Here at EquityEdge Research, we make Small-Cap Investing easy for you by Backing you up with Robust & Full-Fledged Research.

New Addition: Breakdown of Raw Materials in Our Premium Reports. This will help you understand the Major costs for the company.

What Else You Need…Let Us Know?!

Please Fill the form Below if you are interested in our Services and would like a Free Sample of our Equity Research Report covering a Small/Micro-cap Company.

Read our Previous Report here:

India Glycols Ltd.

Here at EquityEdge Research, we make Small-Cap Investing easy for you by Backing you up with Robust & Full-Fledged Research.

Table of Contents:

Key Highlights.

Company Price Chart Analysis.

About the Company.

Management Analysis.

Business Breakdown.

Financial Analysis

Ratio Analysis.

Shareholding Analysis.

SWOT Analysis.

Concall Analysis (Q1FY26).

Growth Drivers & Risks/ Challenges for the Company.

Competitor Analysis.

Premium (Includes Free):

Global Pharmaceuticals Industry.

Indian Pharmaceuticals Industry.

Financial Analysis- Quarterly.

Competitive Analysis- Bio & Financials.

Daily Share price trend TTM- Peer comparison.

Company Relative Valuation.

Raw Material Breakdown.

1. Key Highlights:

FY25

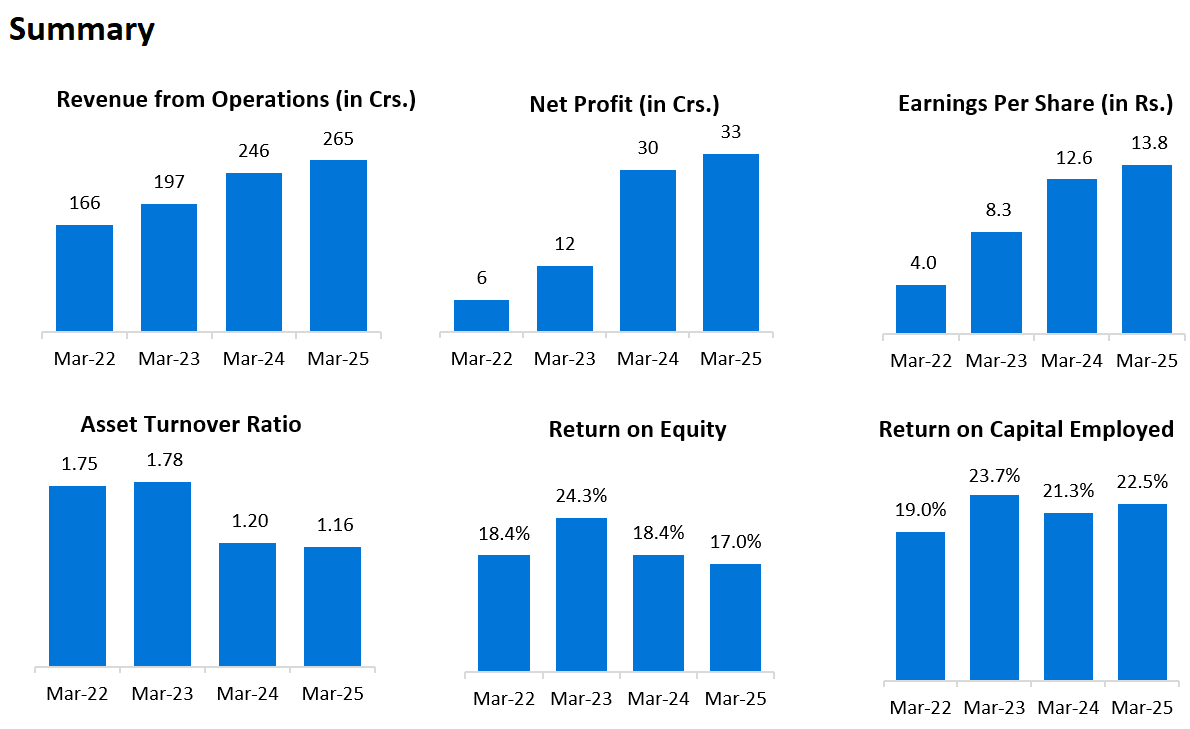

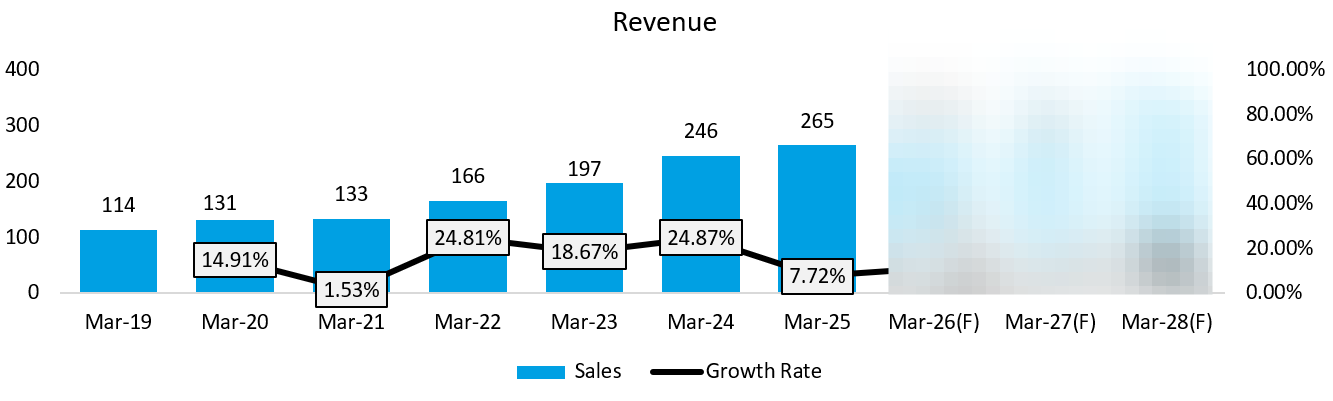

REVENUE: ₹ 265 Cr. (+7.72% YoY)

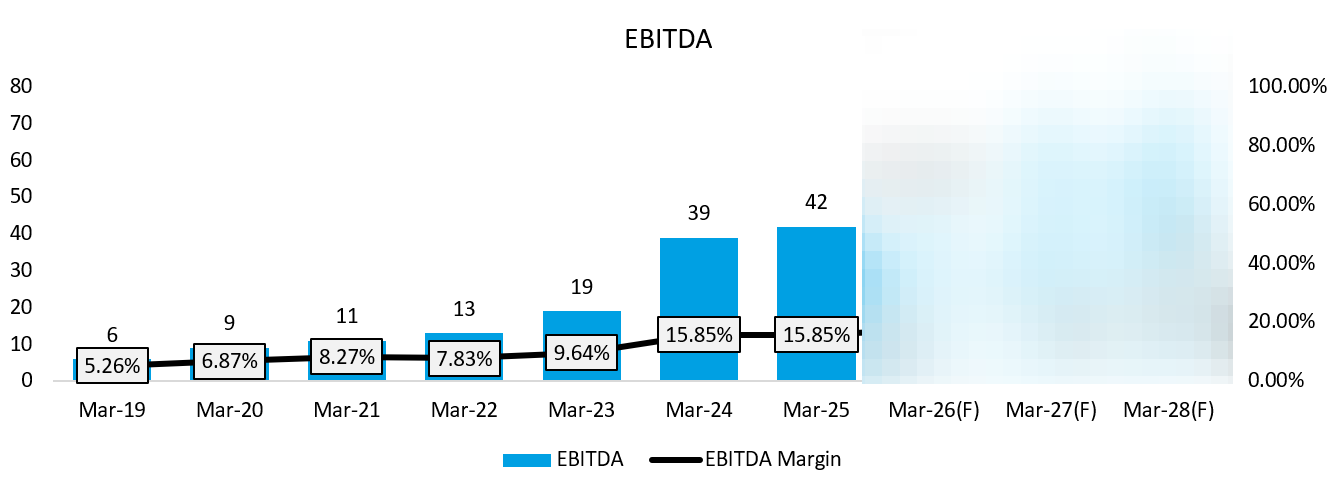

EBITDA: ₹ 42 Cr. (+7.69% YoY)

EBITDA MARGIN: 16% (No Change in YoY)

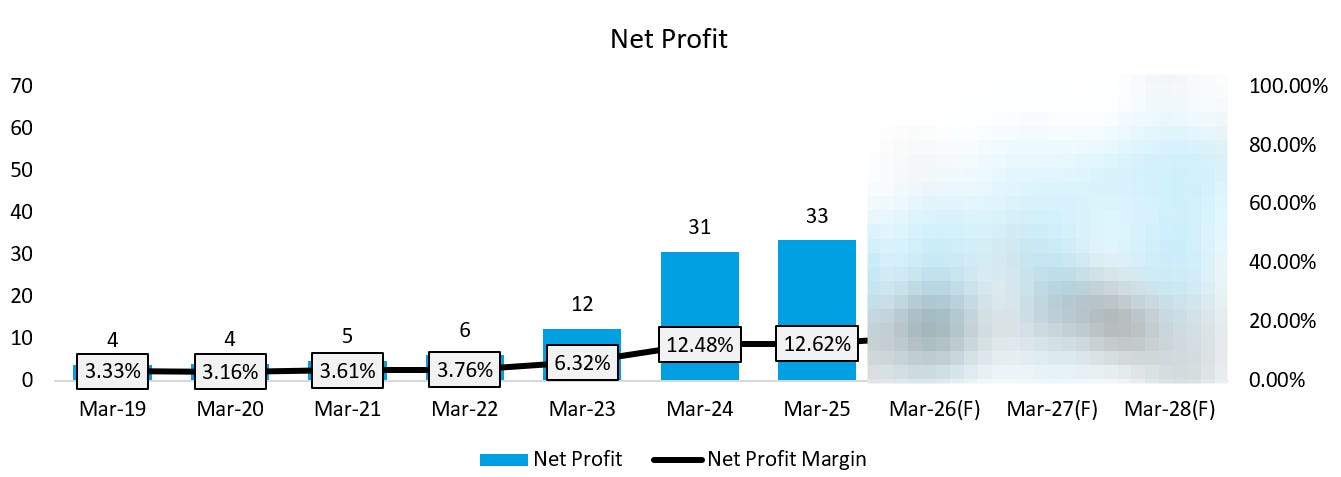

PAT: ₹ 33 Cr. (+10% YoY)

H1FY26

REVENUE: ₹ 139 Cr. (No Change in Half Year, +10.32% YoY)

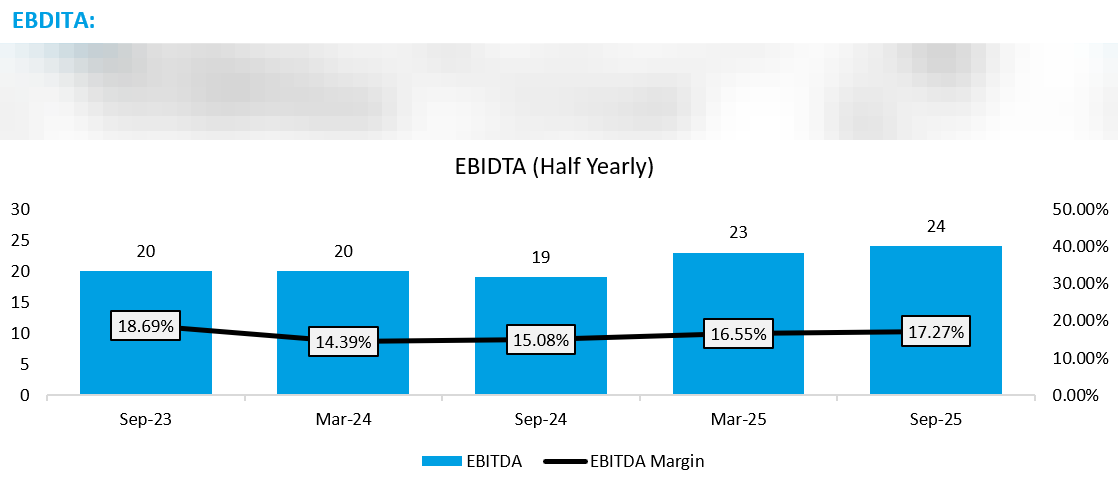

EBITDA: ₹ 24 Cr. (+4.35% Half Yearly, +26.32% YoY)

EBITDA MARGIN: 17% (No Chnage in Half Yearly, +200 bps YoY)

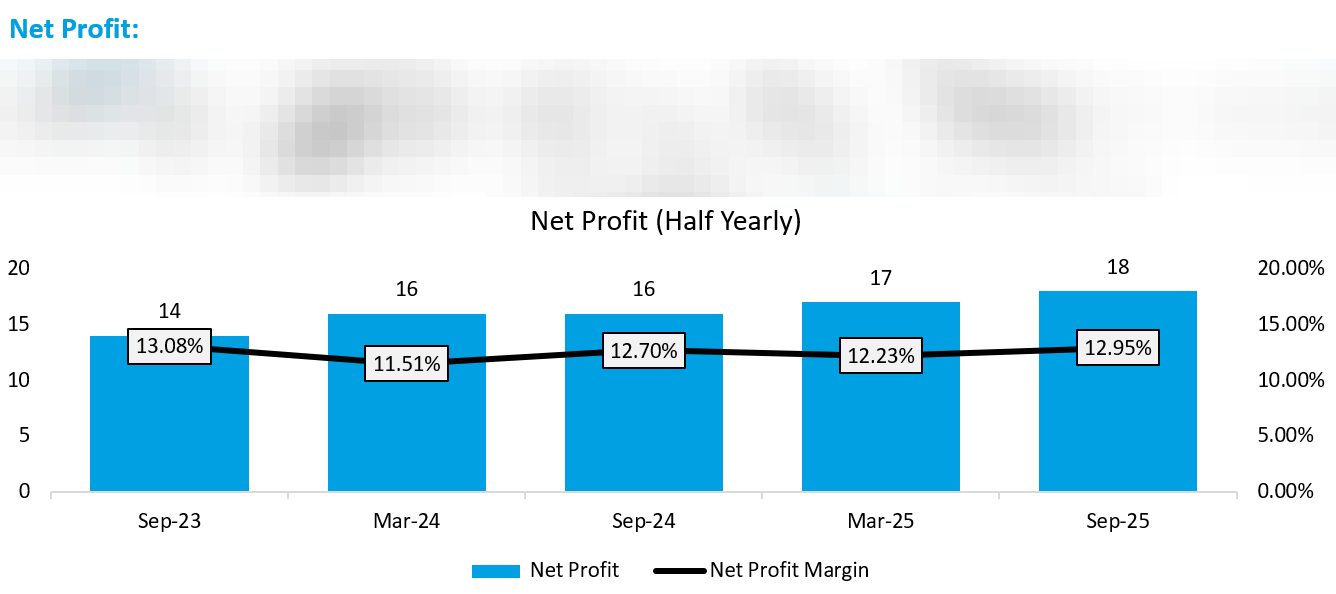

PAT: ₹ 18 Cr. (+5.88% Half Yearly, +12.5% YoY)

OTHER HIGHLIGHTS:

Manufacturing Prowess: Two state-of-the-art facilities in Gujarat (Pirana and Dahej SEZ) with a total installed capacity of 9,200 MTPA.

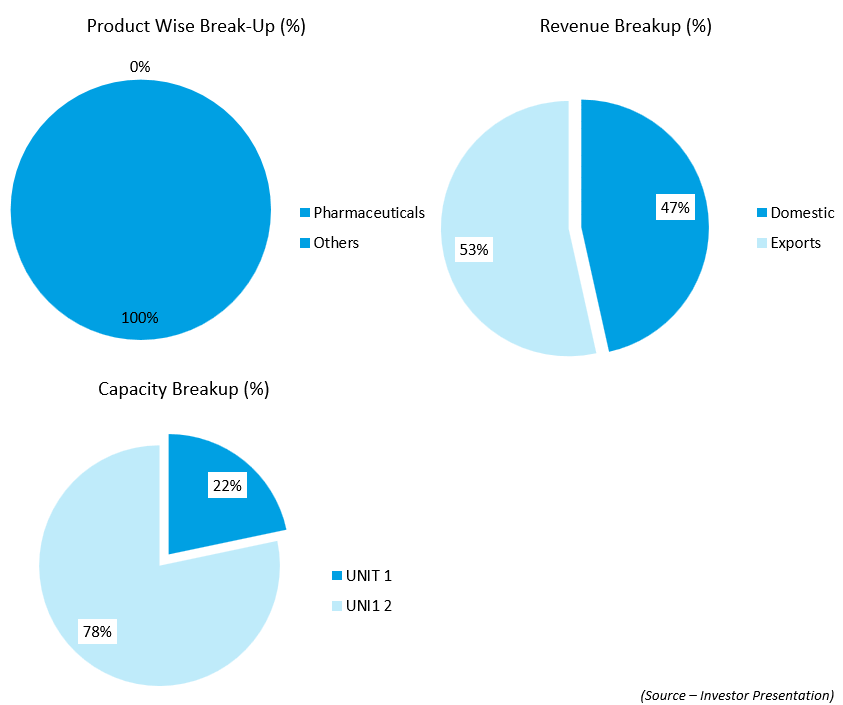

Global Reach: A balanced revenue stream with 53.49% from exports and 46.51% from the domestic market.

Order Pipeline: Has a confirmed order book for the next 3 months, ensuring operational stability and predictable demand.

Strategic Expansion: Establishing a third manufacturing facility in Nayka Kheda, Gujarat.

This will increase total capacity from 9,200 MTPA to 12,000 MTPA.

It focuses on product diversification into high-margin excipients like Croscarmellose Sodium (CCS) and Sodium Starch Glycolate (SSG).

Projected to generate ₹70 Crore in revenue in Year 1.

Market Diversification: Actively exploring new applications for its products in segments like cosmetics, food & beverages, and textiles to drive future growth.

2. Company Price Chart Analysis:

*Comparison charts are Indexed*

2.1 Accent Microcell Ltd. Performance:

2.2 Accent Microcell Ltd. Vs. NIFTY:

2.3 Accent Microcell Ltd. Vs. NIFTYSMLCAP50:

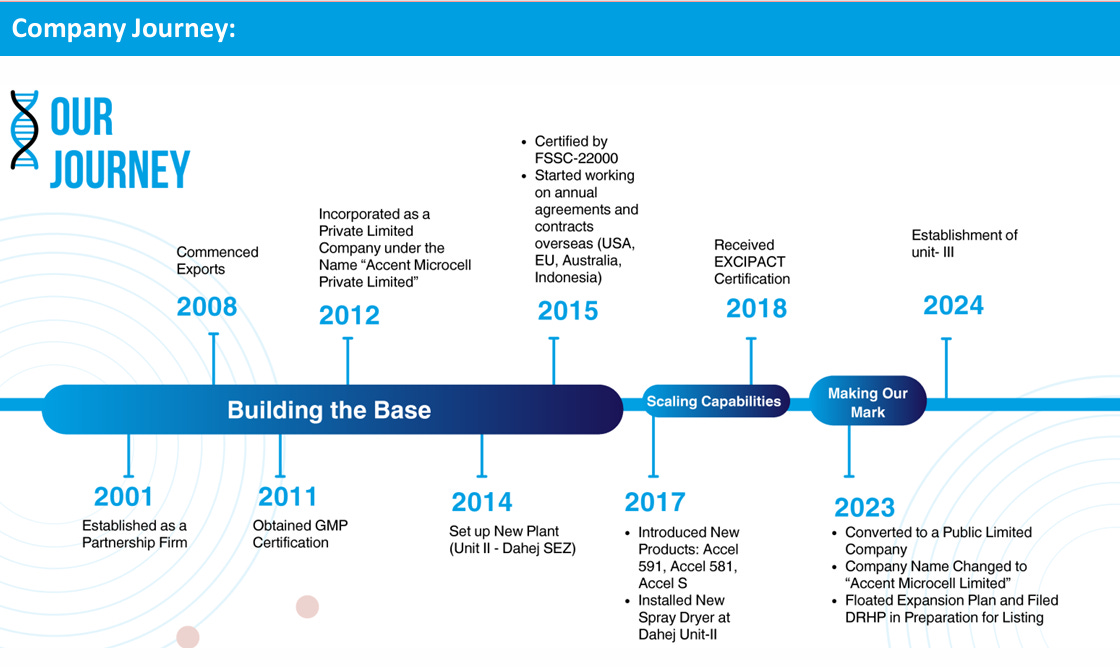

3. About the Company:

Accent Microcell Ltd., headquartered in Ahmedabad, Gujarat, is a specialised manufacturer in the domain of excipients and cellulose-based materials. It focuses on producing microcrystalline cellulose (MCC) and related cellulose derivatives, which form the backbone of many formulations in the pharmaceutical and nutraceutical industries.

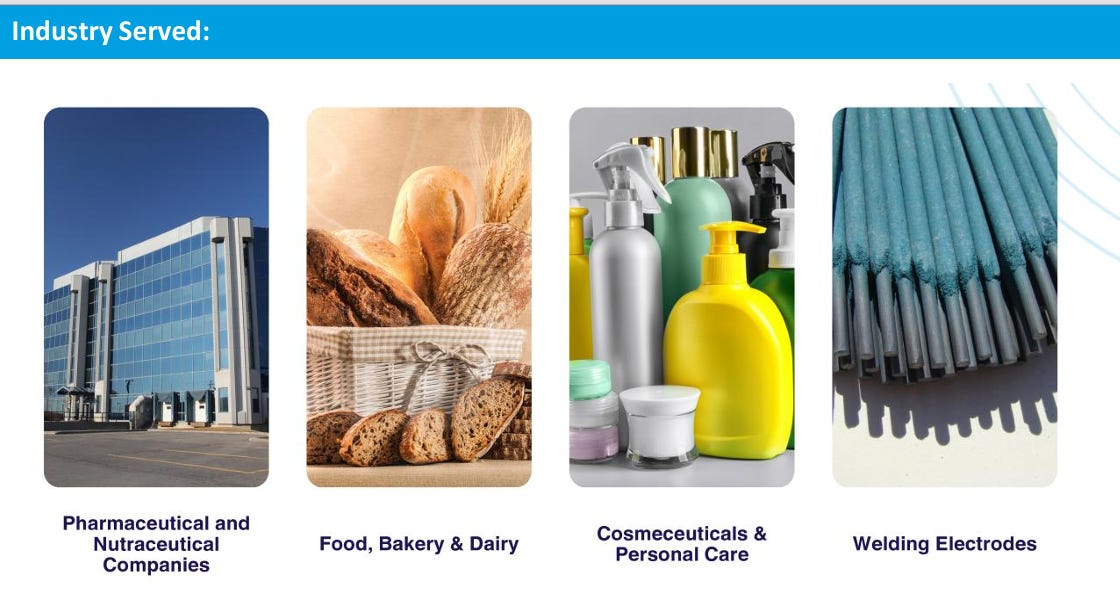

Over time the company has broadened its application base—supplying to food, bakery & dairy, personal-care & cosmetics, textile & leather, paints & ceramics, rubber, plastic, filtration, and other industrial sub-segments.

With operations at two major plants (Pirana unit and Dahej SEZ unit) and a global export footprint, Accent positions itself as a quality-driven excipient partner serving more than 10 end-use sectors and 200+ customers worldwide.

BUSINESS SEGMENTS:

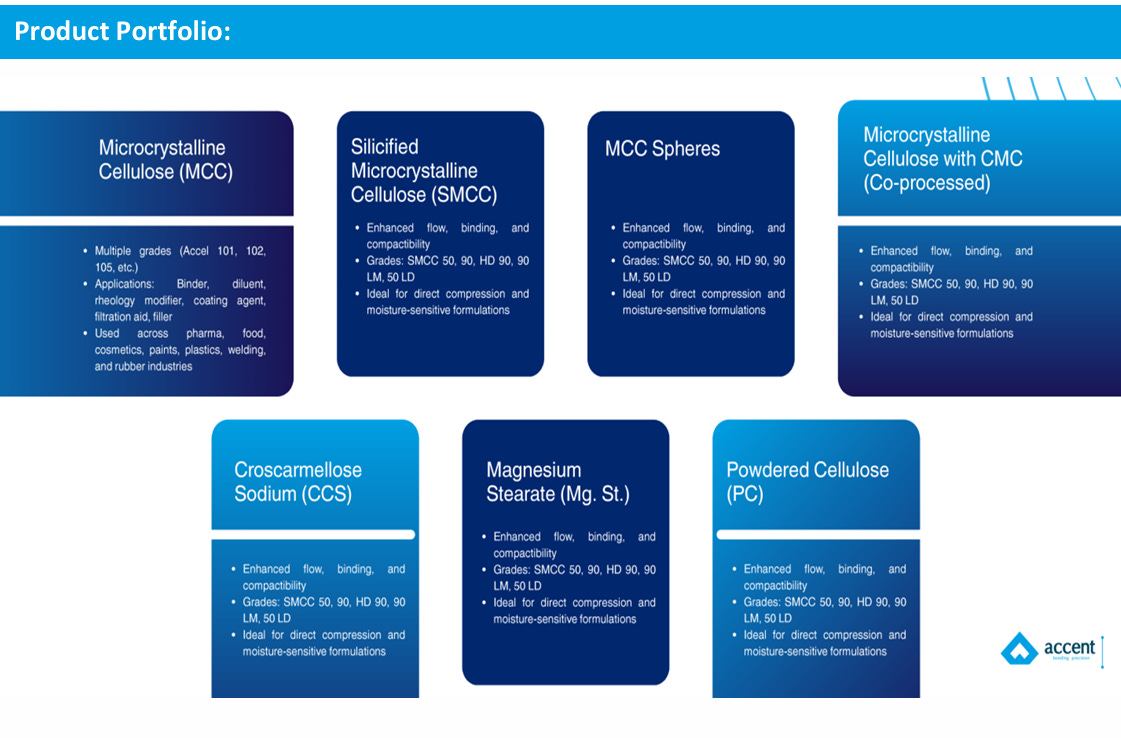

Pharmaceutical & Nutraceutical Excipients: This is the foundational area: Accent manufactures microcrystalline cellulose (MCC), silicified MCC, MCC spheres, cross-carmellose sodium, magnesium stearate and other cellulose-based excipients which are used in tablets, capsules, coatings, binders, fillers and disintegrants. These materials are critical in pharmaceutical formulations for delivering active ingredients, ensuring stability, and enabling valid release profiles.

Food, Bakery & Dairy and Consumer Industries: Beyond pharmaceuticals, Accent supplies its cellulose-based and excipient materials to food, bakery and dairy sectors (as anti-caking agents, fillers, texturisers), and to consumer products (cosmetics, personal care). This segment broadens the application of its core materials into everyday consumer and industrial use.

Industrial & Specialty Applications: This covers a range of non-consumer uses: textile, leather, paper & board, paints & ceramics, construction & cements, welding electrodes, rubber, filtration, plastics. Essentially, Accent leverages its cellulose derivative technologies into industrial and specialty materials markets, reflecting diversification beyond pure pharmaceutical excipients.

(Information related to Raw Materials provided in Premium Version.)

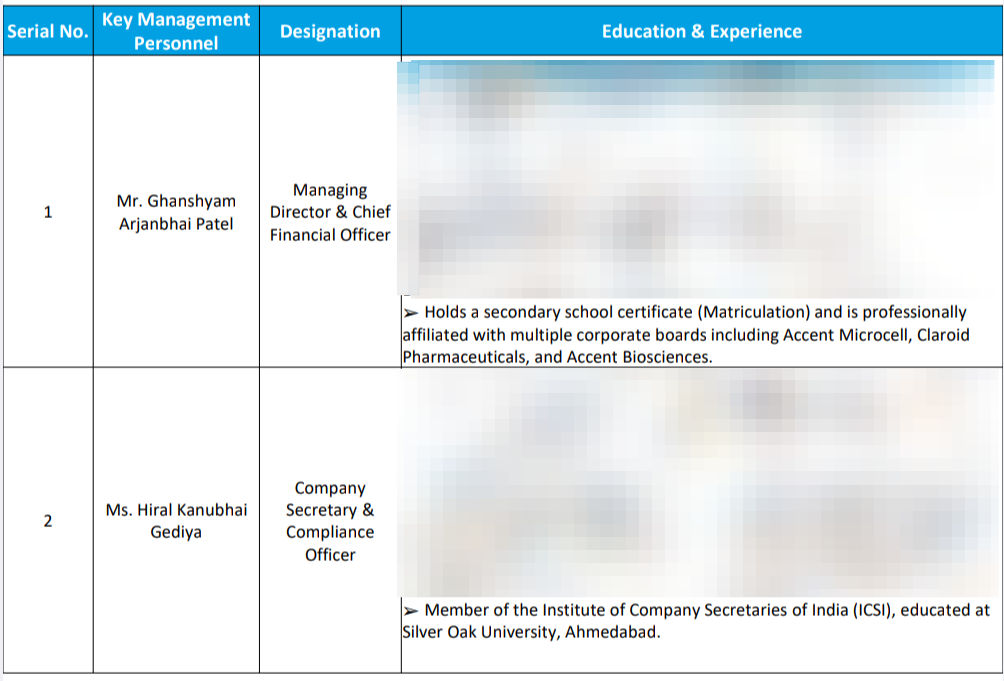

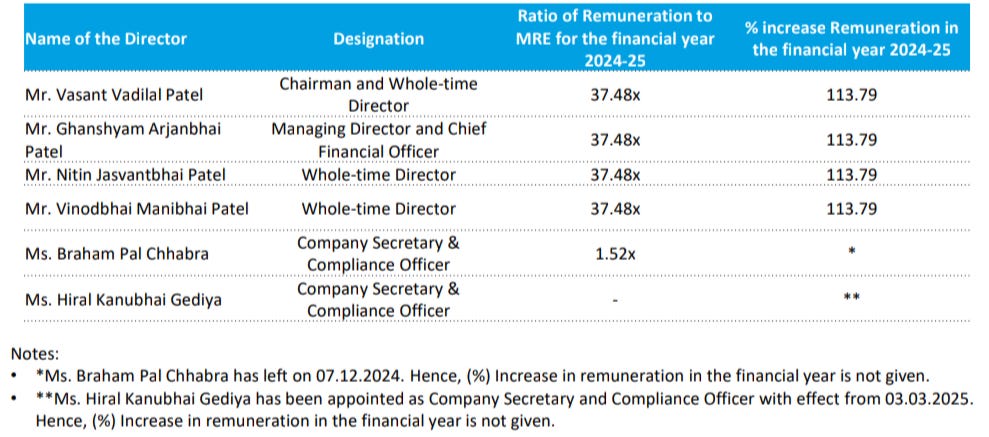

4. Management Overview:

4.1 KMP's Remuneration:

5. Business Breakdown:

6. Company’s Financial Analysis:

QUARTERLY ANALYSIS:

(Read detailed Quarterly Analysis in the Premium Version)

ANNUAL ANALYSIS:

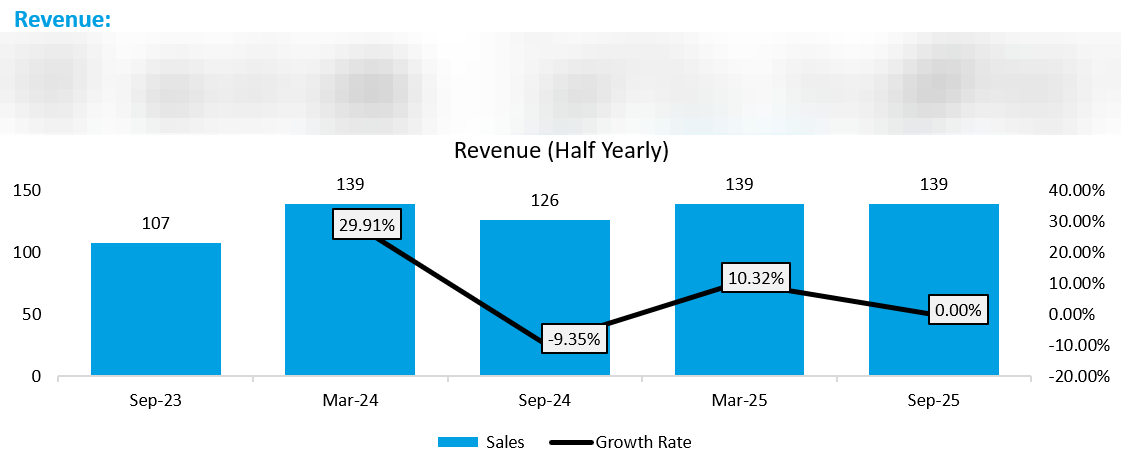

6.1 Revenue:

(Read detailed Annual Analysis in the Premium Version)

Accent Microcell Ltd.’s revenue was ₹246 crores in FY24, saw a huge revenue increase (+24.87% growth) the management points to commissioning/scale-up and increased international sales the major reason. Revenue stood at 7.72% revenue growth and stood at ₹265 crores.

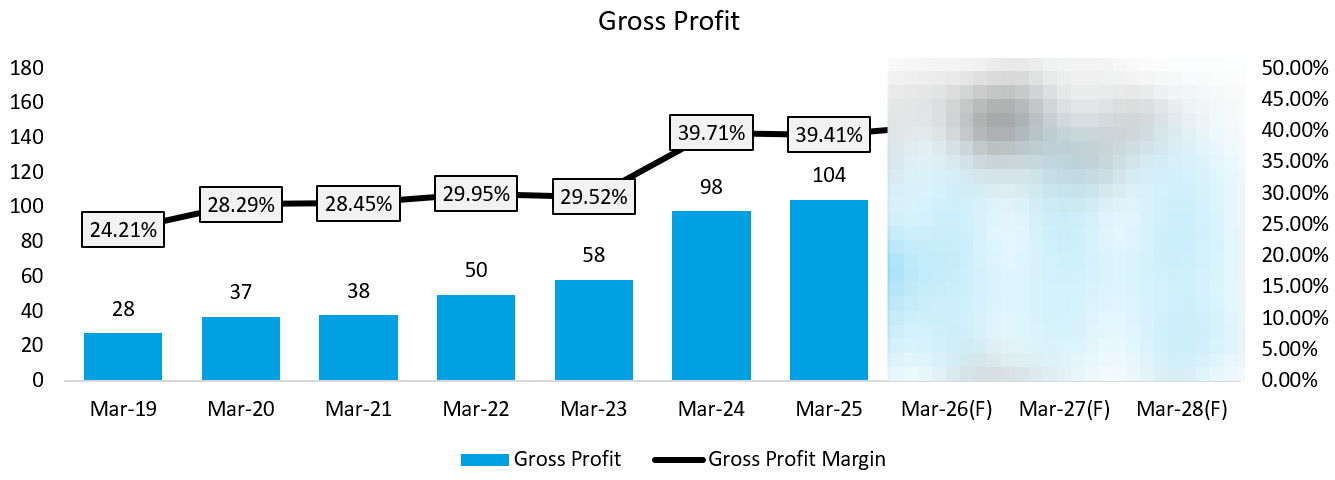

6.2 Gross Profit:

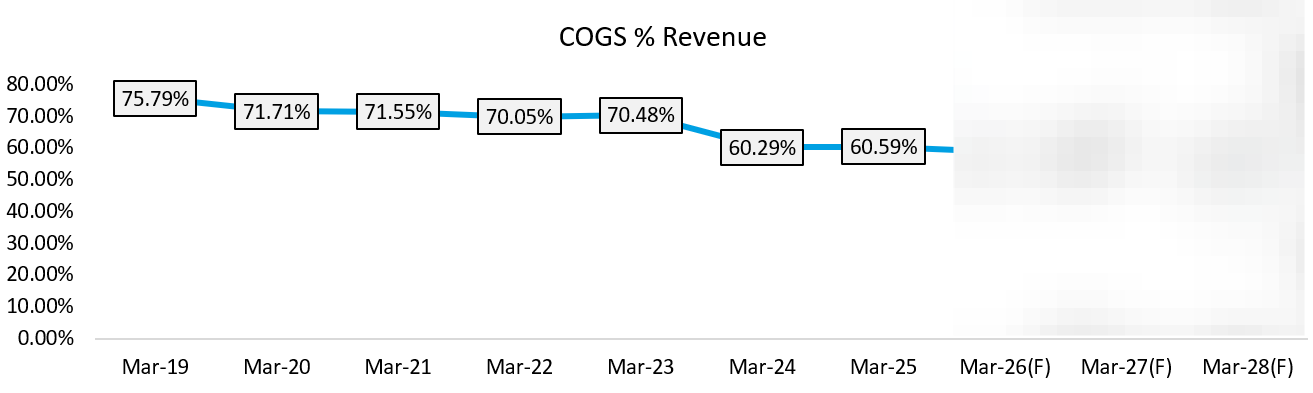

There was a huge increase in gross profit in FY24, which stood at ₹98 crores. The margin increased due to fall in the prices of Raw Materials by 1000bps. Also the management says that they are expanding capacity to manufacture higher-value products. The premiumization is adding to the reason. We can notice that for both FY24 and FY25, the margins have held up at ~40%.

6.3 EBITDA:

EBITDA rose to ₹39 crores in FY24. This increase is mainly due to the growth driven by increase in sales volume. Lower input cost and lower freight rates.

6.4 Net Profit:

FY24 saw a substantial earnings jump (12.48% increase YoY), this was due to higher sales growth and lower COGS. The company saw better demand in FY24 and FY25. Lower financing costs and income from other sources also are key growth drivers.

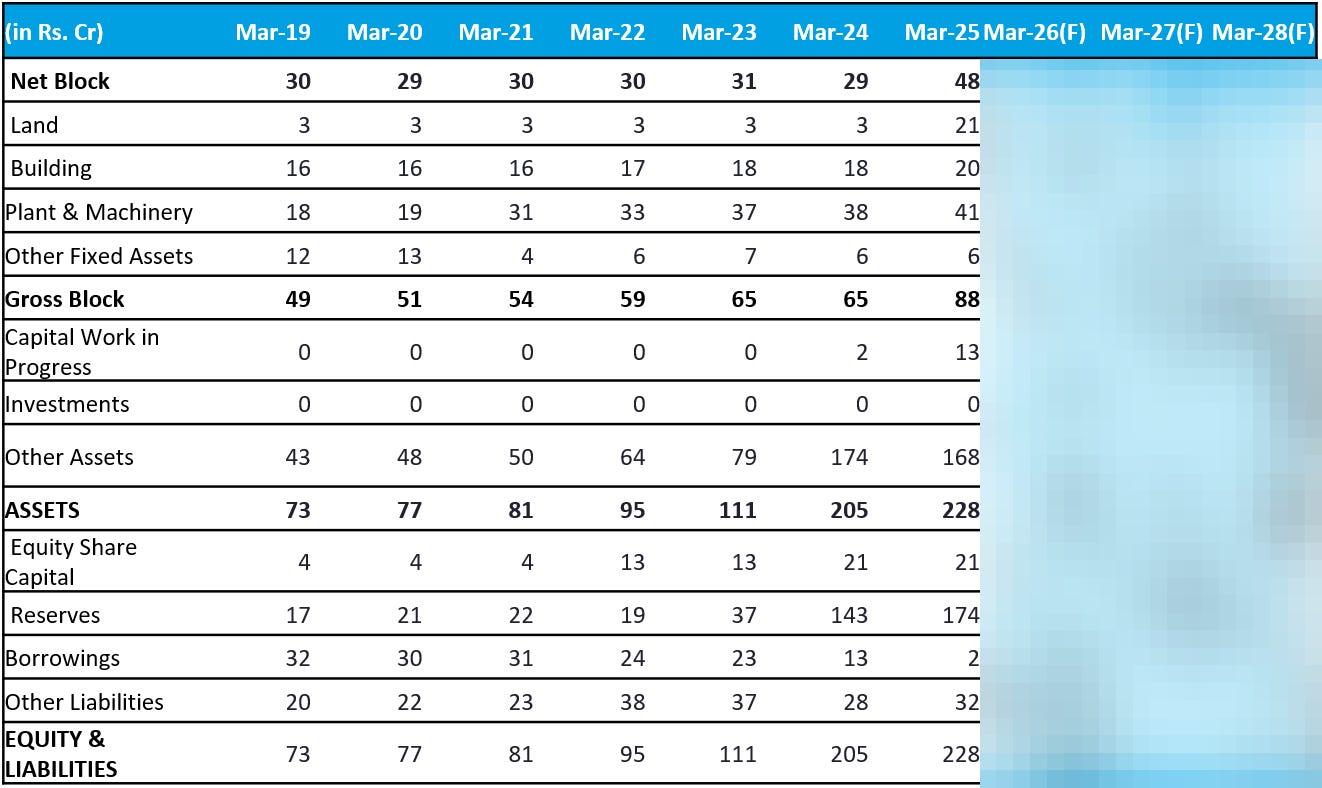

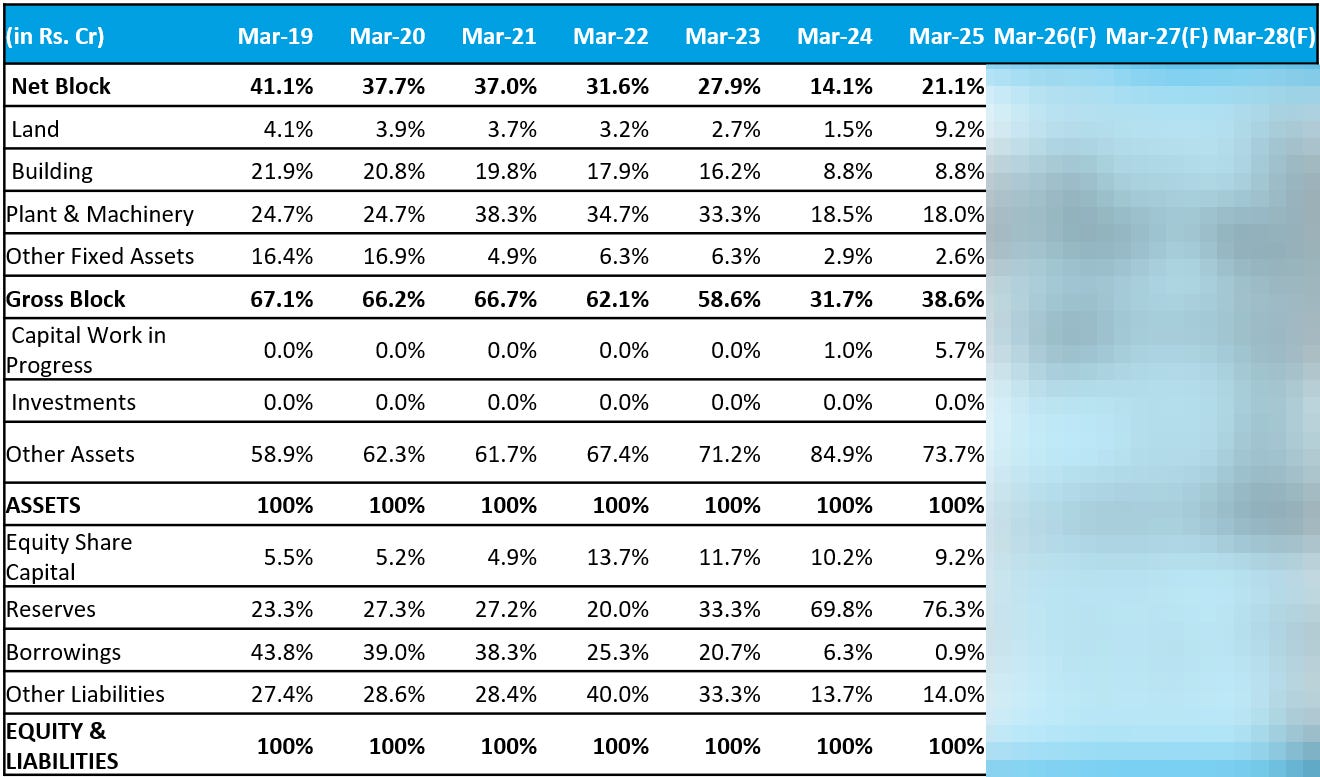

6.5 Balance Sheet:

6.6 Common-Size Balance Sheet:

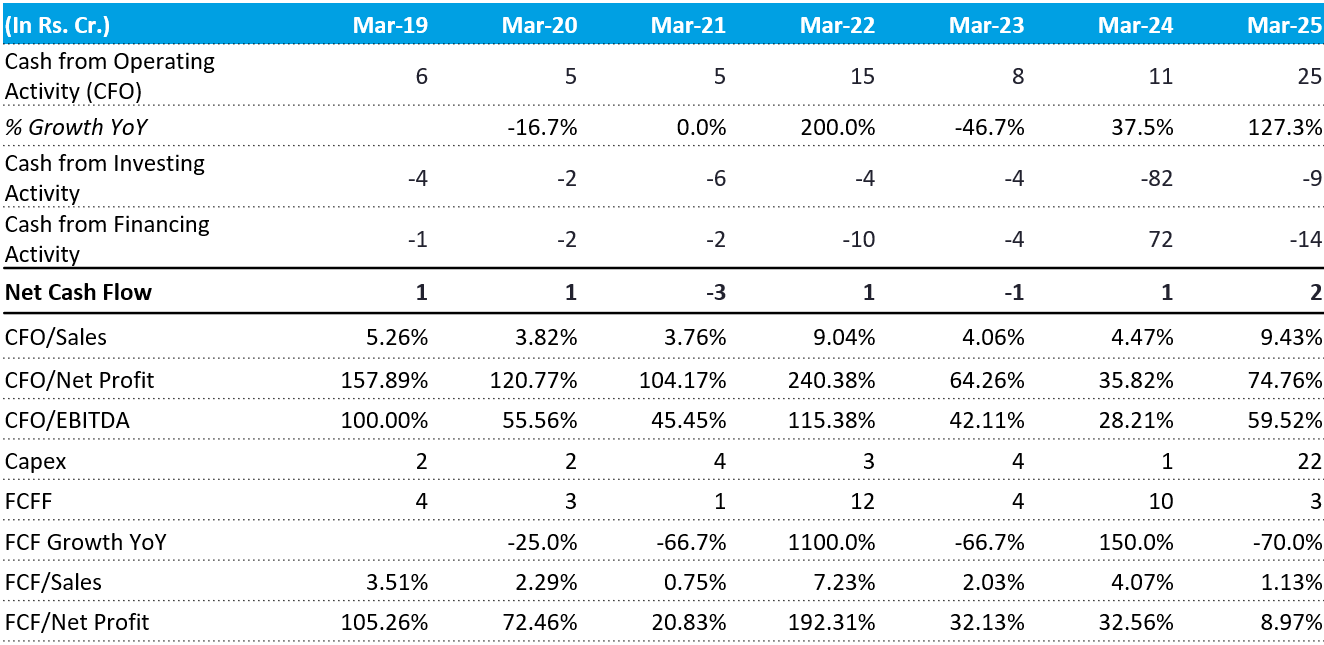

6.7 Cash Flow Analysis:

CFO stood at ₹25 crores in FY25. The surge in FY25 suggests very strong operational cash conversion: perhaps strong sales growth (and collections), improved efficiencies and favourable working capital movements.

The -₹82 Cr in FY24 suggests a significant capital investment or acquisition. The major investments are back to normalised level in FY25.

In FY24, there’s a large positive 72 Cr financing inflow- which was due to the new capital raised by the company.

Free Cash Flow (FCFF) remained inconsistent. A low FCFF despite strong CFO (as in FY25) is because the firm is ploughing cash into growth rather than returning cash or accumulating cash reserves.

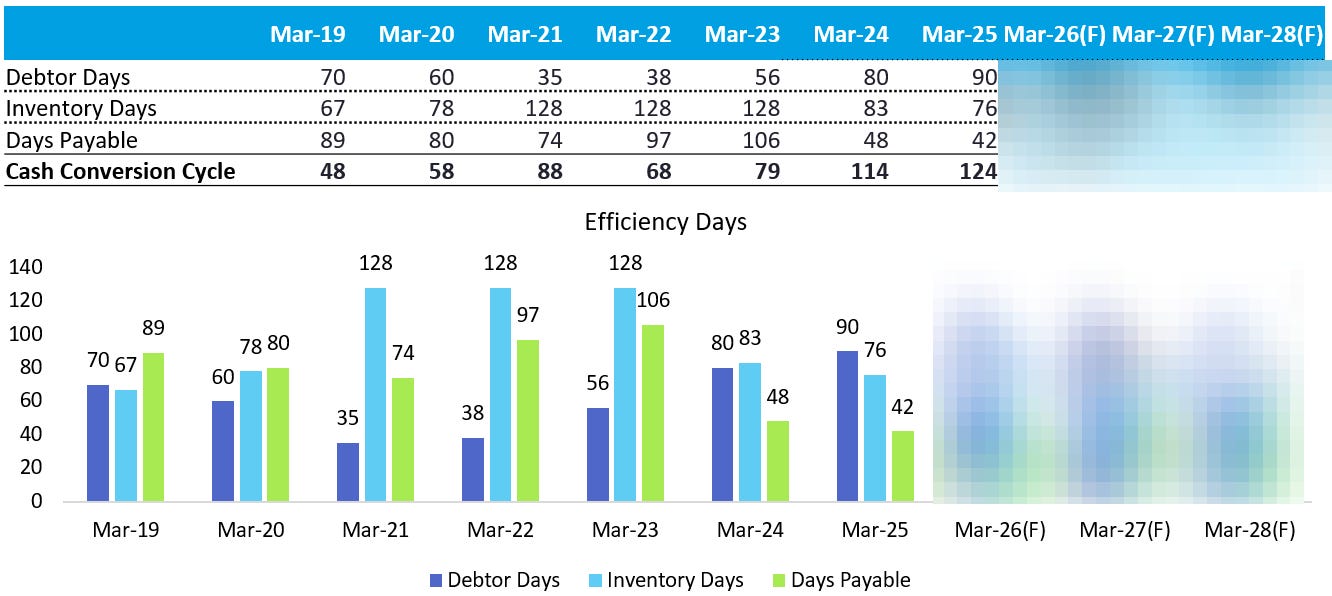

6.8 Cash Conversion Cycle:

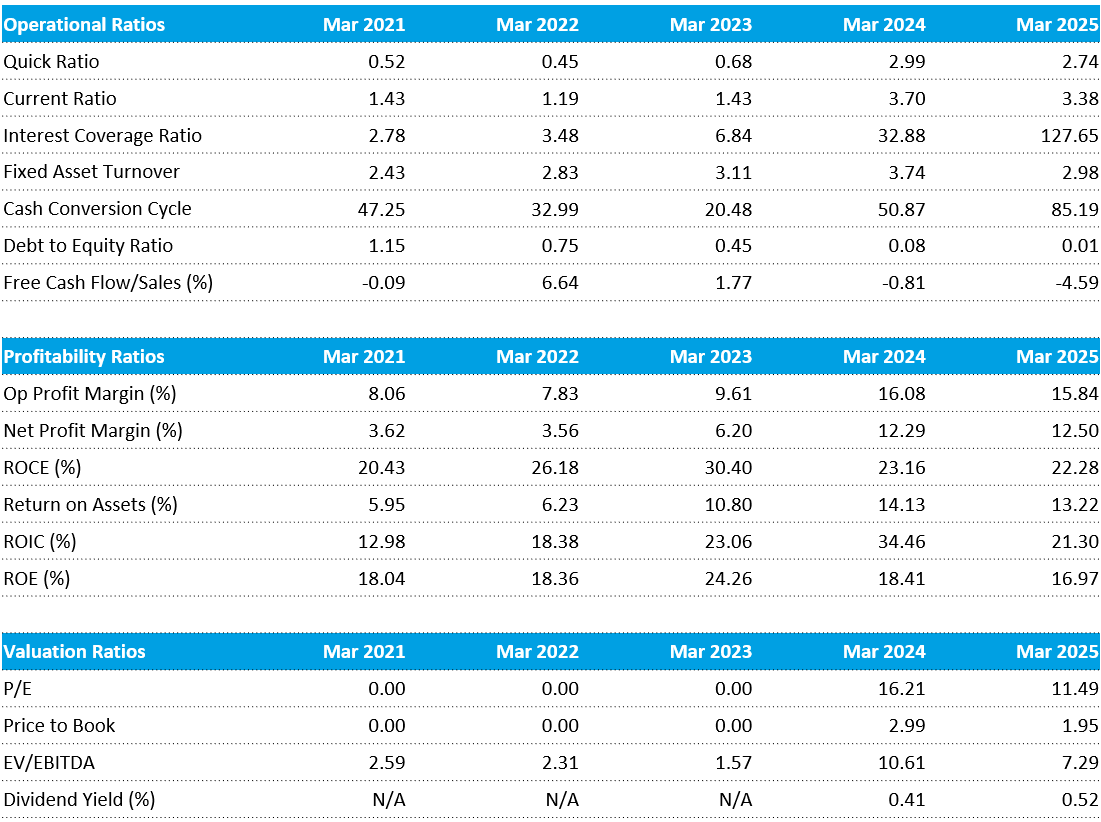

7. Key Ratios:

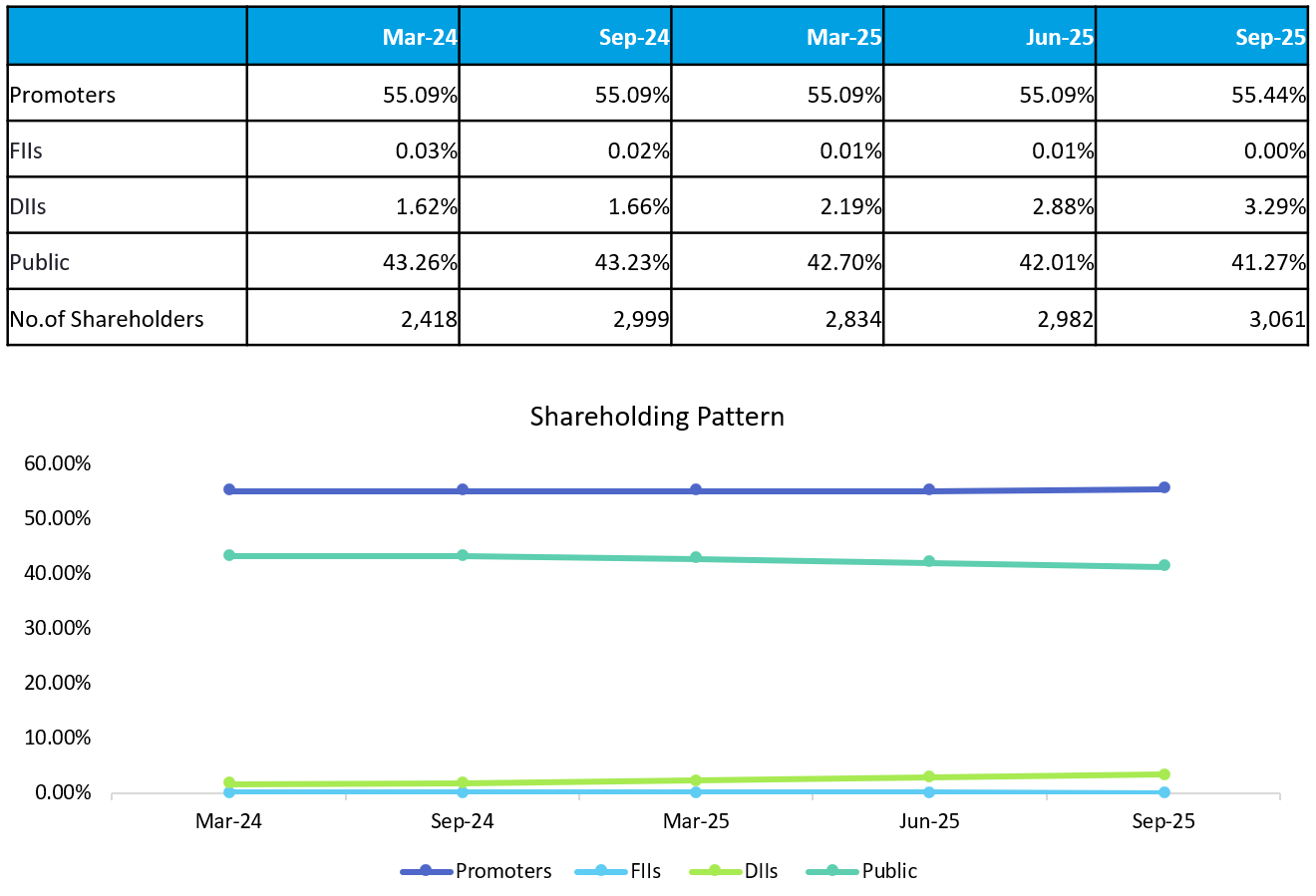

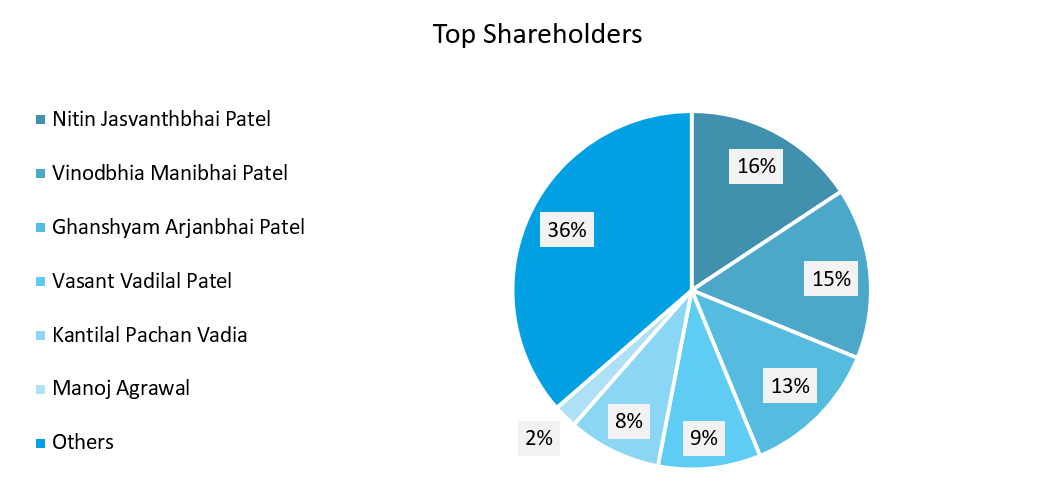

8. Shareholding Pattern:

9. SWOT ANALYSIS:

9.1 Strengths

Defined Capacity Expansion and Modernization: The company has a clear, phased growth plan to more than double its capacity. It will move from a current capacity of 9,600 metric tons (MT) per annum to a total of 24,000 MT. This expansion is structured in two parts: Phase 1, adding 2,400 MT of premium products (by Oct-Nov 2025), and Phase 2, adding 12,000 MT of MCC (by July 2026).

Strategic Product Portfolio Enhancement: The business is actively shifting towards higher-value products. The product basket is set to expand from the current 3-4 products to 12-15 products. The new premium products, such as CCS, have a realization that is approximately 3.5 times that of the company’s core MCC product.

High Customer Switching Costs: The business operates in a highly regulated market where customers (especially in the pharma sector) have lengthy and rigorous approval and validation processes (lasting from several months to a few years) for their suppliers. This creates a sticky customer base and a significant barrier to entry.

Export-Led Business Model: Exports account for a significant 65% of the company’s business, with a strategic goal to increase this to 70% for new capacities. This indicates strong global quality acceptance and reduces dependence on the domestic market. Key export regions include North & South America, Europe, and Asia.

9.2 Weaknesses

Current Production is Capacity-Constrained: With existing facilities operating at nearly 100% utilization, the company has limited ability to meet a sudden surge in demand or grow its volumes organically until the new Unit 3 becomes operational.

Extended Working Capital Cycle to Gain Market Share: In a strategic move to onboard domestic Indian MNCs, the company has offered more liberal payment terms. This has extended the debtor days, as the validation and stability process for these new customers can take 2 to 3 years.

Historical Reliance on Traded Goods: In FY25, traded goods accounted for approximately 15% of sales volume (down from 20% in FY24). While this percentage is decreasing, it represents a lower-value component of the business that will only be drastically reduced once Phase 2 of the new plant is fully operational post-FY27.

Lower-Margin Domestic Business: A significant portion of the domestic business is based on a different manufacturing technology that yields lower-margin products compared to the technology used for the export market. This creates a drag on the overall profitability mix.

9.3 Opportunities

Favorable Competitive Landscape: A recent operational issue at a key competitor’s (Sigachi) plant has created a significant market opportunity. This event has directly led to an increase in inquiries and has provided the company with improved pricing power and an order book that is full for the next 4 to 5 months.

Strong and Growing End-Market: The global market for MCC is estimated at 250,000 MT and is growing annually by 16,000 to 17,000 MT. This robust underlying demand growth can readily absorb the new capacity being added by the company and its competitors. The Indian market alone is estimated at 50,000 MT.

Entering New, Untapped Application Segments: The company has identified new end-user markets for its existing and derivative products, including the cosmetic and tobacco industries, which provides avenues for growth beyond its core pharma and nutraceutical segments.

Margin Accretion from Product Mix Change: With the first phase of expansion focused on 2,400 MT of premium products, the company is positioned for a significant improvement in its product mix. The plan for Unit 3 Phase 1 is to have a product mix of approximately 70% CCS, with the remainder being other high-value products.

Potential for Backward Integration: The company is evaluating producing key inputs like CMC in-house. This would reduce reliance on external suppliers for semi-processed goods and could further enhance operational efficiencies.

9.4 Threats

Impending Increase in Industry Supply: The company’s planned capacity addition is occurring at the same time as competitors are also expanding. For instance, a key peer has also announced a 12,000 MT capacity expansion. This influx of a combined 24,000+ MT of supply into the Indian market could create pricing pressure by export and domestic demand.

Execution Risk on Key Expansion Projects: The company’s entire near-to-medium-term growth strategy hinges on the successful and timely commissioning of its new unit. Any delays in the Phase 1 (target Nov 2025) or Phase 2 (target July 2026) timelines would be a significant setback.

Significant Global Competition: The company competes with established global leaders in its field, specifically “Rocket” from Germany and “Mingtai” from Taiwan. These players have a strong international presence and brand recognition.

Exposure to Geopolitical and Trade Risks: With exports planned to be 70% of the incremental business, the company is inherently exposed to global geopolitical instability, shipping disruptions, and potential tariff changes in its key overseas markets.

10. Concall Analysis:

10.1 Company Overview & Core Business

Core Product: Manufacturer of Microcrystalline Cellulose (MCC), a key excipient used in the pharmaceutical and nutraceutical industries.

Exports: ~65% of total turnover.

Geographic Mix: 55% of business from North & South America, 30-35% from Asia, 8-10% from Europe, and 5% from Australia.

Value-Added Products: Besides standard MCC, the company manufactures and sells premium, value-added products like Croscarmellose Sodium (CCS), SMCC, MCC Spheres, and co-processed MCC, which command higher margins.

10.2 Impact of Competitor’s Plant Incident (Sigachi)

Market Reaction: The company has been receiving a “good quantum” of new business inquiries globally for the “last couple of months.” New inquiries are coming in at higher prices. The incident has created a supply-demand gap in the market.

Accent’s Response: The company is taking a measured approach, first catering to its existing, committed business. It has capacity to cater to the increased demand for the next 4 to 5 months.

Growth Outlook Impact: Management stated that the market CAGR for MCC is typically 5-6%. Due to the current scenario, they expect an additional 1% to 1.5% growth, potentially taking the near-term industry growth to 7-8%.

10.3 Capacity Expansion: Unit 3

Phase 1 (Premium Products): 2,400 metric tons per annum. Focus on premium, high-realization products like CCS (Croscarmellose Sodium), CMC, and SSG. CCS will be the primary focus (~70% of the mix). Commercialization is expected by the end of October or early November 2025. The price realization of CCS is ~3.5 times that of standard MCC. Management has guided for a 25% PAT margin for the CCS product line.

Phase 2 (Standard MCC): 12,000 metric tons per annum of MCC. Expected to come on stream by July 2026. Construction will take approximately one year. The total company capacity will increase from the current 9,600 MTPA to 24,000 MTPA post-completion of both phases. The total capex for Unit 3 (Phase 1 & 2, excluding land) is estimated to be ₹105-110 crores. The capex for Phase 2 alone is around ₹55-60 crores.

10.4 Financial Guidance & Outlook

Long-Term CAGR: The company expects a 15-20% CAGR for the next 3 to 5 years. In the near term, due to the new capacity and market situation, growth could be even higher.

Target Blended EBITDA Margin: With the introduction of high-margin premium products from Phase 1, the weighted average EBITDA margin is expected to improve to 20-22% in the “next couple of years.”

PAT Margin (Full Company): The blended PAT margin on the full 24,000 MT capacity is guided to be 20-22%, subject to utilization levels.

Growth in H1 FY26: Management cautioned that growth in the first half of the year will be “muted” as the current capacity is already optimally utilized, and the new Phase 1 capacity will only come online in Q3.

10.5 Key Q&A Insights

Gross Margin Differences vs. Peers: Management attributed the difference in gross margins compared to peers like Sigachi may have a different mix of products. Accent Microcell uses a higher grade of raw material (”Sapi” pulp vs. “Riya”), which has a higher cost but is required by its pharmaceutical and nutraceutical end-users.

Working Capital: Debtor Days have increased over the last two years. This is due to a strategic push into the domestic market to onboard Indian MNCs, which required offering more liberal payment terms (approval process can take 6 months to 2 years). Management has an optimistic target to reduce working capital days but has not provided a specific number.

Traded Goods: In FY25, traded goods accounted for ~15% of volumes. Post-commercialization of Phase 2, these traded volumes will be drastically reduced and replaced by in-house manufacturing, which will be margin accretive. The margin on traded goods is around 5-7% at the PAT level.

Domestic vs. Export Business: The domestic business (Pirana unit) has negligible profits (~2% margin on ~₹120 crore revenue). The export business is the “money maker.” The company serves the domestic market to maintain customer loyalty and diversify its customer base, which will be crucial once new capacity comes online.

New Customer Win: The company has received final confirmation from a “renowned and well-established multinational company globally” after a 3-4 year approval process. This is a significant win and will lead to large-volume supplies in the coming years.

11.1 Growth Drivers

Unit-3 expansion focused on high-realization, premium excipients

Phase-1 (premium products) capacity ~2,400 MTPA (CCS/CMC/SSG) with CCS ~70% of the mix. Phase-2 adds ~12,000 MTPA of standard MCC, total post-expansion capacity guided to ~24,000 MTPA. Capex for Unit-3 (both phases) ~₹105–110 crore.

Phase-1 brings products (CCS, CMC, SSG) that command materially higher pricing (management cites CCS ~3.5× standard MCC) and higher PAT contribution (~25% PAT on CCS line).

Rapid commercialization of Phase-1 (Oct–Nov 2025 target) accelerates margin conversion before full volume scale.

Product diversification, R&D, and sectoral expansion into higher-growth end markets

Portfolio expanded to 22 MCC grades, SMCC, MCC spheres, co-processed MCC, CCS, SSG, CMC; R&D delivered MCG spheres, MCC powder, SMCC in recent years; roadmap targets cosmetics, personal care, nutraceuticals, food, textiles, and other premium segments.

Diversified, value-added formulations reduce reliance on commoditised MCC pricing cycles and open new, higher-margin customer segments with durable demand growth. R&D capability supports customer-specific co-processed solutions that raise stickiness and ASPs.

Broader addressable market, improved ASPs, and sustained margin upside as the sales mix shifts to co-processed/premium excipients and non-pharma sectors.

Margin recovery by replacing traded volumes with in-house production and improved balance-sheet resilience

Traded goods were ~15% of volumes in FY25 (traded PAT margins ~5–7%), management plans to vastly reduce traded volumes post Unit-3.

Converting traded sales into in-house manufactured, higher-margin products increases gross and PAT margins.

Immediate margin accretion as in-house premium volumes ramp, lower financing stress during scale-up, and higher ROCE as utilisation improves.

Long-standing customer relationships and high entry barriers

Multi-year supply approvals from global MNCs, one newly onboarded multinational client after a 3–4 year qualification cycle, and over two decades of export relationships across 75+ countries.

Pharma-grade excipient suppliers face strict regulatory and quality validation processes, leading to multi-year lock-ins once approved. This results in recurring revenue streams and very low customer churn.

Stable export revenue visibility and sustained order pipeline, even during sector downturns, supporting long-term growth consistency.

Growing global demand for MCC and derivative excipients

Global MCC market size US$1.33 billion (2025), projected CAGR ~7.1%, pharma and nutraceutical industries expanding at ~6% CAGR globally, emerging adoption in food, cosmetics, and personal care.

MCC and its derivatives are essential in formulations across fast-growing consumer health and lifestyle segments. Rising regulatory focus on product safety and quality favours certified suppliers like Accent.

Expanding global demand base enables volume growth across existing and emerging applications, strengthening export momentum.

11.2. Risks/ Challenges

Raw-material dependency & input-quality risk (imported pulp / Sapi grade)

The company imports premium “Sapi” wood pulp (sources include the USA, South Africa, and Sweden); management flags limited domestic wood-pulp availability and geopolitical supply sensitivity.

Product performance (esp. pharma/nutraceutical grades) and customer approvals require consistent quality pulp.

Price spikes or supply disruptions directly raise COGS and can force margin dilution or loss of contracts.

Working-capital and receivables strain from domestic push and liberal payment terms

Debtor days have risen over two years due to onboarding Indian MNCs with extended approval/payment timelines. The domestic Pirana unit (~₹120 crore revenue) operates at ~2% margin.

Management aims to reduce WC days but has not provided targets. Traded goods (~15% of volumes) also create shorter-margin cash cycles.

Larger receivables and inventory during the Unit-3 ramp increase financing needs, even if capex is funded, and lower domestic margins intensify cash conversion pressure.

Margin volatility due to product-mix transition and pricing discipline

The company is transitioning from bulk MCC (lower-margin) to premium CCS/CMC/SSG/SMCC (higher-margin) products, with Phase 1 of Unit-3 heavily skewed toward CCS (~70% of mix).

During this transition, capacity utilization and sales realisation can fluctuate as premium products require longer validation and client onboarding cycles.

A temporary mismatch between production ramp-up and client absorption can depress blended margins and inventory turnover, particularly if new capacity comes online before demand fully materialises.

High export dependence and geographic concentration

Exports contribute ~65% of turnover, with 55% from the Americas, 30–35% from Asia, and 8–10% from Europe.

Despite a diversified country spread, revenue concentration in specific regions like North and South America exposes Accent to currency volatility, trade barriers, logistics costs, and local regulatory changes.

Adverse FX movements, shipping cost inflation, or protectionist measures (especially in the U.S. and Latin America) can erode export profitability and working capital efficiency.

Competitive intensity and new capacity additions in the excipient space

The domestic excipient industry is seeing multiple expansions from organized players like Sigachi Industries, Gujarat Microwax, and emerging unlisted competitors.

As capacity grows faster than demand in India, price-based competition may intensify, especially in standard MCC grades where Accent has limited differentiation.

Overcapacity could lead to price erosion in the MCC segment, putting pressure on margins and utilization rates even as Accent ramps up its new facility.

12. Competitors:

12.1 Sigachi Industries Ltd. — Sigachi Industries is an Indian company focused on manufacturing micro-crystalline cellulose (MCC) and cellulose-based excipients for the pharmaceutical, food, cosmetic and specialty chemical sectors. Founded in 1989 and headquartered in Hyderabad, the company operates multiple manufacturing sites and sells into more than 50 countries. Its product range includes MCC, cellulose powders under brands like HiCel and AceCel, along with other excipients and chemicals. However, the company recently encountered a major industrial accident in its Telangana facility, leading to operational disruption and regulatory scrutiny.

12.2 Patel Chem Specialities Ltd. — Patel Chem Specialities is an Ahmedabad-based manufacturer and exporter of pharmaceutical excipients and specialty chemicals, founded in 2008. Its core offerings include cellulose-based excipients such as sodium carboxymethyl cellulose (Sodium CMC), croscarmellose sodium (CCS), sodium starch glycolate (SSG), calcium CMC, and specialty chemicals like sodium monochloroacetate. The company emphasizes GMP, ISO and FDA-compliance, serves the pharmaceutical, food, cosmetic and industrial segments, and uses in-house R&D to tailor products.

12.3 Kilitch Drugs (India) Ltd. — Kilitch Drugs is an Indian pharmaceutical company that manufactures and markets both generic and branded formulations, and also provides contract manufacturing services for export and domestic markets. It operates manufacturing facilities in India and exports to several countries, offering a wide dosage-form portfolio across various therapeutic categories.

Thank You So Much For Reading!!

Researched By- Naresh, Mayank and Vaibhav

All information is sourced from the company’s annual reports, Press Release, News Articles, GoIndiastocks.in, Screener.in, industry reports, and Economy Outlook reports.

Disclaimer: We do not recommend buying or selling any stock. You should consult your financial advisor before buying or selling any financial instrument.

We are Proud to Announce Our New Launch of the Premium services where we Deep-dive into the Business and back you up with Robust Research.

We Provide services for different Level of Investors. You can Email us directly to start your journey!