Housing Inequality in India

When Homes Become Castles, and the Poor Are Left Outside the Gates

Picture this. You’re standing on a flyover in Mumbai, looking down at rows of shiny high-rises. Each tower boasts infinity pools, gyms fancier than your local club, and balconies the size of small apartments. And somewhere, hidden in the shadows of these glass castles, is the person who built them — the worker who laid the bricks, poured the concrete — dreaming of owning even a one-room home.

That dream is slipping further away. The data tells the story. Let’s break it down.

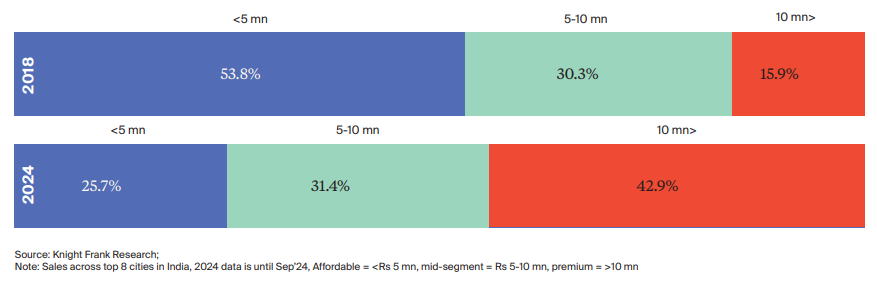

1. The Disappearing Affordable Home And the Rise of the Rich Buyer

Once upon a time — well, 2018 — affordable homes (below ₹50 lakh) made up more than half the housing sales in our top 8 cities. That was the era when we said: Look, housing for all is possible.

Fast forward to 2024. Affordable homes now form just one-fourth of sales. Meanwhile, rich buyers are on a shopping spree — premium homes have jumped from 16% to 43% of sales.

What’s really happening? The housing market feels like an exclusive club. If you have money, you’re welcome in. If you don’t, you’re kept out.

2. The EWS Category: Defined on Paper, Denied in Reality

Governments call a family earning up to ₹3 lakh a year "EWS" — Economically Weaker Section. But try buying a home on that income. The numbers don’t add up.

In 2024, EMIs would eat up 62% of an EWS household’s income. Banks won’t touch that — their limit is 50%. In Mumbai, even a tiny 30 sq m flat costing ₹26 lakh would need a household income of ₹6 lakh a year — double the official EWS limit!

Translation? The poor qualify for nothing. Our policies define the poor as earning ₹3 lakh, but our housing market defines them as earning at least double that. The system writes them out.

3. Why Builders Don’t Build for the Poor

Let’s get real — builders follow the money. In 2018, half the new homes launched were affordable. Now? Barely one-fourth. And the money trail explains why: just 3.6% of total real estate capital since 2011 went into affordable housing.

Truth bomb: It’s not personal. It’s economics. Builders don’t see profit in small-ticket homes. The math doesn’t work, so the poor get left behind.

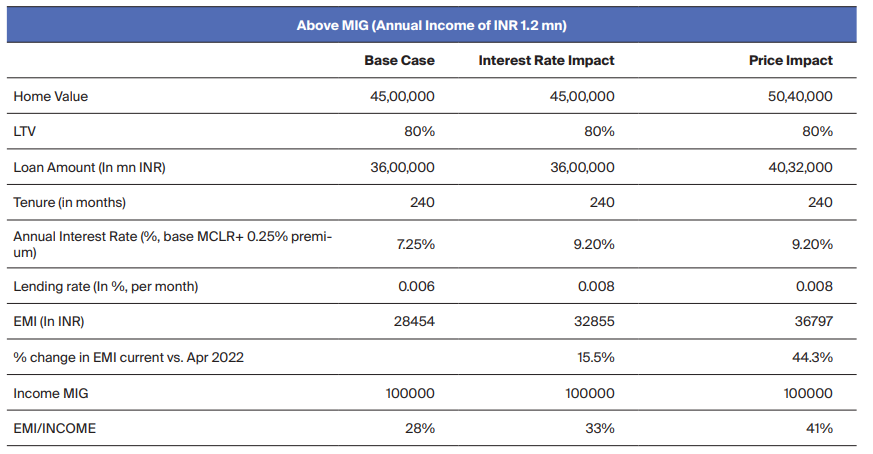

4. Rising Interest Rates: The Silent Inequality Machine

You know what rising interest rates do? They kill the dreams of the poor. There’s a strong negative correlation (-0.24, if you’re counting) between rates and priority sector housing loans. When EMIs rise, it’s the EWS and LIG folks who drop out first. Rich homebuyers? They keep buying.

It’s not just about cooling demand. It’s about how policy choices widen the gap. The RBI’s fight against inflation hits the poor harder in the housing market.

Impact assessment of interest rate and house price rise on housing affordability

MIG- Middle Income Group

5. The Smallest Homes, The Steepest Prices

Between 2019 and 2024 in Mumbai, prices for tiny flats (under 30 sq m) rose 55%, outpacing the 29% increase seen in larger flats. In a city where land is scarce, smaller doesn’t mean cheaper — it means more expensive per square foot.

Price per sq ft is higher: Micro-flats now cost over ₹25,000/sq ft, while mid-sized homes average around ₹18,000–₹20,000/sq ft.

Affordable in name, not in reality: A 25 sq m flat costing ₹30 lakh pushes ownership out of reach for EWS/LIG families — despite being branded "affordable."

Unit sizes are shrinking: Average flat size in Mumbai has fallen from 932 sq ft in 2016 to 750 sq ft in 2024, even as prices for smaller homes rise faster.

Mismatch in demand and supply: While over 60% of demand is for homes under ₹60 lakh, builders chase higher margins — leaving fewer small homes, and pushing prices up.

Bottom line: The poor pay more for less. Smaller homes are no longer an entry point — they’re a premium product disguised as affordable.

So what? The smaller the home, the steeper the inflation. When land is scarce, the poor pay more per square foot for their dreams.

Unequal Capital Flows Reflect Deep-Rooted Housing Inequality

The limited inflow of private capital into affordable housing not only signals the sector’s financial unviability but also reveals a deeper structural inequality in India’s housing ecosystem. While the premium and mid-segment housing markets continue to attract both domestic and foreign investments, affordable housing remains starved of institutional support.

Disproportionate Investment Patterns:

Between 2011-2024, of the total USD 44 billion PE inflow into India’s residential sector, affordable housing captured a mere USD 1.6 billion—just 3.6% of total real estate PE investments.

Negligible Foreign Capital Participation:

Foreign funds contributed only 15% of PE inflow into affordable housing during this period, underscoring their reluctance to enter a segment perceived as low-margin and high-risk.

In contrast, premium housing and commercial real estate have consistently attracted robust foreign investment, reflecting a global capital preference for higher-yield, premium assets.

Impact on Housing Inequality:

This capital starvation of affordable housing exacerbates housing inequality:

Supply Gap: With limited private participation, launches of affordable homes have plunged — from 52% of total launches in 2018 to just 23% in 2024.

Price Escalation: The scarcity of new affordable housing stock has contributed to disproportionate price increases, particularly for smaller units meant for EWS/LIG segments. For example, in Mumbai, units <30 sq m saw a 55% price rise since 2019, outpacing mid-segment price growth.

So What’s the Big Picture?

Let’s call a spade a spade. India’s housing policies look good in theory, but when people actually try to benefit from them, they find it’s hard to get what was promised, just like seeing fancy clothes on sale but not being able to buy them.

The poor are priced out.

Builders don’t want to build for them.

Financing is out of reach.

And the little homes that were meant to offer shelter? They’re becoming luxury goods.

What’s the Economic Concept Here?

Housing as a Market Failure.

Housing for the poor is a classic market failure. Left to itself, the market doesn’t supply affordable housing, because the returns aren’t worth it. And when the government tries to step in, it often misfires — defining EWS unrealistically, or offering subsidies that don’t match actual prices.

When markets fail this way, we need smart public intervention. Not token schemes. Not hollow slogans. But policies that make affordable housing viable for builders, for financiers, and most importantly, for buyers.

Final Word

Every home we build or don’t build tells a story of who we value, and who we leave behind. The numbers don’t lie: right now, India’s housing story is leaving the poor out in the rain.

Source - Knight Frank

Hi Nirmal, sorry for the inconvenience. It seems the issue might be from Substack’s side. You can try unsubscribing and then subscribing to our channel again, that should help.

Hey guys I don't know why but I don't receive an email when you guys publish.