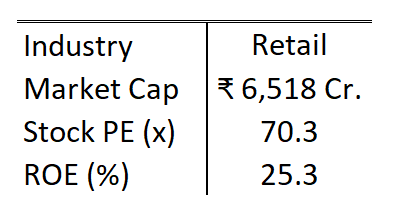

Aditya Vision Ltd.

High on debt, high on expansion!

Welcome to the 6th edition of our small-cap coverage. Today, we're diving into the electronic retail chain Company “Aditya Vision Ltd.”. Let's start! But before we do, here is the link to the fifth edition.

List of Contents:

1. Company Share Price chart & comparison with Index

2. About the Company

3. Company Journey

4. Business Model

5. Management Overview

6. KMP's Remuneration

7. ESOPs (if any)

8. Key Products/ Services

9. Revenue/Turnover Analysis

10. Financials of the Company and its analysis

11. Shareholding Pattern

12. MD&A

13. SWOT Analysis

14. Latest Concall Analysis

15. New Initiatives and Opportunities

16. Key triggers for the company in the future

17. Competitors

18. Growth Guidance by Management

19. Industry Overview

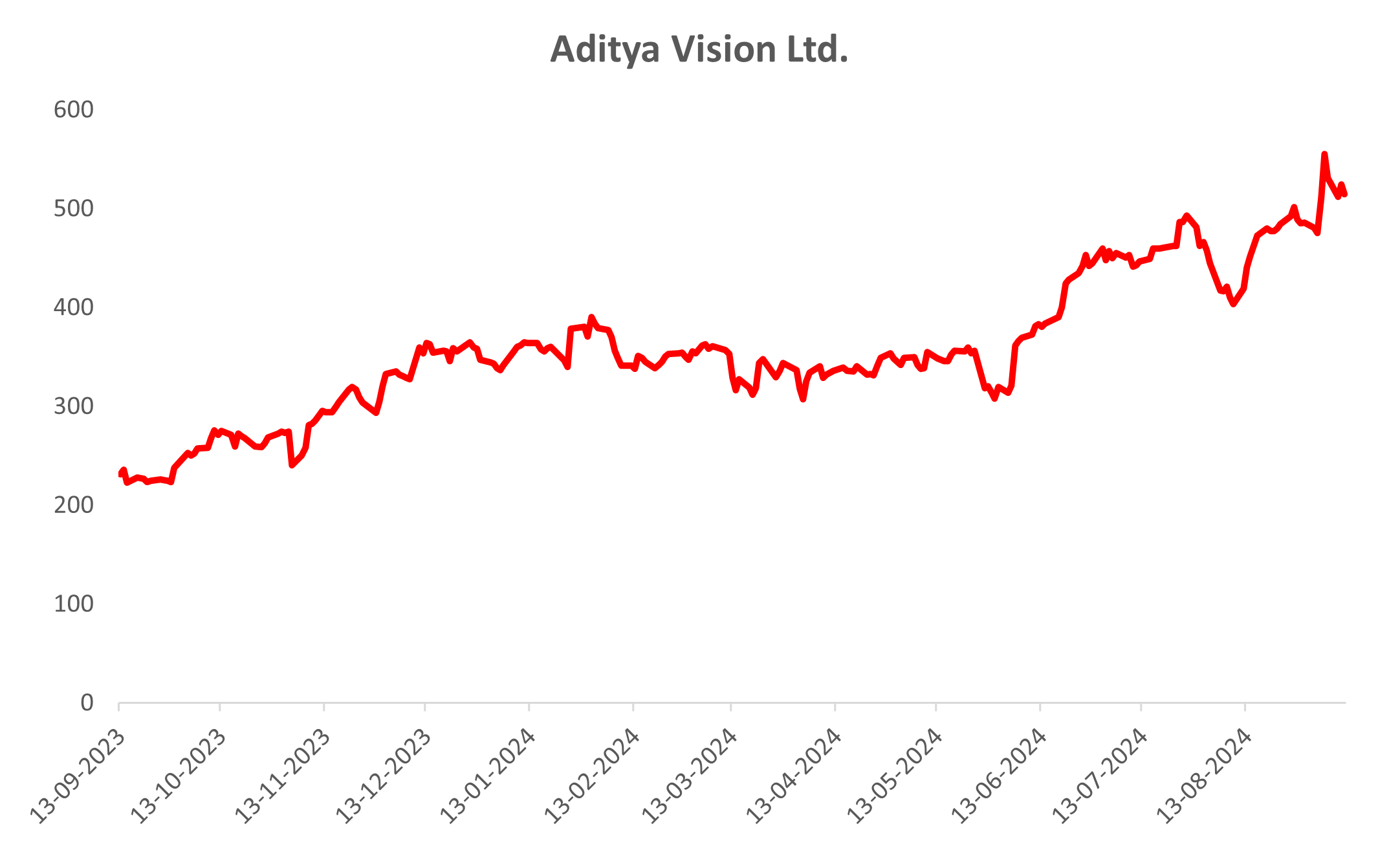

1. Company Share Price chart & comparison with Index

Comparison with BSE SENSEX 30

Comparison with BSE SMALLCAP

All above charts are *Indexed on 13 Sep 2023 (=100)

Source- Research 360

2. About the Company:

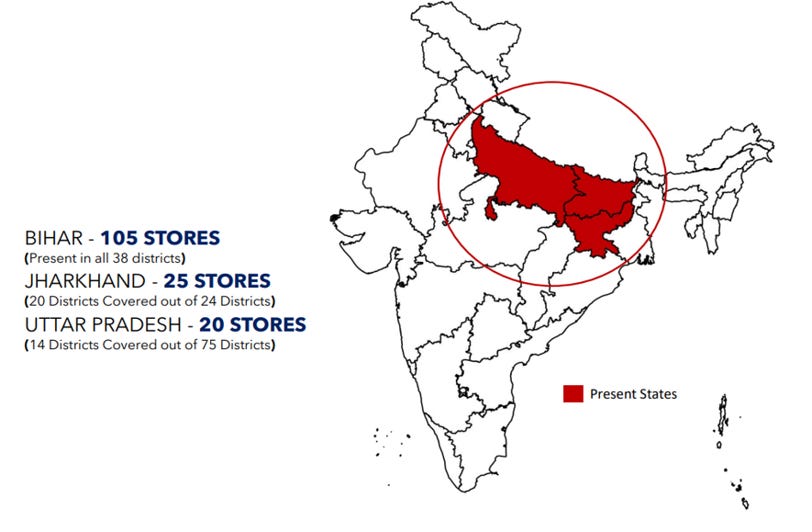

Aditya Vision Limited is a prominent multi-brand consumer electronics retail chain headquartered in Patna, Bihar. Established in 1999, the company has grown significantly, now operating over 150 outlets across Bihar, Jharkhand, and Uttar Pradesh. Aditya Vision offers a wide range of products, including digital gadgets, home appliances, and personal care items. Known for its strong regional presence, the company is also listed on the Bombay Stock Exchange, making it a notable player in India’s consumer electronics retail sector.

Business Presence

Zero Store Closure since Inception

People living in Bihar, Jharkhand & UP constitute 30% of India’s Population

• Estimated Population of Bihar: 13 crores

• Estimated Population of UP: 24 Crores

• Estimated Population of Jharkhand: 4 Crores

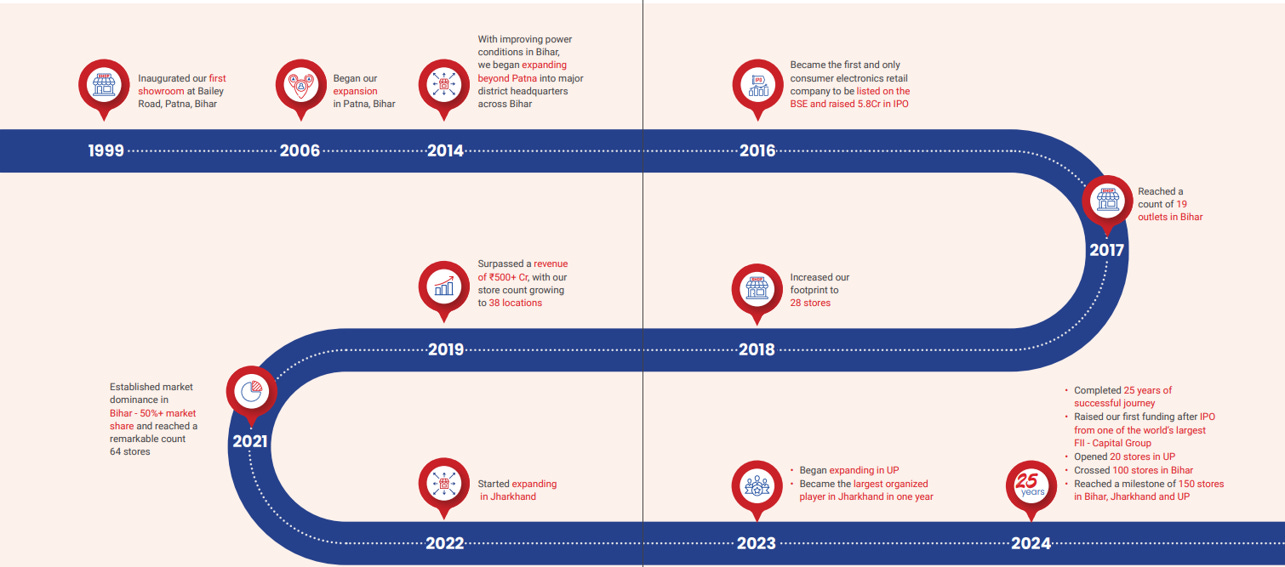

3. Company Journey-

4. Business Model

Business Model: Aditya Vision Ltd.

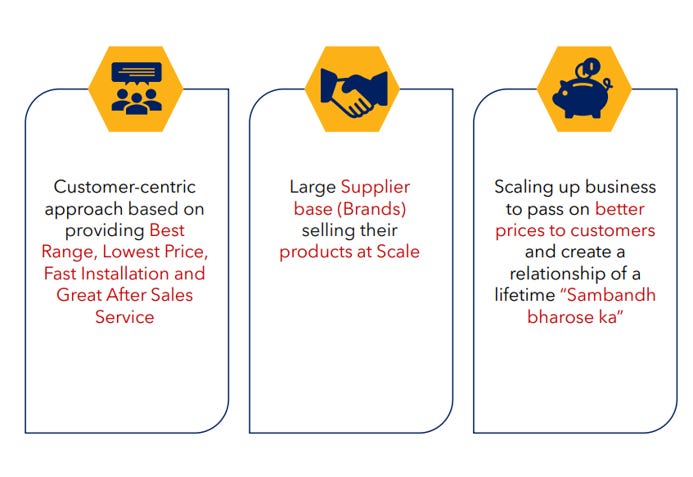

Aditya Vision has an inherently local and customer-centric retail business model that is skewed toward rural and semi-urban areas in Bihar, Jharkhand, Uttar Pradesh, and other contiguous states. The business model that the company has finds resonance in providing an experience within the store to meet very needs: a feeling of trust instilled, product verification, and personal guidance which is considered most cogent to drive sales in these regions.

1. Guidance of consumer and consultative selling approach

The company operates its business in rural Bihar, Jharkhand, and Eastern Uttar Pradesh where generally consumers are dependent upon advice from salespeople to decide upon which product to buy. In these regions, it is all the more necessary because customers have little idea about the latest models and their specifications. Consultations offered by the company help customers better judge what to buy and within which budget range.

This advisory-based sales approach helps the company in gaining higher conversion rates and ensures long-term customer loyalty.

2. High-Value Buying: Confidence and Assurance

Aditya Vision created a retail experience to restore confidence in making high-value purchases—specifically for consumer durables and electronics. Unlike small, low-value products that consumers might be quite comfortable buying online, large appliances more often than not require physical inspection. This hands-on experience is very core to its business model and hence gives the company a differentiation from online competitors, where product uncertainty and a lack of immediate customer support might cause shoppers to walk away.

3. Faith in a Known Brand

In these regions, the purchase decision is one of the major aspects based on trust. People naturally relate Aditya Vision to a brand image with a trustworthy retailer for selling products from all major national and international brands. In rural areas, people generally buy from stores with which they are familiar or can trust, especially in high-value purchases.

4. The family-oriented in-store purchase experience

White goods and consumer electronics are a family decision to buy. Aditya Vision capitalizes on this core market whereby there is joint decision-making on the fact that they are essentially large sections of the family visiting the store together to make it an occasion. It further cements the advantage of the company over online retailers whereby such habits are still prevalent in semi-urban and rural areas.

5. Robustness of the Offline Model in Consumer Durables and Electronics

Aditya Vision thrives on the resilience of offline retail in consumer durables and electronics. While online channels have picked good momentum for categories like mobile phones and laptops, large appliances are predominantly bought offline due to the verification needed for the confirmation of product usage, immediate support, and service on a personalized basis.

It is easily positioned to pick up that lion's share of this market, with immersive in-store experiences, hands-on product demonstrations paired with strategic staff consultations, especially in its served regions.

6. Focus on Tier-2 and Tier-3 Markets

The serving of hitherto untapped potentials in Tier-2 and Tier-3 cities, popularly known as the rural areas of the country, where consumer durables and electronics are mainly sold through physical stores, basically forms the core of the business model of Aditya Vision.

7. In-store Exclusivity for Ensuring the Sustainability of Revenues

Unlike online websites, Aditya Vision generates revenues through 'in-store-only' promotions, package deals, and extended warranties in a very sustainable manner. These will be designed to facilitate actual sales in the store and hence enhance the value proposition for the customer. The company is capable of offering high-ticket items with value-added services that build long-term relationships with customers while maintaining healthy profit margins.

This will be coupled with strategic store expansion, which will keep the company ahead with good competition at its edge in rural India and semi-urban India.

5. Managerial Overview-

Promoter Chairman and Managing Director

Mr. Sinha possesses a wealth of experience in consumer electronics retail and banking. Before joining Aditya Vision, He was a banker with around 20 years of experience in a PSU bank.

Promoter and whole-time director

With over 19 years of experience in Consumer Electronics retail, Mr. Prabhakar has been instrumental in overseeing the Company’s operations and spearheading the expansion of its consumer electronics product portfolio.

Promoter and Non-Executive Director

Mrs. Sinha holds key responsibilities in overseeing the day-to-day operations and managing customer relationships within the Company.

Promoter and Whole-Time Director

Mrs. Yosham Vardhan joined Aditya Vision in early 2021 and has played an important role in the growth and expansion of our company.

Company Secretary –

Akanksha Arya

Chief Financial Officer –

Dhananjay Singh

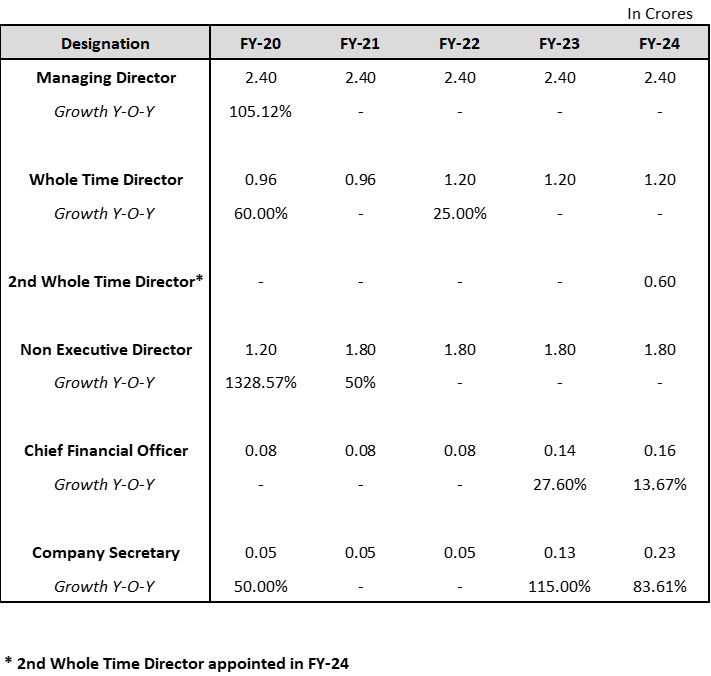

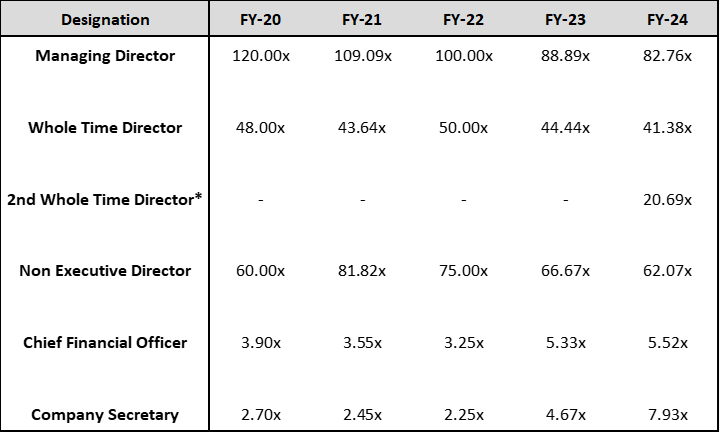

6. KMP’s Remuneration

KMP Remuneration to Median Employee Remuneration

7. ESOPs:

The total number of options approved under ESOP is 12,02,850 in the 2021 plan.

8. Key Products/ Services:

The company has more than 10,000 SKUs, encompassing digital devices like laptops, tablets, and cell phones; entertainment solutions like TVs, sound bars, home theatres, cameras, and accessories; and home appliances like refrigerators, air conditioners, air fryers, and washing machines, as well as small appliances and kitchenware like air fryers, cooktops, dishwashers, and chimneys.

Stores as per region on 31st Mar 2024.

The company sells for major brands such as:

9. Revenue/ Turnover Analysis

Revenue split:

10. Financial Statement Analysis:

SALES:

The Sales have grown at the CAGR of ~26% which is a healthy sign.

Gross Profit Margin%:

We can observe below that the gross margins have seen quite a volatile phase.

The sudden rise in material costs in FY20 led to negative gross margins.

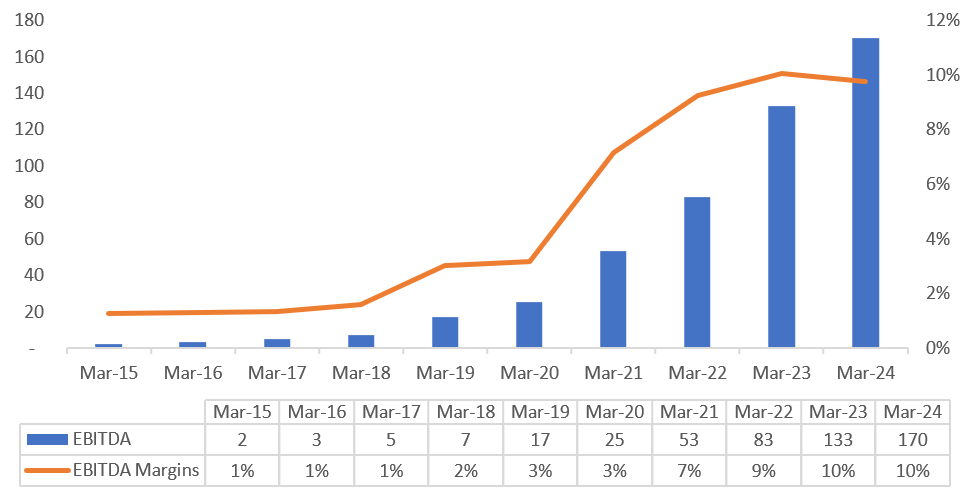

EBITDA Margin%:

Although the Gross margins have been volatile, the company has been able to consistently improve its EBITDA Margins which is a favorable outcome.

Net Profit Margin %:

Similarly, the company has also improved its Net profit margins which is a good sign.

EPS & ROE:

In the past 3 years, EPS has shown a healthy CAGR of 47%.

ROE has also increased which is a positive sign for the shareholders. In FY 2024, the ratio is 25 due to funds raised by the company from Capital Group (FII), increasing its total reserves.

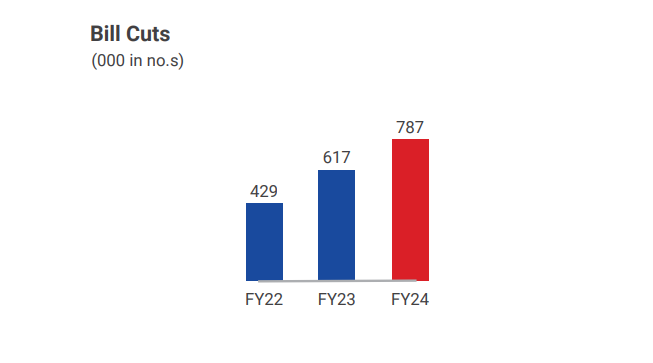

BILL CUTS:

From FY22 to FY24, the company’s number of bills has grown with a CAGR of 35.45%. This is a healthy sign as it shows the sales is strengthening.

SAME-STORE SALES GROWTH:

The company’s same-store sales growth is based on stores that have been in operation for 12+ months. The ratio has been quite volatile. This can be due to the company’s focus on rapidly expanding by opening new stores. In the past 3 years, we have seen a positive number which is a good sign today.

Important Metrics:

The company’s average selling price (AVP) has been growing but at a minimal CAGR of 4.7% in the past two financial years.

The change in Product mix clearly shows the uptrend in demand for ‘Digital Gadgets’.

The no. of stores has seen a spike in previous 2 financial years. Although this is a good sign as management seems bullish on growth, the company needs to focus on improving its AVP and sustaining the same-store sales growth.

BALANCE SHEET:

The company has paid off its long-term borrowings. Currently, the business’ borrowings include Lease liabilities and short-term borrowings only.

Debtors have remained 0 consistently which is a good sign.

The inventory levels have shot up in FY2024 but remain at < 50% average level. This is due to the company’s strategic management decision. The inventory levels have dropped down to 367 Cr. on June 30, 2024, down 66 Cr. From 433 Cr. on 31 Mar, 2024.

In the con-call of Q1 FY25, Management Quoted: “Before the start of Q1 FY ’25, we anticipated strong sales, and we were fully prepared and stocked up for the quarter demand. Due to stocking a high inventory of compressor products at the right time, Q1 has seen an exceptional revenue growth of 39%. Sale of air conditioners grew by 56% Y-o-Y

Cashflow Statement:

The company has a history of consistent Capex. This shows that the management has a bullish outlook on its growth.

KEY Ratios:

Debtor days have stayed zero consistently for the past 10 years. The company operates on a cash-and-carry model.

A dip in Fixed Asset Turnover shows a higher increase in Fixed Assets relative to an increase in Revenue.

Debt to Eq has consistently stayed high for the company which can be a point of concern.

Cash Conversion Cycle:

Debtor days have stayed close to zero.

Inventory days have seen an uprise. The management says that due to future expansion plans and a positive demand outlook, there is a need for higher inventory levels.

Days Payable increased during FY20 & FY21 but has come down to average levels.

11. Shareholding Pattern:

We can observe that after FY22, the distribution of share from the promoter’s end to FIIs & DIIs whereas the public holding has gone down. This means the company’s shares are now under low-float status compared to prior periods. This is a good sign for the investors.

12. MD&A:

Indian Economy:

India projected the highest annual growth rate among the major global economies, 7.3%12, for the fiscal year ending in March 2024. India's big economy continues to expand at the quickest rate in the world. (Source: The Economic Times)

(Source: The Economic Times)

(Source: PIB)

Indian Consumer Electronics Outlook:

The Indian consumer electronics market is growing rapidly, now ranked as the fifth largest globally. In FY22, the industry was valued at ₹1,430 billion and is projected to grow by 9-10%, reaching around ₹2,200-2,300 billion by FY27. Growth potential remains substantial due to low penetration levels, especially in Hindi heartland states, compared to other emerging markets. Factors such as rising disposable incomes, increased focus on health, wellness, and entertainment, easy access to interest-free financing, improved power supply, and climate changes are boosting demand for consumer durables. Additionally, there is a noticeable shift toward premium products, as consumers prefer high-end, feature-rich models over basic ones.

Air Conditioner: Room air conditioner penetration in India is only about 7-8%, compared to 30% globally. The market is projected to grow at a CAGR of approximately 12%, reaching around ₹50,000 crore by FY29. Consumers are increasingly choosing premium products, reflected in the rise of inverter AC sales (70-75% in FY22, up from 10-15% in FY17) and the decline in window AC sales (19% in FY22 compared to 25% in FY17).

Refrigerator: Refrigerator penetration in India is around 30-35% and is expected to grow at a CAGR of 9.5% from FY22-27 in terms of volume. With refrigerators now seen as necessities and improving power supply in tier-II and III cities, sales are expected to grow faster in these regions. Consumers are opting for larger refrigerators, with sales of 184+ litre direct cool models rising to 85-87% in FY22 from 79% in FY17, and 270+ litre frost-free models increasing to 53-55% from 48% in the same period.

Television: Television penetration is highest at over 60%, with demand driven by premiumization, as consumers upgrade from basic models to UHD, OLED, or QLED TVs. While volume growth is projected at 5-6%, price growth is expected to be higher.

Washing Machines: Washing machines, with a lower penetration of about 10%, are expected to see volume growth of 8-9% during FY22-27. The share of fully automatic washing machines has grown from 39% in FY17 to 43% in FY22.

Smartphones: The smartphone market struggled in 2022, with a 10% YoY decline in shipments to 144 million units, driven by high inflation and fewer new launches in the entry-level segment, despite improved supply conditions.

According to a CRISIL report, the consumer durables sector in India is expected to witness a revenue growth of i this fiscal year.

India is poised to become the fifth-largest consumer durables market globally and one of the fastest-growing electronics markets. This demand surge is driven by rising incomes in urban and rural areas, increasing urbanization, and changing lifestyles.

Growth Drivers:

Increased Disposable income.

Urbanization.

Favourable Government Policies.

Surging Electrification in Tier 2 & 3 Cities.

Availability of Easy Finance.

Infrastructure Development.

Growing Internet Penetration.

Growing Demand for Advanced Computing Devices Among the Working Population and Students.

Evolving Consumer Preferences and Technological Advancements

Competitive Pricing.

13. SWOT ANALYSIS:

Strengths

• Market leader in under-penetrated states such as Bihar, Jharkhand and eastern part of UP.

• Established brand & strong-standing partnerships with OEMs.

• Exceptional after-sales service.

• Investment-backed funding.

• Well-developed distribution networks in both rural and urban areas.

• First-mover in key markets.

• Increasing share of organized retail.

Weaknesses

• Stringent FDI laws impacting retail sector investment

• Rise in raw material costs resulting in higher prices

• Dependency on seasonal demand fluctuations

Opportunities

• Lower penetration of white goods compared to other developing countries.

• Easy availability of finance.

• Untapped rural markets.

• Increase in purchasing power.

• Increasing demand for premium products.

• Improved electricity access in remote areas.

• Growing internet penetration.

Threats

• Competition from regional and pan-India players.

• Deterioration in electricity conditions.

• Changes in government policies.

• Sudden surge in commodity prices.

• Rise in e-commerce.

14. Q1 FY25 Latest Concall Analysis:

A. Financial Performance:

Revenue Growth: Aditya Vision reported a revenue of ₹889 crore in Q1 FY25, a significant 39% year-on-year (YoY) increase from ₹641 crore in Q1 FY24. This growth was attributed to the strong demand for summer products like air conditioners (ACs), refrigerators, and coolers.

PAT: The Profit After Tax (PAT) grew by 42% YoY to ₹53 crore, up from ₹37 crore in the corresponding period last year. This growth outpaced the revenue increase, showcasing the company’s improving operational efficiency.

Gross Margins: Gross margins remained stable, with a slight improvement from 15.1% in Q1 FY24 to 15.2% in Q1 FY25. The company managed to maintain margins despite competitive pricing pressures.

EBITDA: The EBITDA for the quarter stood at ₹85 crore, reflecting an EBITDA margin of 9.6%. The margin remained in line with previous guidance, despite a slight dip attributed to expansion and operational costs in new regions.

EPS: The Earnings Per Share (EPS) for the quarter was ₹41.07.

B. Operational Performance:

Inventory Management: The company strategically stocked compressor products (ACs, refrigerators, etc.) before the summer season, leading to high sales. As a result, the company saw a notable 39% revenue growth, with AC sales growing by 56% YoY. Inventory levels decreased significantly from ₹433 crore on March 31, 2024, to ₹367 crore by June 30, 2024.

Geographical Contributions: Bihar remains the largest contributor to revenue at 81%, followed by Jharkhand (11%) and Uttar Pradesh (8%). The company’s same-store sales Growth (SSG) stood at 21% for the quarter, indicating robust performance in established markets.

Store Expansion: The company has reached 150 stores, with 105 in Bihar, 25 in Jharkhand, and 20 in Uttar Pradesh. During Q1 FY25, Aditya Vision added five new stores. They plan to continue expanding in underpenetrated regions like Central and Western UP and target 25-30 new store openings annually, aiming to reach 200 stores by FY26.

C. Key Growth Drivers:

Summer Product Demand: Q1 is traditionally a strong quarter for Aditya Vision due to high demand for cooling products such as ACs, refrigerators, and coolers. The company anticipated this demand and stocked up on inventory, driving sales.

Consumer Durable Market: The increasing penetration of consumer durables in rural India, rising disposable incomes, better financing options, and improved infrastructure have been key drivers for the company’s growth. Management emphasized that rural demand for durable goods is a significant growth opportunity.

D. Strategic Initiatives and Expansion Plans:

Cluster Expansion Strategy: The company follows a “creeping cluster” expansion strategy, focusing on densely covering regions before moving to new areas. Currently, they are concentrating on Central UP and plan to expand towards Western UP in the future.

Future Growth: The company has ambitious plans to expand its store network, particularly in Central UP and eventually into new territories like Madhya Pradesh and Chhattisgarh. Management expects to open 25-30 new stores annually and reach 200 stores by FY26.

Focus on New Markets: Expansion into new territories is critical for future growth. The company’s entry into Uttar Pradesh has been particularly successful, contributing 8% to total revenue in just one year. This marks an encouraging trend as the company continues to gain market share in new regions.

E. Financial Strategy and Debt Management:

Net Debt-Free Status: Following a successful fundraise, Aditya Vision is currently net debt-free. The company used a portion of the funds raised for working capital, particularly for stocking compressor products during the high-demand season. Any temporary debt is primarily related to inventory purchases and is covered by cash credit facilities.

Cost Management: Despite rising operational expenses from expansion and inflation-driven price increases for products like ACs and refrigerators, the company maintained a healthy financial position. Finance costs include interest on lease liabilities due to store expansion, but this has not negatively impacted overall profitability.

F. Market Dynamics and Competitive Landscape:

Competitive Pressures: The company faces competition in newer territories like Uttar Pradesh from local players and distributors who operate as retailers. However, management emphasized that Aditya Vision's strategic marketing efforts, such as displaying premium products, and their leadership in the 5-star AC market (with 60% of AC sales being 5-star models), give them an edge.

Impact of Price Inflation: There has been a 10-15% price increase for key products like air conditioners and refrigerators due to inflation and higher raw material costs (e.g., copper). However, management remains confident that rising disposable incomes and the low penetration of consumer durables will sustain demand.

G. Future Outlook:

The management is optimistic about the long-term growth prospects, particularly in underpenetrated markets. They plan to sustain the momentum through store expansion, efficient inventory management, and leveraging growing consumer demand in rural and semi-urban areas.

Per store metrics for the company:

The company typically generates Rs. 60Mn in the first year, doubling to Rs. 120Mn in the 2nd year and subsequently Rs. 180Mn in the 3rd year (mature store). Once a store becomes mature, the company opens a new store nearby.

15. New Initiatives and Opportunities

The company is aggressively pursuing an expansion strategy focused on increasing its retail footprint across the Hindi Heartland, particularly in Uttar Pradesh (UP), Bihar, and Jharkhand. This strategy termed the "creeping cluster" approach, involves a phased expansion from Eastern UP to Central UP within the current financial year, with a broader target of reaching 200 stores by FY '26.

The management is confident that the robust brand presence, combined with a deep understanding of regional consumer preferences, will enable the company to tap into the significant untapped potential in these regions. Additionally, the company has identified key cities in Bihar, such as Purnia, Motihari, and Arrah, where existing stores have shown strong performance, prompting plans for additional stores to meet rising demand.

In Jharkhand, the success in Deogarh has led to the decision to open a second store, further solidifying the company’s dominance in the state.

16. Key Triggers for the Company in the Future

A few number of driving factors important for the growth of the company will be Central and in due course Western UP expansion given the market potential in cities like Varanasi and Lucknow.

Product Mix Evolution:

Current and Future Product Mix: Over the next two to three years, they anticipate a gradual increase in the share of IT and mobility-related products in their overall product mix. This change is expected to occur organically as they respond to market trends and consumer demand. However, they do not plan to shift their focus entirely towards IT-related products; rather, they foresee a gradual growth in this segment within the existing product offerings.

Additionally, the management’s long-term vision includes the potential entry into new markets such as Madhya Pradesh and Chhattisgarh, which could unlock further revenue streams. Whilst some of these markets have also installed competition, past success by the firm in these similarly competitive environments increases confidence in capturing market shares.

17. Competitors in the Market:

Vijay Sales: One of the largest electronics retail chains in India, offering a wide range of products, including televisions, home appliances, smartphones, and more. They operate through both physical stores and an online platform.

Croma: Owned by Tata Group, Croma is a leading retail chain for consumer electronics and durables. It offers a diverse selection of electronics, home appliances, and gadgets across its many stores and online portal.

Reliance Digital: Part of the Reliance Group, this retailer is one of the top consumer electronics chains in India, offering a variety of products ranging from mobile phones to large home appliances. They also have a significant online presence.

Sargam Electronics: A large regional player in North India, Sargam Electronics specializes in home appliances, mobile phones, and other electronic goods. It has several stores in Delhi-NCR and nearby regions.

Electronics Mart India Ltd.: As previously mentioned, this is a growing electronics retailer, offering a wide range of consumer durables through its stores and online platform.

Pai International: Popular in South India, Pai International offers a wide range of consumer electronics, appliances, and gadgets through both physical stores and online sales.

18. Growth Guidance by Management

The management has provided clear guidance on the company’s growth trajectory, projecting the addition of 25 to 30 new stores annually, with a target of reaching 200 stores by FY '26. It is contemplating close to 500 stores in the longer run by leveraging the huge market opportunities in Hindi Heartland.

EBITDA margins are seen at around 8-10%, which the company can sustain over a period.

The sales channel will be physically retail; there is no immediate foray into online selling. This conservative approach allows the company to concentrate on its core strength—expanding and enhancing its physical retail presence.

The management’s focus on maintaining a three-year payback period for new stores, even in newer markets like UP, underscores its commitment to sustainable and profitable growth.

19. Consumer Electronics Industry Overview:

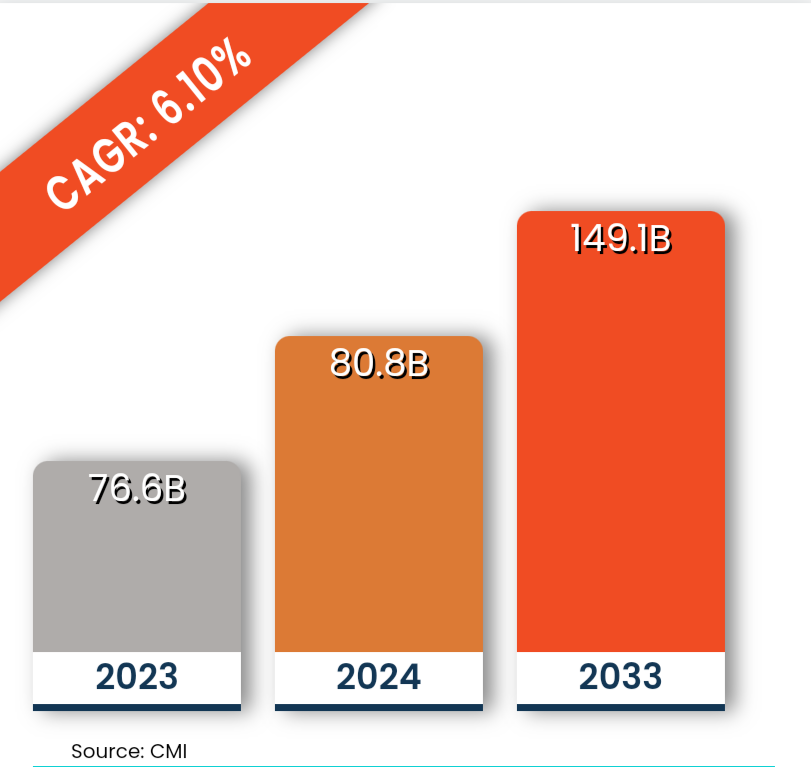

India's Consumer Electronics Market was valued at USD 80.8 Billion in 2024 and is expected to reach USD 149.1 Billion by 2033, at a CAGR of 6.10% during the forecast period 2024 – 2033.

Consumer electronics are electronic (analog or digital) equipment and devices intended for everyday use, typically in private homes. Consumer electronics include devices used for entertainment, communications, and recreation. Consumer electronics (CE) refers to devices used for communication, entertainment, or information purposes. Over the years, manufacturers developed new devices and reinvented older ones.

India Consumer Electronics Market: Growth Factors –

Indian Consumer Electronics industry is mainly driven by various factors such as increasing disposable income, increasing youth population, growing internet penetration, growing demand for advanced computing devices among the working population, evolving consumer preferences, and technological advancements.

Indian Consumer Electronics Industry dynamics are shifting rapidly. The quality and affordability of consumer electronic gadgets have been key drivers of this rapid change. With the growing economy, people’s disposable income is also increasing in India, which fuels the demand for consumer electronics.

For instance, India’s GDP is expected to more than double over the next decade, reaching USD 7.5 trillion with an expected annual growth of 6.6%. At the same time, per-capita income is expected to double, and the country is projected to have five times as many high-income households by 2031, which in turn is expected to increase the purchasing power parity, thereby driving demand for consumer goods.

Growing demand for quality consumer electronics products is expected to drive the market growth during the forecast period. In the age of the Internet and hyper-connected world, consumers have become more cautious about the worth of electronic gadgets they purchase.

With the hi-tech revolution, consumers are looking for devices that offer superior performance, durability, and reliability. According to a survey conducted by Custom Market Insights, 95% of consumers read online reviews before they shop, and 58% say they would pay more for the products of a brand with good reviews. This indicates that product quality is key when making a purchase decision.

Furthermore, the right product price balance has also played an important role in driving this transformation. Consumer goods companies understand the importance of offering value for money to consumers by offering feature-rich devices at competitive rates. Thus, above mentioned factors are expected to drive the market growth during the forecast period.

Furthermore, an increasing internet penetration and growing integration of various emerging technologies in consumer electronics devices such as Artificial Intelligence, Internet of Things, Augmented Reality, Virtual Reality, Remote Access, advancements in microcontrollers, and advanced personification technologies are expected to increase the adoption of the consumer electronics devices among working and young population, thereby driving the market growth.

India Consumer Electronics Market: Restraints –

Various factors such as less adaption and utilization in rural areas, semiconductors and other electronics component shortage in India, overdependence on imports, fluctuation in raw material prices, stringent government regulations about data privacy, growing counterfeiting of consumer electronics, higher prices of consumer electronics are restraining the market growth during the forecast period.

However, by applying the right pricing strategies, increasing domestic semiconductor and other electronics component production, and effectively coping with government regulations, consumer electronics companies can overcome the above-mentioned challenges and increase market share in the Indian market.

India Consumer Electronics Market: Opportunities –

An increasing penetration of E-commerce platforms in urban, semi-urban, and rural areas is expected to create lucrative opportunities for market growth during the forecast period. The growth of e-commerce platforms such as Flipkart, amazon, and respective company’s websites has made consumer electronics devices easily available to a broader audience in the Indian market.

The growing popularity of online purchasing due to alluring discount offers and easy and installment payment options is boosting the sales of consumer electronics devices across the country, which in turn creates lucrative opportunities for the market during the forecast period.

The IT industry in India is thriving, and there is no shortage of highly talented and skilled IT forces in India. From engineers and software experts to technicians, India’s skilled IT labor has greatly contributed to developing consumer electronics manufacturing.

Furthermore, supportive government policies and initiatives such as the Production Linked Incentive Scheme and the ‘Make in India’ initiative and growing subsidies for local manufacturing are attracting global players in the Indian Market.

Recently, the Ministry of Electronic and Information Technology proposed incentives for local smartphone manufacturers in the country. Thus, such supportive government policies and initiatives are expected to create lucrative opportunities for the consumer electronics market during the forecast period.

India Consumer Electronics Market: Recent Developments –

• Apple had a stellar year, finishing at 9 million units, despite having the highest ASP of USD 940. This was led by previous generation iPhone models and its push for local manufacturing. Its iPhone 13/14 was among the Top 5 shipped models annually.

• Samsung remained in the leadership position, with a record high ASP of USD 338, although with a 5% shipment decline YoY. Its Galaxy A14 was the highest-shipped device in India in 2023.

• In January 2023, Samsung launched its latest 2023 Side-by-Side Refrigerator Range, exclusively manufactured in India, and tailored with features designed specifically for the Indian market. Through this new product launch, Samsung is aiming to expand its presence in the Indian market.

Source – custom market insights

Thank you for reading till the end! I hope you enjoyed this report.

Researched By- Naresh, Mayank and Vaibhav

All information is sourced from company annual reports, screener.in, and industry reports.

Disclaimer- We do not recommend buying or selling any stock. You should consult your financial advisor before buying or selling any financial instrument.