. Consumption patterns shifted toward services, housing, transport, and organised retail.

The new CPI now covers 1,395 markets across 434 towns and incorporates e-commerce prices in large cities. That inclusion alone changes how we interpret price competition and pricing power in urban India.

The household no longer shops in one marketplace. Inflation measurement cannot either.

Post-COVID Health Priorities

The pandemic altered spending behaviour. Health and wellness moved from discretionary to essential.

The weight for health has increased from 5.9% to 6.1%. That may look like a marginal change, but in CPI arithmetic, even small weight adjustments matter.

Formalisation of Services

As incomes rose, households began paying for professionalised services babysitters, domestic attendants, pet care, gym equipment.

The informal-to-formal shift in services is now visible in the basket. Inflation is no longer measured only in commodities; it is measured in human services.

When Measurement Distorts Policy

Outdated weights do more than misdescribe reality they distort decision-making.

Under the 2012 series, food and beverages carried a 45.86% weight. That made headline inflation hypersensitive to seasonal, supply-side shocks: onions, tomatoes, monsoons.

But the Reserve Bank of India (RBI) cannot fix rainfall with interest rates.

Yet high food weight often pushed the RBI into a hawkish posture. Even if manufacturing and services were sluggish, volatile food spikes forced elevated rates.

This created what might be called the “food drama” problem policy reacting to transitory supply noise.

The new weights dampen that effect. A more representative CPI gives policymakers a sharper lens. Repo rate decisions can now reflect current consumption patterns rather than yesterday’s habits.

Why This Digital Shift Matters

The inclusion of digital services has deeper implications.

1. Services Inflation Gets Stronger

The number of services items has risen from 40 to 50.

With rural house rent included for the first time and digital subscriptions integrated, the services basket now captures a more professionalised, service-heavy economy.

Core CPI (excluding food and fuel) already commands 57.9% weight. Digital integration strengthens that dominance.

For monetary policy, this shifts attention from mandi prices to marketplace pricing power.

2. Subscription Economics Enters Inflation

Digital platforms often begin with “introductory pricing” and later transition to monetisation phases.

By tracking OTT platforms, the CPI now captures this shift. If a streaming platform doubles its price once subscriber lock-in is achieved, it will show up in the data.

This is inflation born not of supply shocks — but of business models.

3. The Transparency vs Pricing Power Debate

Digital markets create two competing forces.

On one hand, there is the “Amazon Effect”: instant price comparison drives competitive downward pressure.

On the other hand, digital gatekeepers can accumulate pricing power through subscriber ecosystems, lock-in, and algorithmic pricing.

CPI now sits at the centre of this debate. If pricing power consolidates, inflation data will reflect it.

If competition dominates, CPI will record disinflationary pressure.

The measurement framework is now equipped to observe this tug-of-war.

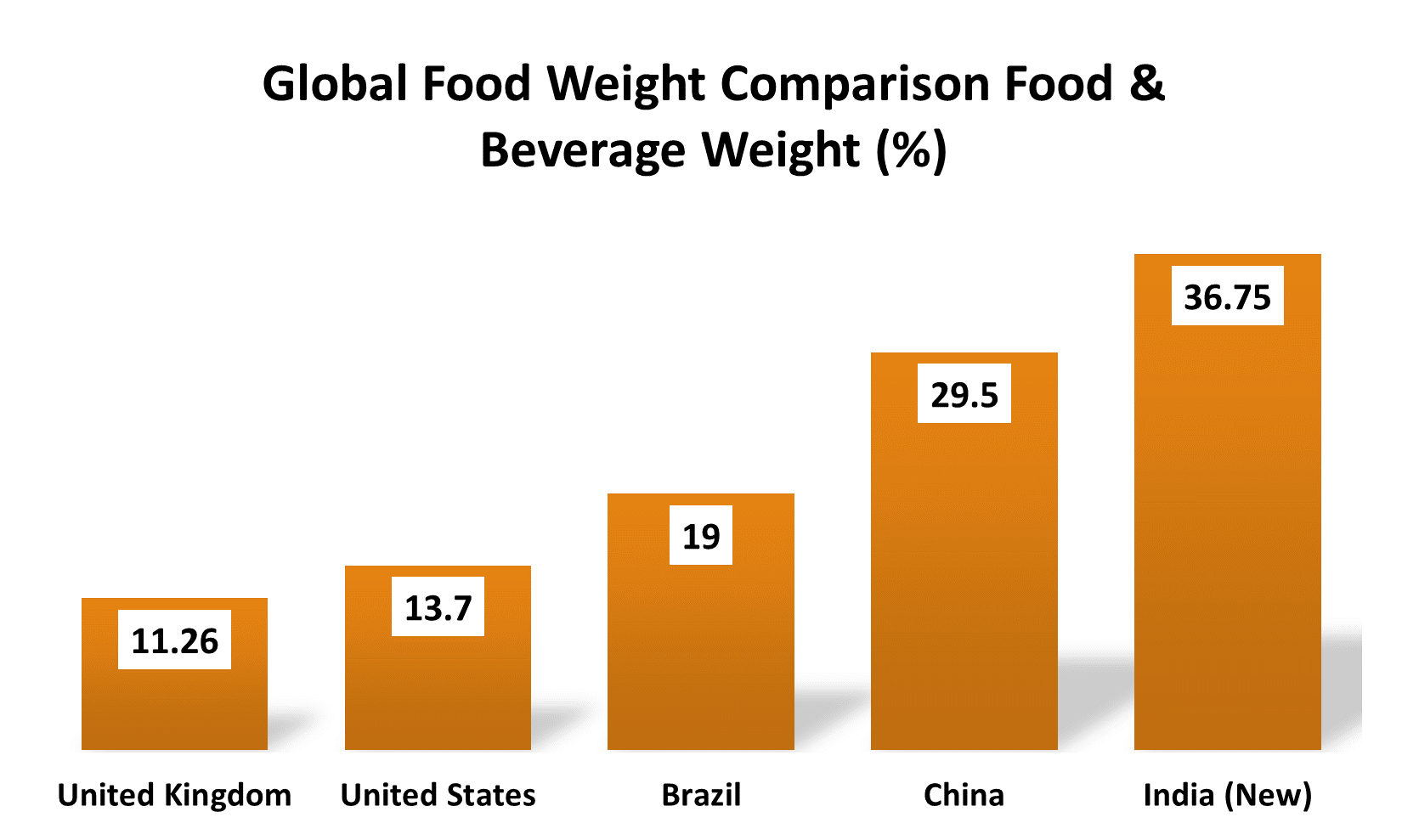

Where India Stands Globally

The adoption of the UN’s COICOP 2018 framework aligns India’s CPI hierarchy into 12 international divisions.

The IMF typically recommends updating weights every five years. India’s transition toward this cycle signals statistical maturity.

Yet India remains in transition.

India’s new food weight of 36.75% places it in an interesting middle ground.

India remains above developed economies but has moved well below traditional low-income structures.

Developed economies allocate much larger shares to services, housing, utilities, and discretionary digital spending.

This is what middle-income transition looks like in data.

Food still matters. But it no longer defines the entire inflation story.

The Dampener Effect: Less Food Drama

Now we come to the most consequential structural change: the reduction in food weight.

Under the 2012 series:

Food & Beverages weight: 45.86%.

Under the 2024 series:

Food & Beverages weight: 36.75%.

A reduction of 911 basis points.

This is Engel’s Law in action. As incomes nearly doubled over the past decade, the proportion spent on food declined, even though absolute spending increased.

Part of this drop is statistical reclassification. Restaurant meals were moved into a standalone category called Restaurants and Accommodation Services (3.3% weight). Dining out is service plus food and now the classification reflects that.

But beyond classification, this is a genuine structural transition.

Reduced Volatility, Sharper Signal

Food inflation is volatile and supply-driven dependent on monsoons, transport bottlenecks, and global commodity swings.

Lower food weight means:

Fewer extreme month-on-month swings.

Reduced headline noise.

Greater emphasis on persistent demand-side pressures.

But volatility does not disappear. It migrates.

Gold and silver jewellery now more prominent under Personal Care can introduce sharp spikes. In January 2026, silver jewellery inflation hit 159.67%.

So while food drama reduces, bullion drama may occasionally replace it.

The Bigger Question: Does Digitalisation Lower or Raise Inflation?

Now that the CPI formally includes e-commerce pricing, OTT subscriptions, data-heavy telecom plans, and digital goods, a deeper question emerges:

Is digitalisation fundamentally disinflationary or does it quietly create new forms of pricing power?

Economists tend to see this debate through two opposing lenses: the transparency effect and the pricing power effect.

Both are real. Both operate simultaneously. And the new CPI is finally equipped to observe them.

Argument 1: Digitalisation as a Disinflationary Force

There is a strong case that digital platforms lower prices.

1. Price Transparency

When consumers can compare prices instantly, sellers lose informational advantage. Research suggests that price comparison tools can generate savings of 12%–18% on essential goods.

In a digital marketplace, ignorance is expensive. Transparency compresses margins.

2. The “Amazon Effect”

Platforms like Amazon, Flipkart, and BigBasket reduce search costs dramatically. Traditional retailers must respond by cutting prices or improving service.

India’s Open Network for Digital Commerce (ONDC) attempts to go further reducing platform lock-in and commission layers, thereby potentially lowering final prices.

Competition, in this story, keeps inflation contained.

3. Efficiency Gains and Technological Deflation

Digital goods often experience rapid quality improvements at stable or declining prices think smartphones.

The CPI’s shift to a chain-based index helps capture product replacements more smoothly. Instead of struggling with outdated model comparisons, the system adapts as technology evolves.

This allows technological deflation better products at similar prices to be reflected more accurately.

From this angle, digitalisation is inflation’s enemy.

Argument 2: Digitalisation as a Source of Pricing Power

But there is another side.

Digital platforms may begin competitive and end dominant.

1. Subscription Stickiness and Lock-in

Once a household becomes embedded in an ecosystem Apple devices, Amazon Prime delivery, Netflix watchlists switching costs rise.

Firms gain pricing power not because competition vanished, but because convenience creates inertia.

2. The Monetisation Phase

Many digital services enter with low introductory prices. The goal is scale.

Once scale is achieved, prices rise.

The CPI now tracks OTT platforms like Jio Hotstar, SonyLiv, and YouTube Premium precisely to capture this transition from subsidised growth to margin extraction.

Inflation can be embedded in business models.

3. Algorithmic Price Discrimination

AI-driven pricing allows platforms to adjust prices dynamically based on location, demand, browsing patterns, or inventory.

In theory, this improves efficiency.

In practice, it can allow firms to extract consumer surplus more precisely.

Digitalisation may compress margins in commodities but expand them in ecosystems.

The CPI as Referee

What is striking about the 2024-based CPI is that it does not take sides in this debate.

It simply measures.

If digital transparency drives prices down, CPI will show it.

If platform dominance drives prices up, CPI will show that too.

The index has evolved from tracking wholesale vegetables to tracking subscription economics.

That is not trivial. It is an expansion of what we mean by “cost of living.”

Conclusion: India’s CPI Now Reflects 2024 India

Step back from the arithmetic.

What has changed?

The CPI has been recalibrated to reflect a modern, post-pandemic, increasingly middle-income India.

It is no longer a food-dominated snapshot of a lower-income economy.

It is a broader, more service-oriented mirror of current consumption.

Forward-Looking Questions

The CPI revision closes one chapter and opens several new ones.

Will Housing Weight Rise Further?

Housing, water, electricity, and gas currently stand at 17.67%. As urbanisation deepens and rural rent inclusion matures, housing could become a primary driver of inflation.

How Will EVs and Green Energy Enter CPI?

Today’s basket includes CNG and PNG. Tomorrow’s economy will include electric vehicles, charging infrastructure, and renewable energy services. Future CPI revisions will need to incorporate these transitions.

Is India Entering a Services-Inflation Era?

With core weight at nearly 58%, inflationary pressures may increasingly be driven by wage growth, urban services demand, and global commodity dynamics rather than local monsoon patterns.

That is a different macro regime.

Thank You So Much For Reading!!

Researched By- Naresh and Ayush.

Sources- NewsIndiaExpress, ET, dailypioneer, ResearchGate, ICIS, Invescomutualfund, CareRating, IndianExpress, TOI, MOSPI, theprayasindia.

Well, we all agree that all kind of data is manipulted. The governments do their best to show the rosy picture.

We wish it was different...

thanks you for sharing appreciate your efforts